Total spending grew 0.9% in June.

US investors have returned from the long weekend in a cautious mood. US and EU equities are broadly weaker with big tech outperforming, helping the NASDAQ stay on the green. Core yields are also higher with supply and ECB meeting on Thursday factors at play.

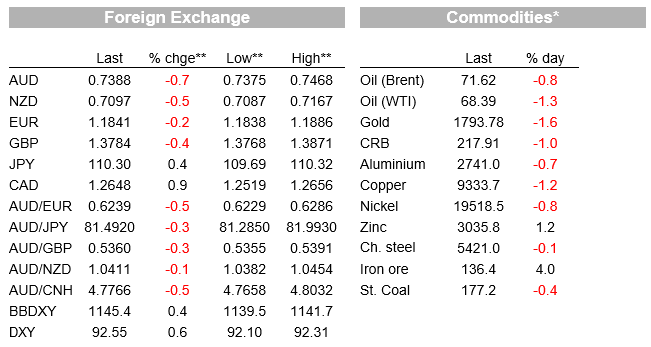

US investors have returned from the long weekend in a cautious mood. US and EU equities are broadly weaker with big tech outperforming, helping the NASDAQ stay on the green. Core yields are also higher with supply and ECB meeting on Thursday factors at play. The USD has extended its post payrolls recovery with CAD, AUD and NZD at the bottom of the G10 board.

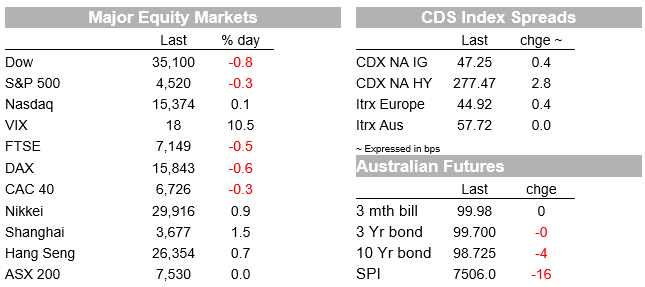

The S&P 500 has ended the day down 0.34% while the Dow is -0.76%. Industrials and Utilities are the big underperforming sectors while communication and IT are up on the day. Indeed, big tech companies, FANG and Friends, are the notable outperformers ( NYSE FANG+ index is up 1.6%) helping the NASDAQ index close in the green, +0.07%. Meanwhile European equities also closed broadly weaker with the Stoxx 600 down 0.5% as investors begin to consider potential implications from the ECB meeting on Thursday.

There has not been a clear catalyst for the change in mood . Headlines about rising infection in US hotspots have probably not helped while the end of unemployment benefits for millions of Americans is another subject in the media. Overall, it just seems investors are taking some time to ponder the implications from the softer than expected payrolls number on Friday. Yesterday Goldman Sachs downgraded US growth to 5.7% in 2021 from 6% in August amid signs American consumers are likely to spend less due to the Delta variant’s emergence, fading fiscal support and a switch from demand for goods to services.

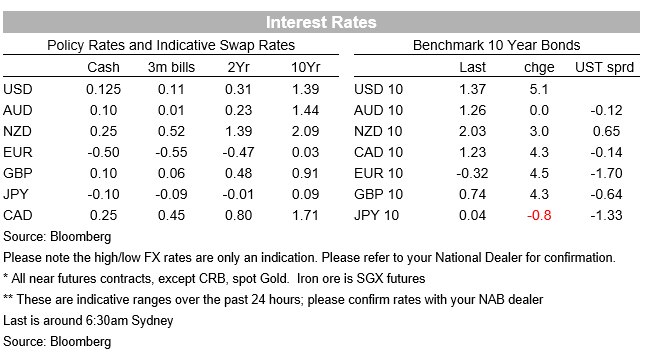

Core yields have also moved up overnight with Supply and the ECB meeting on Thursday likely factors at play. 10y UST yields are up 4 bps to 1.37%, after trading to on overnight high of 1.38%. The US Treasury is planning to issue $120bn of bonds this week with the first tranche last night meeting decent demand. The 3y Note auction of $58b drew strong demand at a yield just below the prevailing market rate. 10-year and 30-year auctions are scheduled for the next two days. Core yield in Europe also rose overnight, 10y Bunds and 10y Gilts rose 4bps to while Italian BTPS gained 6.4bps to -0.322%, 0.737% and 1.24% respectively. The move came on the back of Spain selling EU5b of debut green bonds, Austria offering 10-and 15-year notes and the UK. auctioning 4- and 50-year Gilts. Investors are wary of the ECB meeting on Thursday anticipating a potential trim to the PEPP bond buying pace.

Risk aversion in the air alongside the move up in UST yields have helped the USD extend its post payrolls recovery. The BBDXY and DXY indices are up 0.48% and 0.35% respectively and the USD is stronger across the board. Ahead of tonight BoC policy meeting (more below), CAD is the notable G10 underperformer, down 0.85% as the market anticipates a dovish BoC narrative. Move lower in oil prices, down 1%, has not helped the loonie either.

The AUD is down 0.65% and now trades at 0.7365, partly reflecting broad USD strength although yesterday’s RBA dovish taper has also played its part. As expected by NAB, yesterday the RBA stuck to its plan to purchase government securities at the reduced rate of $4 billion a week.The Bank also said it will continue the purchases at this rate until at least mid-February 2022 (so longer review period to February 2022, as opposed to November previously). The RBA is still expecting a strong rebound in 2022, noting “This setback to the economic expansion is expected to be only temporary. The Delta outbreak is expected to delay, but not derail, the recovery.

Global forces have dragged the NZD lower, going just below 0.71 and currently around that mark . Indeed, 71c continues to prove a tough nut to crack for the kiwi. NZD underperformance highlights the influence of global forces with the pair ignoring a strong GDT dairy auction overnight. My BNZ colleague, Jason Wong, noted the price index gained 4% with all products for sale contributing. Whole milk powder rose by 3.3%, skim milk powder rose by 7.3% and both butter and cheddar were up over 3½%. The NZX future for the FY2022 milk price has been steadily rising over the past month, from $7.65 to just over $8 and the overnight auction supports an $8 payout. The recovery in dairy prices provides more fuel for NZ’s record-breaking run in its terms of trade, a supportive factor for NZ farm incomes and the NZD over the medium-term.

In other news, Germany’s ZEW Institute’s analyst/investor survey for September saw a slight improvement in current conditions from 29.3 in Aug to 31.9 – a post pandemic high, but not quite as high as expected (34). Once again however, the forward-looking expectations index slipped – this time to 26.5 from 40.4 and to below the forecats of 30.3. This measure peaked at 84.4 back in May and though it has been sliding since it remains above pre-pandemic highs (just).

Finally, Bitcoin has been stealing some headlines, after falling as much as 17% overnight , after “Bitcoin Day” – the day El Salvador became the first nation to adopt it as legal tender. The app in El Salvador crashed for a few hours which didn’t help confidence. BTC has since recovered a little, now down “only” 10% to just under $47k.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.