Long-term signal vs. Short-term noise

Insight

Stronger than expected US data pushed US yields higher and supported a broadly stronger US dollar on Friday.

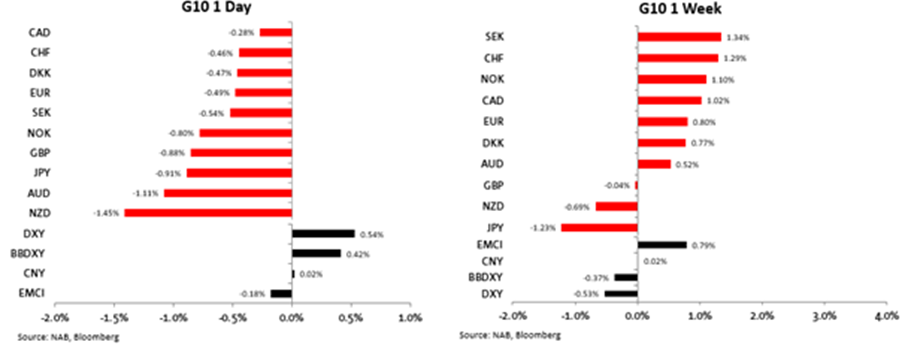

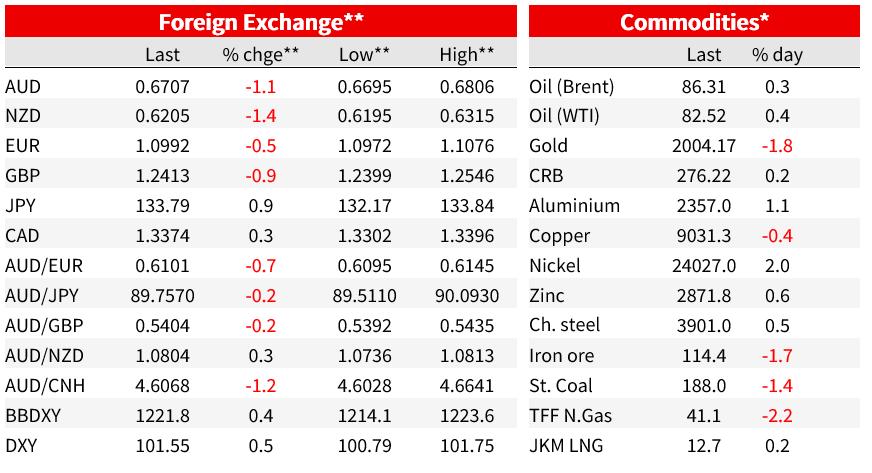

Stronger than expected US data pushed US yields higher and supported a broadly stronger US dollar on Friday. Stronger than expected earnings results from big banks also supported the moves, with Financials outperforming despite a small fall in the S&P500. Friday’s gain in the dollar, up 0.5% on the DXY, unwound Thursday’s move lower, but leaves the DXY 0.5% lower over the week.

In the data flow, retail sales on Friday showed spending down 1.0% m/m in March, sharply below the -0.5% consensus. But the narrower measures were more resilient than expected . Ex autos and gas, retail sales fell just 0.3% m/m (consensus -0.6%) and the control group fell 0.3% (consensus 0.5%). Auto sales fell 1.6% m/m, but after a January surge are still reflecting support from demand backlogs, while a 5.5% decline in gas sales led declines. That suggests a pattern of slowing consumption over the quarter after the weather boosted January, but a solid contribution to Q1 q/q growth. The Atlanta Fed’s GDP-now is running at 2.5% saar in Q1.

Elsewhere, UMich consumer confidence rose to 63.5 (62.0 prior and f/c) and has not shown much impact from recent banking sector turmoil. Of some note is a jump in the 1yr inflation expectations read to 4.6% from 3.6%, though a rise in gas prices through April are a likely culprit. The 5-10yr expectations were flat at 2.9% for a 5th straight month. Industrial production was stronger than expected at 0.4% m/m for Mar, but again weather-related effects inflated utilities production and manufacturing production contracted by 0.5%

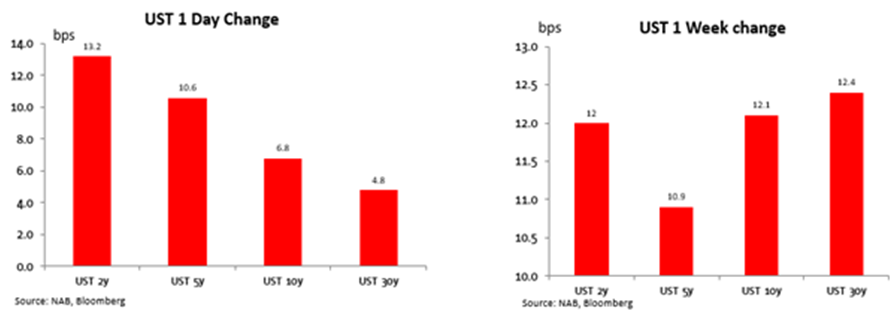

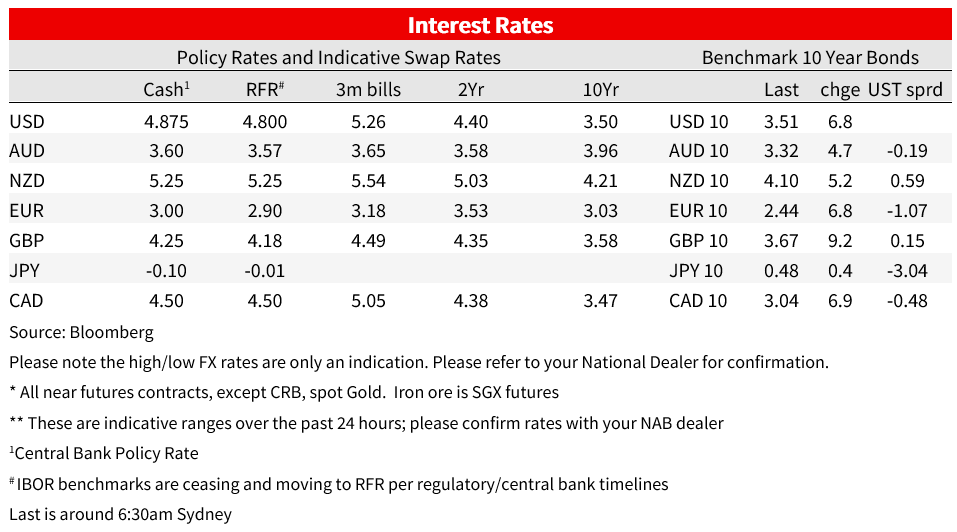

Us 2yr yields were up as much as 15bp following the retail sales data, a large reaction, but helping to sustain the move shortly after were comments from the Fed Governor Waller. The 2yr was up 13bp on Friday to 4.10%, outpacing a 7bp gain in the 10yr. Waller said that “financial conditions have not significantly tightened” and that “monetary policy needs to be tightened further. ” Waller characterised progress on disinflation as having ‘stalled’ by the end of last year and noted surprising strength in jobs data and economic growth suggests, “so far, tighter monetary policy and credit conditions are not doing much to restrain aggregate demand.” Interestingly, he cautioned that banking developments may have “pulled forward factors that were already working to tighten lending conditions” rather than pushed them to a tighter path. Overall, in Waller’s view “monetary policy will need to remain tight for a substantial period of time, and longer than markets anticipate.” But that otherwise strong pushback came with the caveat that he ‘stands ready to adjust his stance’ based on feedback on the economy and lending conditions.

Also on Friday, Atlanta Fed President Raphael Bostic said in a Reuters interview that inflation data “are consistent with us moving one more time.” Some divergence has emerged though, with Chicago President Goolsbee repeating his caution saying it takes time for that to work its way through the system.

The FOMC Minutes earlier in the week noted that Fed officials had taken account of the potential for tightening credit conditions in their March projections, though there was significant uncertainty about the size of the impact. Fed commentary overall doesn’t seem to suggest officials are interpreting the timely banking indicators since as evolving worse than feared. Fed data showed less stress in the banking system last week with demand from banks for liquidity at the Fed’s facilities lower for the fourth successive week and a separate release showed a lift in both deposits and commercial bank lending for the week ending 5 April. On Sunday, Treasury Secretary Janet Yellen said, “ I’m not seeing anything at this time that is dramatic enough or significant enough, in my view, to significantly change the outlook” but did suggest banks are likely to become somewhat more cautious and that could be “a substitute for further interest-rate hikes that the Fed needs to make.”

JP Morgan, Citigroup and Wells Fargo reported on Friday, all topping forecasts and importantly noting that they weren’t materially changing their own lending plans (see WSJ ), though they did increase provisions given expectations for a slowdown in activity and heightened chance of a recession. “I wouldn’t use the word credit crunch,” JPMorgan Chief Executive Jamie Dimon said. Markets now price an 81% chance of a May hike, up from 70% a week ago, and 25bp of tightening by June before 60bp of cuts into the end of the year.

Over the week, the US 2yr was 12bp higher , with rates up across the curve in the US. Despite a quieter week for data flow in Europe, the ebb of immediate banking concerns and no relief on the inflation fight saw European yields sharply higher over the week. 2yr German Bund yields were 33bp higher over the week to a one-month high of 2.88%, their biggest weekly increase since September. Though with a European holiday on Good Friday some of that was catch up to the sharp increase in US yields on Payrolls Friday. The German 10yr yield was 26bp higher to 2.44%.

Markets now price 32bp of hikes for the May ECB meeting , up 10bp from a week ago as investors price in a greater chance the pace of tightening is maintained in May. There was a cast of ECB speakers late last week, with some divergence in views but a clear openness among many officials to consider 50bp. Vasle, Wunsch and Simkus each saw the May decisions as between 25 and 50bp, Nagel said it was ‘far too early’ to stop raising rates, Holzmann told CNBC a half-point hike was ‘in the ballpark’ for May, and hawk Kazaks saw no reason to slow the pace of hikes. A robust chorus that there is more to do, but one which contrast with Villeroy, who said is was premature to decide wheter to hike in May, and Centeno, who said the decision should be between a pause and 25bp.

In FX on Friday the US dollar was broadly stronger, retracing its Thursday declines, but remaining 0.5% lower on the week on the DXY. The stronger dollar on Friday alongside the move higher in yields and resilience in the data took the DXY up to 101.58, pulling away from a low of 100.78. That intraday low was slightly below the previous earlier February low of 100.8 and the lowest since April 2022.

The AUD fell 1.1% on Friday, mostly reversing Thursday’s rise to end the week 0.5% higher at 0.6708. The NZD saw a similar round trip over the final two days of the week, down 1.45% on Friday but losing 0.7% over the week. The AUD rose 1.2% against the NZD over the week, to 1.0804. The pair hasn’t been above 1.0813 since 7 March.

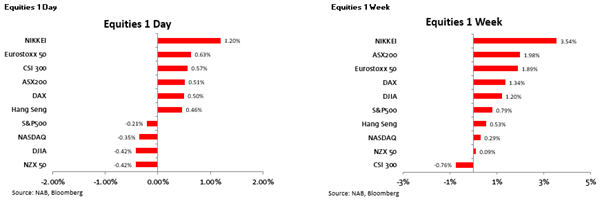

The S&P500 fell 0.2% on Friday even as financials outperformed. That followed a 1.3% gain in Thursday’s session to leave equities 0.8% higher over the week. The more policy-sensitive Nasdaq managed only a 0.1% weekly gain. Strong results from the big financials JP Morgan, Citibank and Wells Fargo, all beating expectations in the quarter and reporting higher profits and Net Interest Margins. JP Morgan shares rose 8%, and Citigroup was 5% higher.

Each of the Banks also saw an increase in deposits. JP Morgan estimated it gained $50 billion in new deposits following March’s bank failures but cautioned they might not stick as things stabilise. Citigroup gained almost $30 billion over the same period, mostly from midsize businesses. Earnings continue this week with Goldman Sachs and Morgan Stanley on Tuesday, but smaller regional banks may be of more interest to gauge deposit outflows.

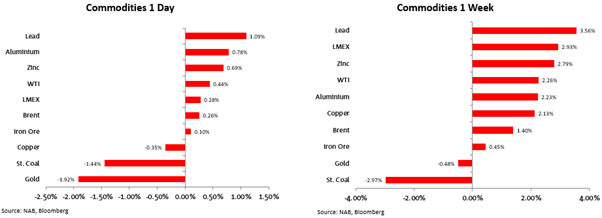

Oil posted its fourth weekly gain over the past week. Brent was 1.4% higher at US$86.31. The IEA said in its monthly outlook on Friday latest OPEC+ cuts threaten to boost oil prices for consumers already facing high inflation. Elsewhere base metals were generally stronger over the week, while iron ore was little changed.

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.