Online retail sales growth slowed in May following a fairly strong April

Insight

Weaker second-tier US data has helped push global yields lower, while disappointing earnings by Tesla (-9.7%) and talk of margin compression dragged down equities.

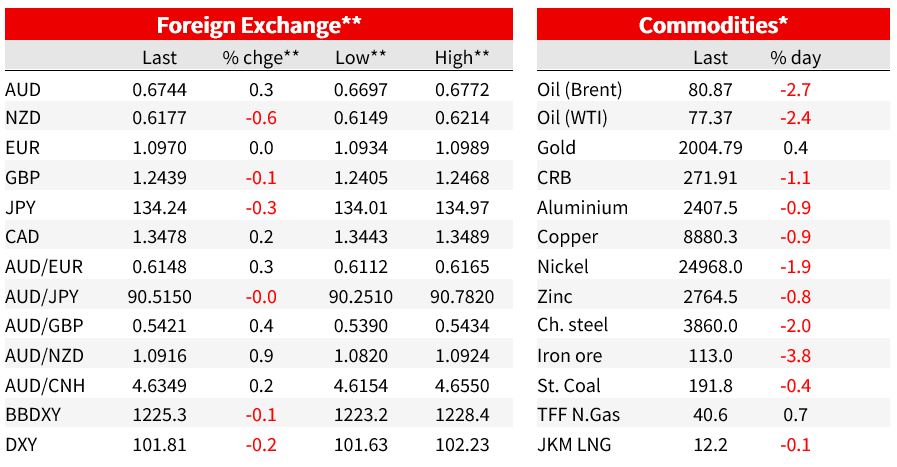

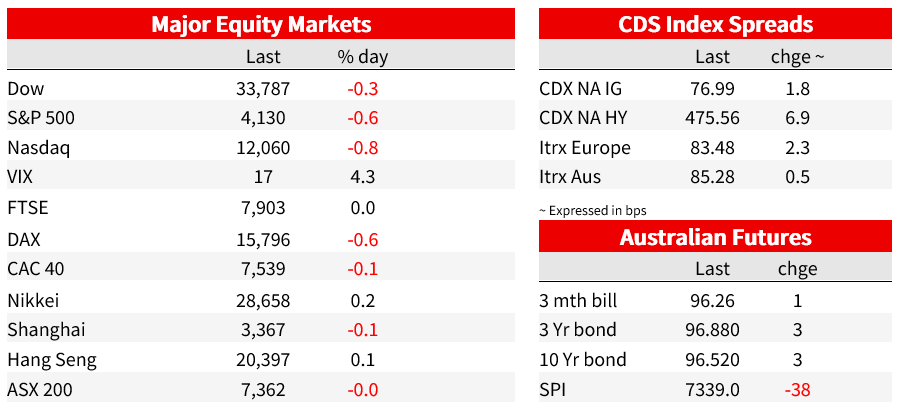

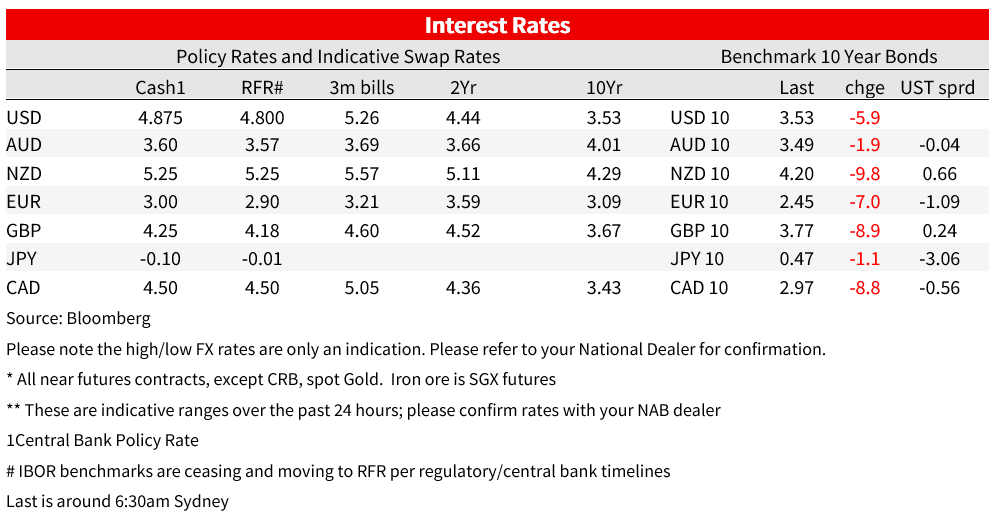

Weaker second-tier US data has helped push global yields lower, while disappointing earnings by Tesla (-9.7%) and talk of margin compression dragged down equities (S&P500 -0.6%; NASDAQ -0.8%). The Philly Fed Manufacturing Survey disappointed (-31.1 vs. -19.3 expected) and jobless claims continue to trend higher. Against that Fed speak remained hawkish. Fed Funds pricing still has an 88% chance of a May hike, but pricing of cuts in H2 2023 moved up to 56bps from 49bps yesterday. Treasury yields are lower and so are European yields. The US 10yr -5.7bps to 3.53% and 2yr -9.9bps to 4.15%. Lower oil prices may be a factor with Brent Oil -2.8% to $80.83, though most of the moves were reflected in TIPs with the 10yr real yield -3.9bps to 1.25% and the implied inflation breakeven was -1.8bps to 2.27%. Topic du-jour around the debt ceiling may be part of it; soft tax receipts see X dates ranging from late May to late July. The USD is weaker (DXY -0.1%). The AUD (+0.3%) has outperformed, and NZD (-0.6%) has reversed around half of yesterday’s fall stemming from the softer Q1 CPI.

First to US, which while second-tier, but did point to a slowing US economy. The Philly Fed Manufacturing Index fell more than expected to -31.3 vs. -19.3 expected and -23.2 previously. The fall was in complete contrast to the New York Empire Fed Survey on Monday (recall it rose to 10.8 vs. -18.0 expected). While details were not as negative, the key takeaway point for your scribe was on the inflation front. Prices Paid and Prices Received declined to their lowest readings since mid-2020, and prices received was actually in negative territory for the first time since mid-2020 (see Philly Fed: April 2023 Manufacturing Business Outlook Survey ). Meanwhile Initial Jobless Claims were broadly as expected at 245k vs. 240k expected, though Continuing Claims lifted a little more (1,865k vs. 1,825k). The trend higher in jobless claims clearly shows a slowing in the labour market and plays to views of a US recession in 2023. Existing Home Sales were also out last night, and were a tad softer at -2.4% m/m vs. -1.8% expected.

There was some Fed speak, but it was not market moving. Speakers reiterated the case for a 25bp move in May and pushed back on the pricing of cuts. The Fed’s Mester (non-voter) noted: “I anticipate that monetary policy will need to move somewhat further into restrictive territory this year, with the fed funds rate moving above 5% and the real fed funds rate staying in positive territory for some time”. Tighter financial conditions in the wake of SVB is likely to do some of the work in bringing inflation down, with Mester noting “With tighter financial conditions, I expect that demand in product and labor markets will continue to moderate and inflation will continue to move down ”. Governor Bowman said we’re still experiencing strong conditions, and the Fed’s Williams late on Wednesday said “Inflation is still too high and we will use our monetary policy tools to restore price stability“. While there will likely be some tightening in credit conditions “it is still too early to gauge the magnitude and duration of these effects”.

As for the US debt ceiling, there is a lot of coverage on what the ‘X-date’ is, when the Treasury runs out of cash. There is some ambiguity over whether the Treasury can make it until June-15, the next big tax take day. If there is enough cash in the coffers until then, that could potentially delay default risk until later in the summer. Concern about the risk of default is causing significant variation in T-bill yields. Investors were willing to accept just 3.19% on an auction of one-month bills, which safely mature ahead of any possible default day, while eight-week bills, which mature after June-15, were sold at 4.85%. Another measure of possible angst is to look at the spread of T-bills vs FHLB notes, with T-bills trading higher than FHLB notes at certain maturities around where X-date could be. No doubt debt ceiling uncertainty and potential market volatility will become more in focus over the next four to six weeks.

Across the ditch, NZ CPI yesterday came in softer at 1.2% q/q vs. 1.5% expected and well below the RBNZ’s 1.8% q/q pick. Tradeables inflation of 6.4% y/y, a full percentage point below the RBNZ’s estimate while non-tradeables inflation of 6.8% y/y and was 0.3 percentage points below. The key messages were that inflation was probably past its peak, weaker than the RBNZ previously thought, but both headline and core measures still remaining too high for comfort and well above target. While there wasn’t much reaction to near-term OIS pricing, with the May meeting still pricing a very high probability of the OCR being raised by 25bps to 5.5%, the data reinforced the likelihood of that being the peak for the cycle. The 2-year swap rate fell 9bps to 5.13%, with the natural focus turning to how long the OCR is likely to remain at its peak and how fast it falls when the easing cycle begins. On that score the market sees some chance of the easing cycle beginning late this year.

The NZD meanwhile fell -0.9% in the wake of the CPI numbers, but recovered overnight to be down -0.6% over the past 24 hours. The USD meanwhile is broadly weaker (DXY -0.1%), with the fall coming after the weaker second-tier US data. The AUD and NZD have been the best performers of the majors overnight: EUR +0.0%, GBP -0.1%, USD/Yen -0.3%.

Finally in Australia, the RBA Review was published with responses given by both the Treasurer and the RBA Governor. The key recommendations of importance for markets are were that the 2-3% inflation targeting framework will be maintained, but the recommendations direct the RBA to target the midpoint of the 2-3% range. It still gives the RBA flexibility in navigating a return to the mid-point, though it requires an explanation of how the RBA is using its flexibility in returning inflation to target, and also asks the RBA to clarify what full employment. Recent communications have increasingly included qualifications about returning inflation to target “in a reasonable timeframe” and the April Board Minutes included: “Members noted that the forecasts produced by the staff in February had inflation returning to the target range only by mid-2025 and that it would be inconsistent with the Board’s mandate for it to tolerate a slower return to target”. A separate monetary policy board is also set to be created (for details see NAB: RBA Review).

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.