We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Markets were spoked on Friday by an unexpected rise in US consumer inafltion expectations

Friday’s key data releases:

US: U. of Mich. Sentiment 57.7 from 63.5 vs 63.0 expected

US: U. of Mich. 5-10 Yr Inflation 3.2% from 2.9% vs 3.0 expected

US: U. of Mich. 1 Yr Inflation 4.5% from 4.6% vs 4.4% expected

UK: Q1 GDP 0.1% vs 0.1% expected

UK: March GDP -0.3% vs 0.0% expected

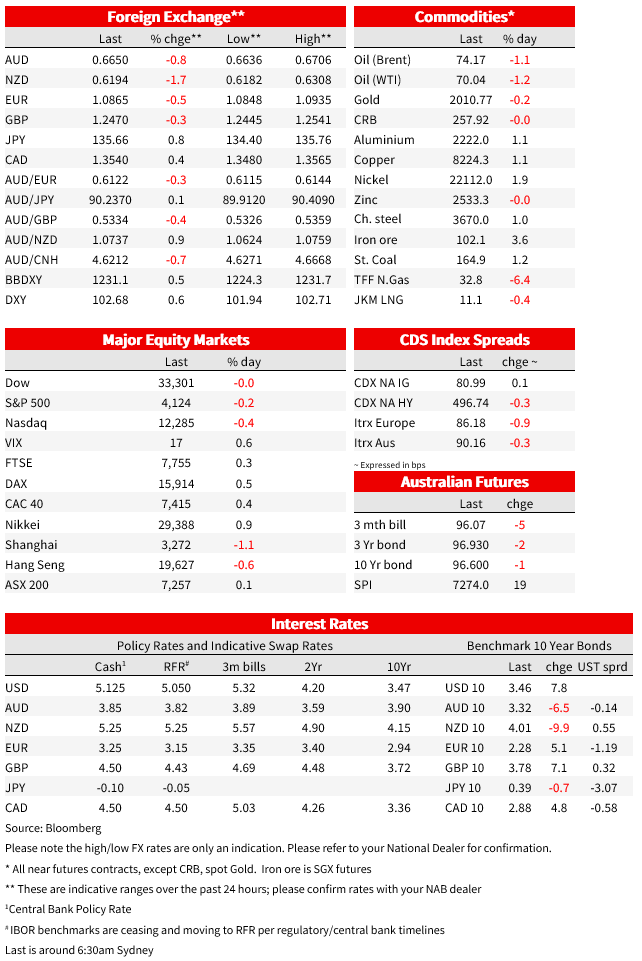

Bond, currency and equity market were all spooked on Friday by the reported rise in the 5-10 Yr. inflation expectations component of the University of Michigan’s preliminary May Consumer Sentiment survey. It rose to 3.2% from 2.9% against an expected 3%, its highest reading since March 2011 (also 3.2%) and previously higher (3.4%) as far back as mid-2008 just prior to the GFC. No matter that Consumer Sentiment itself slumped to 57.7 from 63.5, well below expectations. The release sparked a 10bps jump in front-end US bond yields, a 0.5% rally in the DXY dollar index and near 1% fall in the S&P 500 (about half of which was subsequently retraced). In the US money market, the release has sown a few seeds of doubts regarding confidence the Fed will pass on another rate rise next month, June Fed Funds pricing finishing Friday ascribing a 13% chance to another 25bps hike, up from less than 3% on Thursday.

The blip up in inflation expectations could easily have been dismissed as noise and could well be revised in the final reading. Indeed, as one of our favourite economic commentators, Phil Suttle, observed on Saturday, if central banks’ own forecasts of inflation, made by the supposed biggest experts on the subject, can be so much in need of regular adjustment (e.g., the BoE’s MPC just revised its view for inflation in Q2 2024 from 1% to 3.4%) then what hope does the Uni. of Mich. crowd have in being vaguely right 5 to 10 years out? Yet the fact is, Jay Powell, as Janet Yellen before him, makes explicit mention of this series as something the Fed watches closely.

Fed speak on Friday included Philip Jefferson, now formally nominated for Fed Governor, who said that the full effects of rapid rate hikes was likely ahead, that tighter credit will have only a mild effect on growth but that he sees slower consumer spending growth through year-end. The labour market is strong and wage inflation is inconsistent with the Fed’s 2% inflation goal, Jefferson added. St. Louis Fed President James Bulla rd meanwhile said that the Fed policy is now at the ‘low end’ of sufficiently restrictive – we can be sure his March ‘dot’ is above the 5.13% median – but that prospects for disinflation are good, though not guaranteed. Earlier Friday (during our time zone) Fed Governor Michelle Bowman said it’s not clear if Fed policy is restrictive enough, that inflation remains much too high and that we may need further tightening if it stays too high, adding that rates need to stay restrictive for ‘some time’. The Fed’s Bostic and Kashkari are due to speak later Monday.

ECB speak out of the G7 meetings in Tokyo included Ignazio Visco who said there was too much uncertainty to predict the future ECB rate path and that a meeting-by-meeting approach was needed, while Bundesbank Chief Joachim Nagel said more ECB rate hikes currently look necessary and might be required after the summer break, with inflation still much too strong and core inflation not expected to slow quickly. And ECB VP Luis de Guindos , in an interview with Il Sole 24 Ore published over the weekend, says that “we have entered the ‘home stretch’ of our monetary policy tightening path …and that’s why we’re returning to normality, to 25-point steps”. He reckons ECB QT has been worth 60-70bps on 10-year government bond yields. Guidos, like Visco, says ECB decisions will now be made on a meeting-by-meeting basis and be data dependent.

As for the Bank of England, chief economist Huw Pill speaking Friday said that inflation has hit a ‘turning point’; and is likely to tumble as the base effects of high energy rises this time a year ago start to fall out of the calculation, but that the risks are that inflation will remain too high, noting there is not much ‘room for comfort’. He failed to give any directional steer on interest rates, noting only that further tightening would depend on the persistence of inflation. Pill’s remarks were seen offering some support for a rates pause in June, though in the money market, pricing for a 25bps hike in June actually lifted from 19bps on Thursday post the hike (to 4.5%) to 21.4bps at the London close. The wages components of the coming week’s UK labour market report will be important in this respect, as well as whether the big drop in CPI in April from favourable base effects (to be reported on May 24) exceeds or falls short of expectations.

Pill’s comments came after Q1 UK GDP was reported at 0.1% – in line with expectations – but with the March monthly number coming in at -0.3% against 0,.0% expected, implying negative economic momentum running into Q2 (hot on the heels of the Bank of England scotching its prior forecasts of a protracted UK recession, saying on Thursday it will now be completely avoided).

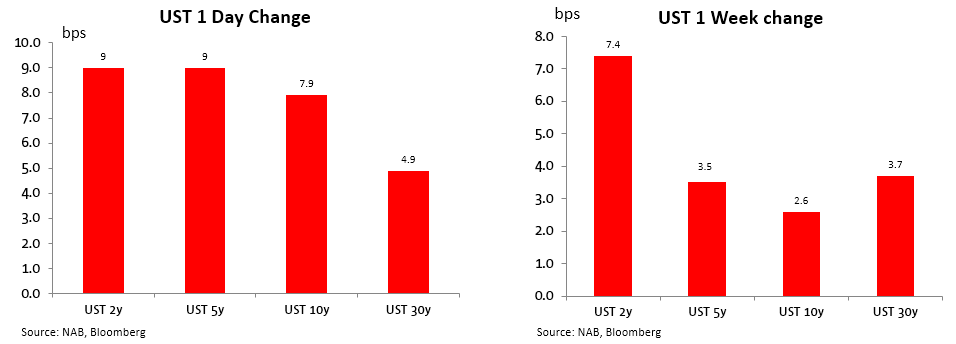

Much of the FX and equity price action Friday was a spill-over from the US Treasury market reaction to the Michigan inflation expectations number, yields out to 5 years jumping 9bps and the 10-year Note by 8bps to 3.46%. On the week, 2s finished up 7.4bps and 10s a lesser 2.6bps, so reversing some of the prior week’s curve re-steepening. European bonds were mostly dragged higher by Treasuries, 10-year Bunds, Gilts and BTPs all up by between 5 and 7bps.

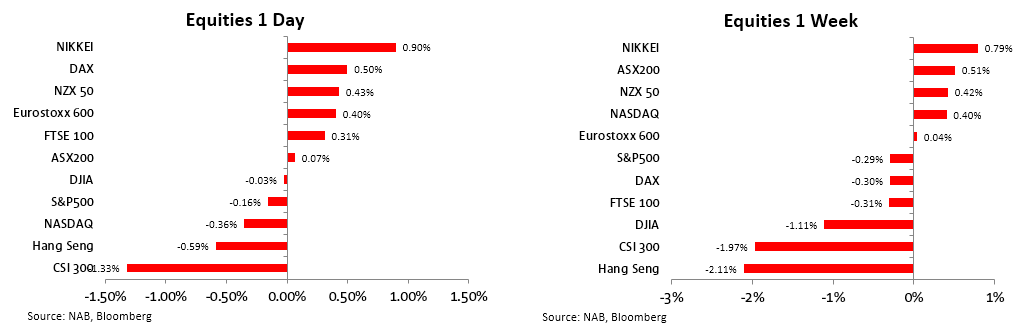

In US stocks , both the NASDAQ and S&P500 lost about 1% from pre-Michigan data levels in the following few hours, before pulling up in afternoon trade to end -0.35% (NASDAQ) and -0.16% (S&P). Earlier European stocks all finished in the green but mostly by no more than 0.5% (Eurostoxx 50 +0.2%). On the week, a very mixed picture, with Shanghai and Hong Kong resuming their underperformance in the face of evidence of faltering economic recovery, Japan and Australia faring best while US equities finished narrowly mixed (NASDAQ down smalls, S&P500 and the Dow both up slightly.

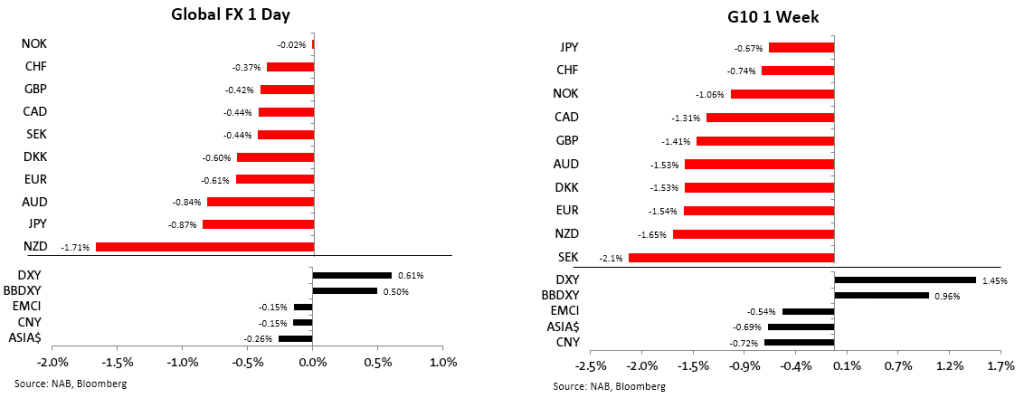

In FX , just as the NZD has been inexplicably strong in the month through Thursday (top of the G10 charts in fact) but which might have been because of Cyclone Gabrielle related insurance flows (we’re only guessing here), on Friday the kiwi displayed all its flightless qualities, NZD/USD slumping by 1.7%, almost 1% more than any other G10 pair. What goes up must come down is about the most intelligent thing we have to say here. AUD/USD also suffered under the higher US yield/risk averse market tone (as slight as the latter was on Friday at least) losing over 0.8% to 0.6646 and closing pretty much on the lows. NOK fared best (flat) despite further slippage in oil prices (WTI and Brent benchmarks off more than 1% ) seemingly still drawing support from last week’s big upside CPI surprise. Friday’s 0.6% gain for the DXY brought its weekly gain to an impressive 1.5% and the broader BBDXY to just under 1%. SEK was the worst performing G10 pair on the week, down over 2%. Perhaps a post-Eurovision victory bounce is in order today?

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.