We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Big moves in markets overnight as US regional bank worries reignited, signs of catering in European loan demand, and a sharp fall in US job openings.

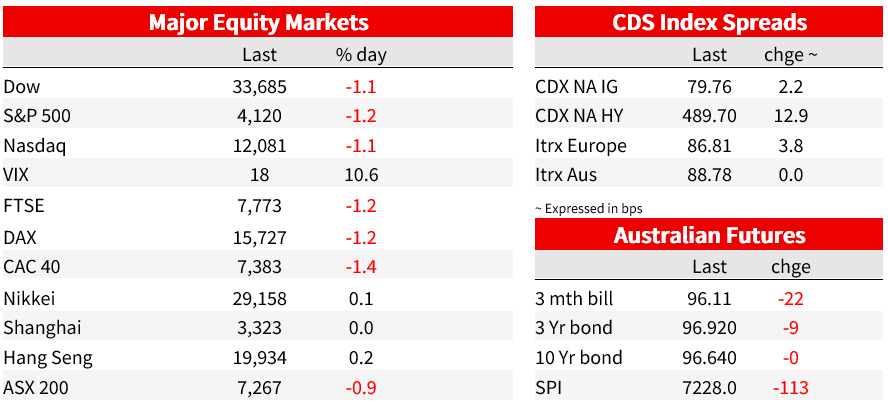

Big moves in markets overnight as US regional bank worries reignited, signs of catering in European loan demand, and a sharp fall in US job openings. That all came after the RBA shocked markets yesterday by hiking by 25bps and guiding that some further tightening may be required. The US regional bank index KRE closed down -6.3% with very sharp falls in some regional banks – e.g. PacBank -27.8%. The broader S&P500 was ‑1.2% (at one point it was -1.9%), while across the pond the Eurostoxx50 was -1.5%. Driving the sell-off appears to be concerns around commercial real estate exposures, no changes to FDIC deposit insurance after changes had been mooted, and perhaps fears that signs of catering loan demand in Europe may play out in the US.

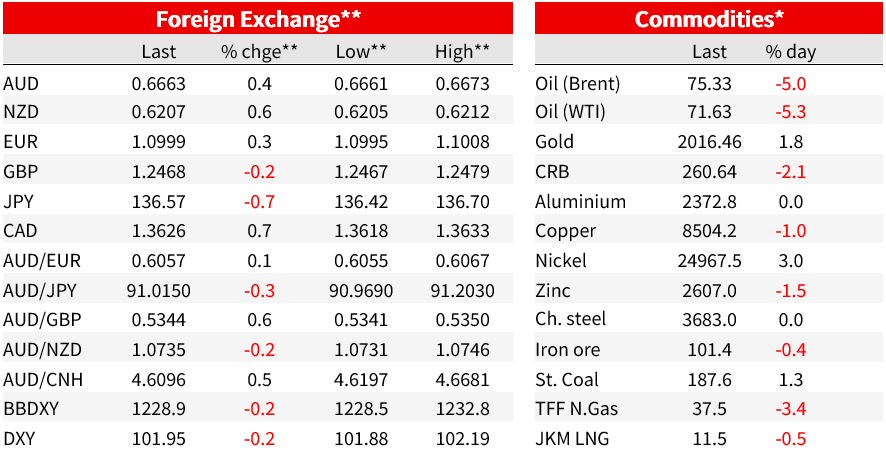

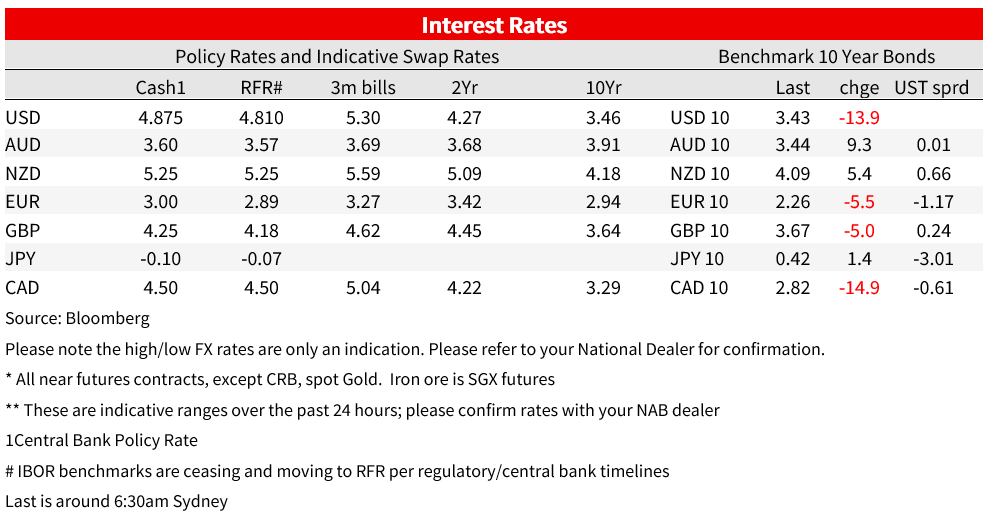

The new debt ceiling X-date of 1 June may also be in the background. Yields fell sharply, firstly on the risk off banking sector tones, and then extending losses post the JOLTS data (9590k vs. 9736k expected). The US 2yr yield fell -17.1bps to 3.96%, with a similar move in 10yr yield of -14.1bps to 3.43%. Oil prices tanked with Brent -5.0% to $75.33 and Gold rose 1.8% to $2,017. The USD was down slightly with DXY -0.2%, while the AUD pared back its outperformance, up 0.4% over the past 24 hours after having been up on the back of the RBA shock hike yesterday with the AUD +0.4% to 0.6663, at one point it hit a high of 0.6717. Other major pairs were mixed with EUR +0.3%, USD/JPY -0.7% to 136.57 as risk off supported and reversing some of the post-BoJ weakness. USD/CAD was +0.7% given oils sharp fall. The NZD meanwhile looks resilient +0.6%. Looking to tonight’s FOMC, markets are still 86% priced for a 25bp hike, but also have 62bps worth of cuts priced in H2 2023.

First to Europe where a tightening in credit conditions appears to be playing out, and reinforcing views the ECB will only hike by 25bps on Thursday (markets have 26.5bps priced). The ECB’s Bank Lending Survey said credit conditions had “tightened further substantially” in Q1. Looking into the details the survey showed there had been a sharp reduction in loan demand, as well as a tightening in credit conditions. The survey showed a net 38% of banks reported a decline in demand for credit from companies in the first three months of this year, the biggest share since the global financial crisis of 2008-09. While on credit standards the pace of net tightening in credit standards remained at the highest level since the euro area sovereign debt crisis in 2011 (see ECB: Bank lending survey). Other data out in Europe included the latest April CPI where core inflation was as expected at 5.6% y/y, though headline was a tenth more than expected at 7.0% vs. 6.9% consensus.

As for the data, the US JOLTS report saw job openings fall -3.9% m/m to 9590k (vs. 9736 expected and 9974k previously), its lowest since April 2021. Even with the fall though, the labour market remains tight with there still being 1.64 job openings per unemployed person. Other stats pointed to slightly more easing up of tightness with the quit rate easing to 2.5% from 2.6%, and suggesting employees are seeing diminishing prospects of switching to higher paying jobs, although the quit rate remains above its 2.3% pre-pandemic average. Layoffs also rose to 1.8m, up from 1.6m in February, with the increase led by job losses in construction, leisure and hospitality and healthcare. Also out overnight were a final-version of durable goods, which was broadly as expected with core durables excluding transportation at 0.2% m/m vs. 0.3% expected.

Finally, the RBA shocked markets, hiking rates by 25bps to 3.85% and giving guidance that more could come (“some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe”). For your scribe the most important point was that inflation is still only expected to get to 3% by mid-2025, and that is the upper bound of the RBA’s tolerance. It doesn’t take much re-assessment of the risks to get the RBA to move. And the inflation risks remain to the upside and asymmetric with “services price inflation is still very high and broadly based and the experience overseas points to upside risks. Unit labour costs are also rising briskly, with productivity growth remaining subdued ”. That probably points to the RBA thinking they may need to do another 25-50bps. Governor Lowe explained the decision in a speech last night, noting that the rationale was that “we have seen further evidence that the Australian labour market is still very tight, that services price inflation is proving to be uncomfortably persistent abroad, and that asset prices – including the exchange rate and housing prices – are responding to changes in the interest rate outlook”. (see NAB commentary for details).

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.