Total consumer spending grew 0.7% in July

Insight

Us equities haven fallen sharply, bond yields are lower and AUD/USD is back near 0.66, ahead of CPI this morning.

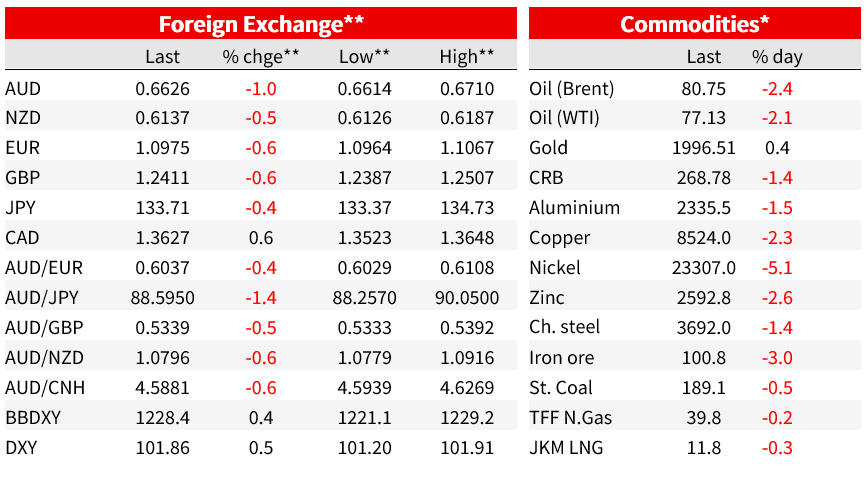

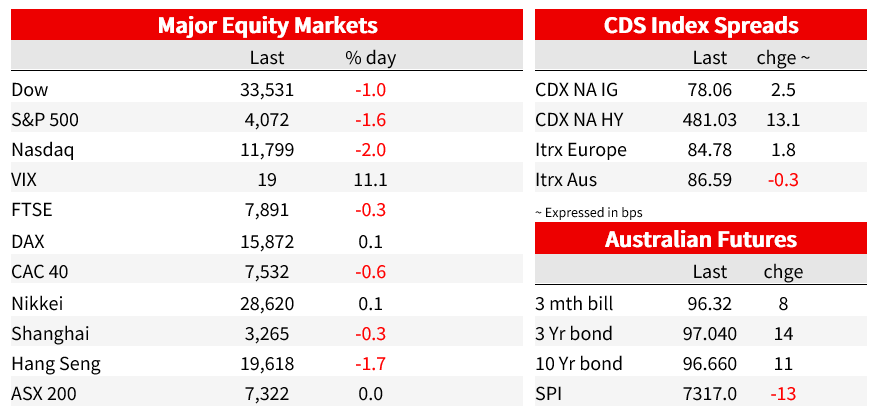

Banking sector stress is back in the headlines this morning with shares in First Republic Bank down 50%. Stock market declines are broad-based though with IT and consumer discretionary stocks faring even worse than financials, the S&P 500 closing down 1.6% ahead of Microsoft and Alphabet’s Q1 earnings reports (just released, with both comfortably beating their consensus street estimates) . The VIX is back above 19 from sub-17, Treasury yields are down as much as 16bps (2-years) with the market-implied probability of a 25-point rate hike from the Fed next week reduced to 75% from 90% on Monday. The USD has attracted a fresh haven support, DXY currently +0.5%. AUD has again underperformed other G10 currencies bar NOK (oil prices are down more than 2%) to be 1.1% lower at 0.6623.

First Republic Bank reported its earnings after the market close on Monday, revealing a bigger than expected deposit loss on Q1 (down 41% to $104.5bn against a street consensus of $136.7bn). It announced plans to cut headcount by 20-25% this quarter and said it was examining ‘strategic options’. Overnight, Bloomberg is citing unnamed sources saying the bank is exploring divesting $50 billion to $100 billion of long-dated mortgages and securities to reduce the bank’s asset-liability mismatch (SVB redux?) as part of a broader rescue plan. Potential buyers, including large US banks, might receive warrants or preferred equity as an incentive to buy assets above their market value, one of the sources said. The lender is trying to shore up its balance sheet to avoid being seized by the Federal Deposit Insurance Corp. and clear the path for a possible capital raise, the report says.

The KBW bank index closed down 3.4% with the S&P 500 down 1,6%, the Dow -1.0% and the NASDAQ -2%, The latter might draw some support in the futures market today, at least on a relative basis, after Alphabet and Microsoft reported earnings post-NYSE which have both comfortably beaten their street consensus. Microsoft was 4-5% up in immediate post earnings trade, Alphabet 3% but both in highly volatile trade..

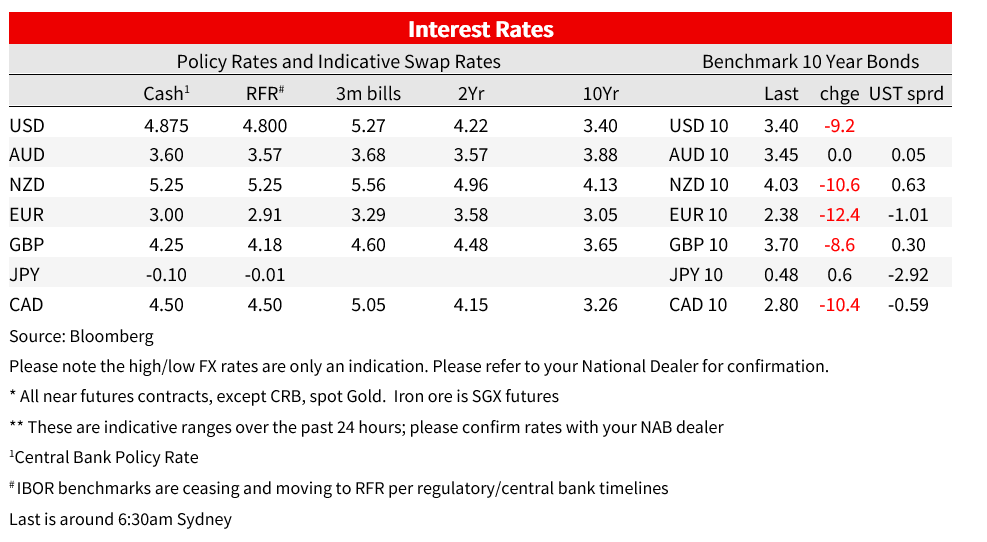

The return of the US regional banking sector to the headlines and related equity market weakness has seen US Treasury yield mostly lower. 2s by as much 10bps on Monday’s close at one point and currently off 15bps to 3.94%. 10s are down 9bps to 3.40%. The US money market is also now expressing less confidence in another Fed hike as early as next Wednesday, with Mondays 90% market implied odds of +25bps reduced to 79%.

At the macro not micro or sector/name specific weakness in stocks, the US debt ceiling is now more fully rearing its head as a market issues after disappointing April tax receipts have raised the prospect of the US Treasury running out of cash and the ability to apply various accounting ruses as early as June. Also being mentioned in dispatches is President Biden formally announcing he will run for a second term next year. A Biden-Trump rematch is looking highly probable.

On the data front, the Richmond Fed’s manufacturing index – the fourth of the regional manufacturing surveys released so far – fell to -10 from -5 against -8 expected. This means that three of the four surveys (Philly, Dallas (reported Monday at -23.4 from -15.7) and now Richmond have been weaker than March and all contradicting the unexpected strength in the (smaller) Empire State survey at the end of last week. The data so far are consistent with another ISM Manufacturing survey (May 2) deep below 50 in April. March was 46.3 and the consensus for April prior to most of these surveys sits at 46.8. Services have been doing much better than manufacturing according to last week’s S&P Global survey and some of regional services indices so far reported (albeit in Philadelphia’s fell to -22.8 from -12.8 overnight). ISM Services is next Wednesday, a few hours before the FOMC concludes its May meeting.

The US Conference Board’s April Consumer Confidence index came in weaker than expected but not alarmingly so at 101.3 from 10.4, driven by the Expectations component (probably picking up the full effect of the March banking sector turmoil) while the Present Situation lifted slightly to 151.1 from a downward revised 148.9, reflective of ongoing strength of the labour market, though in the expectations series, the proportion of people expecting greater job availability in six months’ time fell to 12.5%, reportedly the lowest since May 2016.

Thirdly on the US data front, March New Home Sales rose much more than expected, up 9.6% on the month (consensus -1.3%) though lack of supply of existing homes is seen to have played a large part in this, as well as homebuilders reportedly cutting prices to clear inventory overhang where Pantheon Economics notes builders still have 7.6 months’ worth of inventory against just 2.8 months for existing homes. Other data of note released Monday evening ahead of the ANZAC day holiday included the German IFO survey, which improved by a bit more than expected (93.6 from 93.3) driven by the Expectations component.

In FX, lower Treasury yields are doing the USD no harm whatsoever given their risk-off drivers, the DXY index coming into the New York close +0.5% at 101.8 (so about 1% up on last week’s revisit to its 1-year lows). The broader BBDXY +0.44%. JPY is the only currency up against the USD, more reflective of sharply lower US Treasury yields than safe haven support per se. Most G10 pairs are 0.5-0.7% down on the day, including NZD but excluding AUD, AUD/USD off a cool 1.1% to 0.6623 at present and a low of 0.6614 (its weakest since March 15). NOK is off 1.5% in conjunction with 2% or bigger falls for WTI and Brent crudes, the latter seemingly on deepening demand concerns. In this regard base metals are all lower (copper -2.3% and nickel more than 6% down). Gold is up $7 in conjunction with lower yield but at $1,996.45 is still comfortably inside recent ranges.

Total consumer spending grew 0.7% in July

Insight

Investing and risk management in a world of shifting and unstable cross-asset correlations

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.