Online retail sales growth slowed in May following a fairly strong April

Insight

The US share market is split between tech majors, doing well on the back of strong earnings versus Financials (and the rest) which are buffeted by banking uncertainty and recession fears. Core global yields are higher and the USD is weaker largely reflecting EU FX outperformance while the AUD has led a commodity linked FX decline.

NZ: Trade balance (ann $b), Mar: -16.4 vs. 15.7 prev.

AU: CPI (y/y%), Q1: 7.0 vs. 6.9 exp.

AU: CPI trimmed mean (q/q%), Q1: 1.2 vs. 1.4 exp.

AU: CPI trimmed mean (y/y%), Q1: 6.6 vs. 6.7 exp.

GE: GfK consumer confidence, May: -25.7 vs. -28.0 exp.

US: Goods trade balance ($b), Mar: -84.6 vs. -90.0 exp.

US: Durable goods orders, Mar: 3.2 vs. 0.7 exp.

US: Durables ex transportation, Mar: 0.3 vs. -0.2 exp.

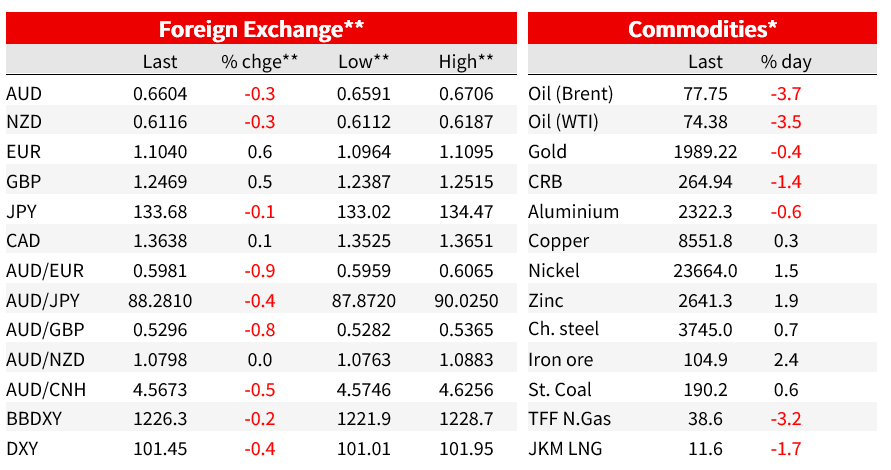

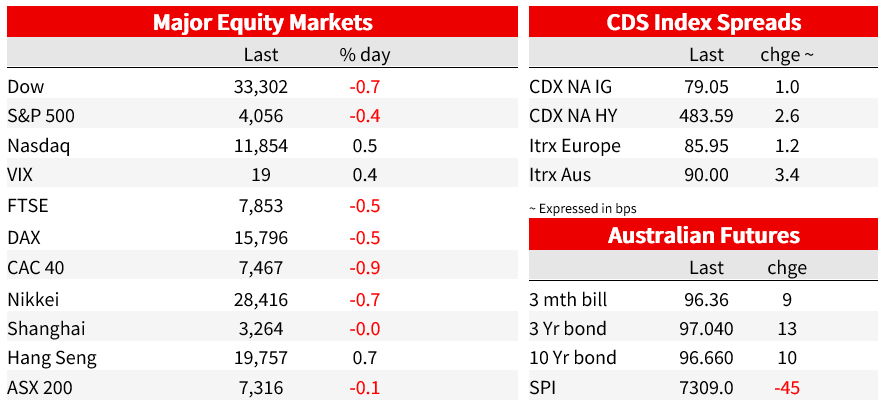

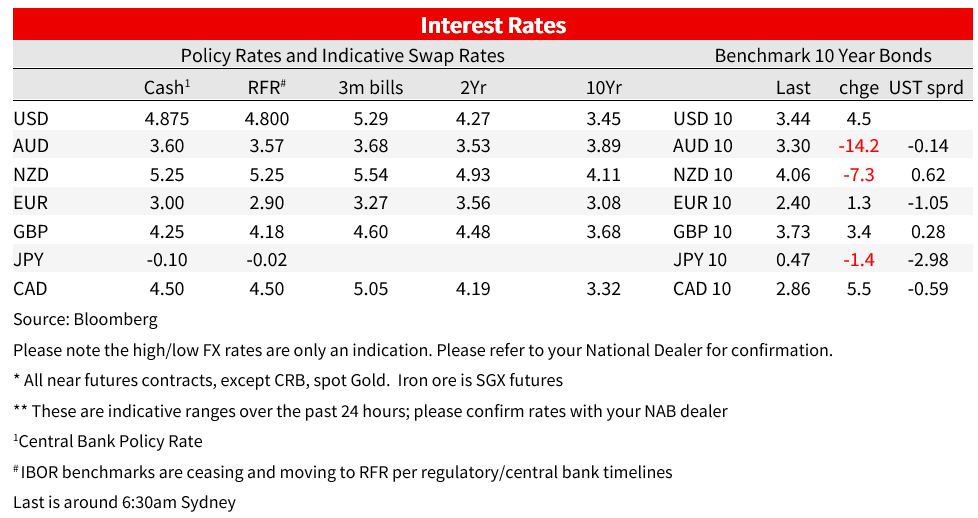

After a positive start, the S&P 500 fell for a second day in a row with banking afflictions outweighing better than expected Tech company earnings. First Republic Bank fell another 30% following reports the government is currently unwilling to intervene for the bank. Core yields have edge higher with 10y UST yields up 4bps to 3.445% while the USD is softer, mostly reflecting EU fx outperformance. The AUD has led a commodity linked FX decline and starts the new day at 0.6605

After jumping close to 0.4% at the open, largely reflecting the better-than-expected earnings results from both Alphabet and Microsoft after the bell yesterday, the S&P 500 recorded a second consecutive day of negative return. The benchmark closed the day down 0.38% with the tech heavy NASDAQ up 0.47%. Concerns over the US banking sector continues to weigh on sentiment with First Republic Bank the centre of the attention. The bank’s shares fell over 40% intraday, recovering before the close to end the day “just” 30% lower, after falling 50% in the previous day. The bank is currently fighting for survival and the overnight sell off came after CNBC reported the government is currently unwilling to intervene for the bank.

Bloomberg notes that regulators are angling towards a private rescue that doesn’t involve the US seizing the bank and taking a multibillion-dollar hit to the FDIC’s insurance fund. On the other side, large banks that could come to the rescue are waiting for more aid from the government. CNBC reported that the bank’s advisers have lined up potential buyers for new shares. The challenge is that this requires the large US banks which have already contributed $30bn of deposits to First Republic, to agree to buy bonds from the company for more than they’re worth. CNBC notes the banks would suffer an immediate loss, but if First Republic survives the large banks could benefit from a recovery in First Republic share price as well as avoid a bigger loss on the deposits they made plus any FDIC fees that would follow a failure.

The US share market is split between tech majors, doing well on the back of strong earnings with Meta, the latest on that front, surging after the bell today following better than expected earnings as well as a strong Q2 outlook while Financials (and the rest) are hit by banking uncertainty and recession fears. Of some relief and suggesting banking concerns are not yet a systemic risk, smaller regional bank PacWest Bancorp, which has also been on the watchlist, is up over 10%, after reporting stable deposits in late March and a rebound in April.

Core global yields edge up overnight with the UST curve showing a mild flattening bias.10y and 5y UST yields climbed around 4bs to 3.49% and 3.448% respectively with the 2y tenor up 6bps to 3.95%.

Looking at economic news, US durable goods orders for March revealed a surge in the headline (+3.2% m/m following vs the 0.7% consensus f/c) thanks to a jump in aircraft orders which reversed weakness seen in February and January. Ex-aircraft orders were +0.3% m/m, still above a 0.2% estimate. But the more important non-defence capital goods orders ex-aircraft were weak at -0.4% and with a revised -0.7% (originally -0.1%) for February. The consensus for core capex was -0.1%. These data will act as a (very) partial drag to tomorrow’s advance GDP data where consumption will surge thanks to the warm January weather, only to be offset by investment and inventories.

Meanwhile in Germany, the economic ministry raised its 2023 GDP growth forecast for a second time, now 0.4%, up from 0.2% three months ago and the 0.2% contraction expected six months ago. The economic minister said “we now see that a gradual recovery is underway, despite a persistently difficult environment”.

Moving on to currencies, the USD is weaker in index terms (DXY -0.37%, BBDXY -0.19%), largely reflecting EU FX outperformance while commodity linked currencies are weaker with the AUD leading their declines. The aussie now trades at 0.6603, down 0.5% over the past 24 hours, after trading to overnight low of 0.6591.Yesterday the softer than expected Australia Q1 CPI report weighed on the AUD with declines in oil prices extending the pair’s decline overnight.

Yesterday, Asutralia’s Core Trimmed Mean Q1 CPI came in two-tenths less than market expectations at 1.2% q/q and 6.6% y/y (consensus 1.4/6.7, NAB 1.3/6.6). Headline inflation was a fraction above consensus at 1.4% q/q and 7.0% y/y, (consensus 1.3/6.9, NAB 1.3/7.0). The data confirmed the widely held expectation that Australian inflation peaked late last year (Q4 2022), but more importantly for markets the softer than expected outcome dowsed the possibility of the RBA hiking next week, extending the pause in the tightening cycle. That being said, with inflation remaining uncomfortably high, the possibility of some further tightening later in the year remains elevated. Still, bond futures rallied after the result, with the 3-year and 10-year rates falling 6-7bps in yield terms, but unwinding much of that move overnight.

A decline in oil prices (-3.7% Brent, -3.5% WTI) which came about notwithstanding a notable drop in US crude inventories, weighing on commodity linked currencies overnight, largely reflecting concerns of an upcoming global growth slowdown. NZD was not helped by the AUD’s decline, following a similar path and starts the new day at 0.6117 (down 0.36% over the past 24 hours) while CAD was -0.2%.

Meanwhile EU currencies outperformed with the euro trading to an overnight high of 1.1095 , its highest level in over a year, before sliding back to 1.1041 where it currently trades. GBP traded above 1.25 and currently sits around 1.2469. JPY is up 0.16% with USD/JPY trading at ¥133.66 ahead of the BoJ meeting tomorrow.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.