Coming in for landing in a heavy cross wind

Insight

A quiet start to the week with little in the way of new news or top-tier data.

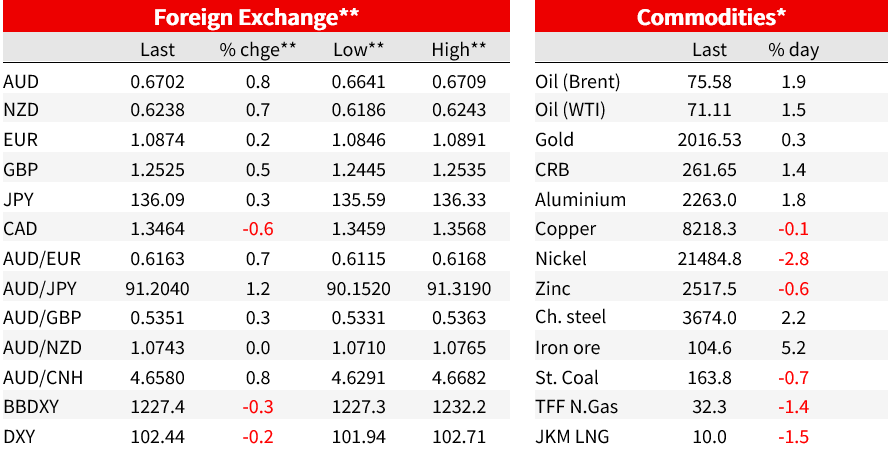

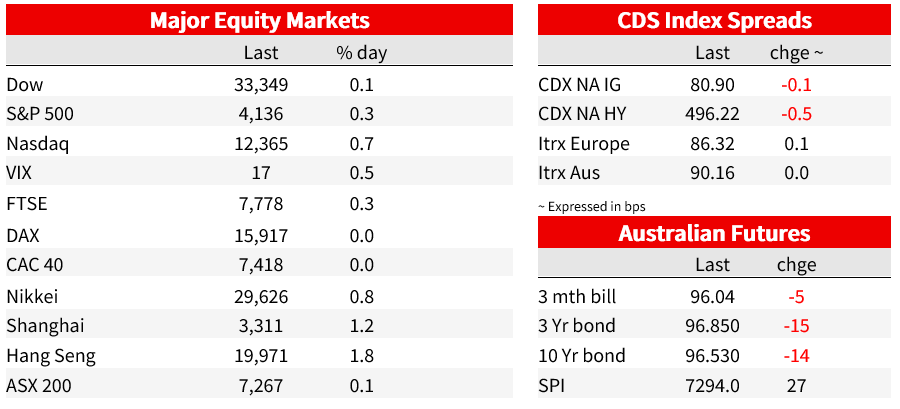

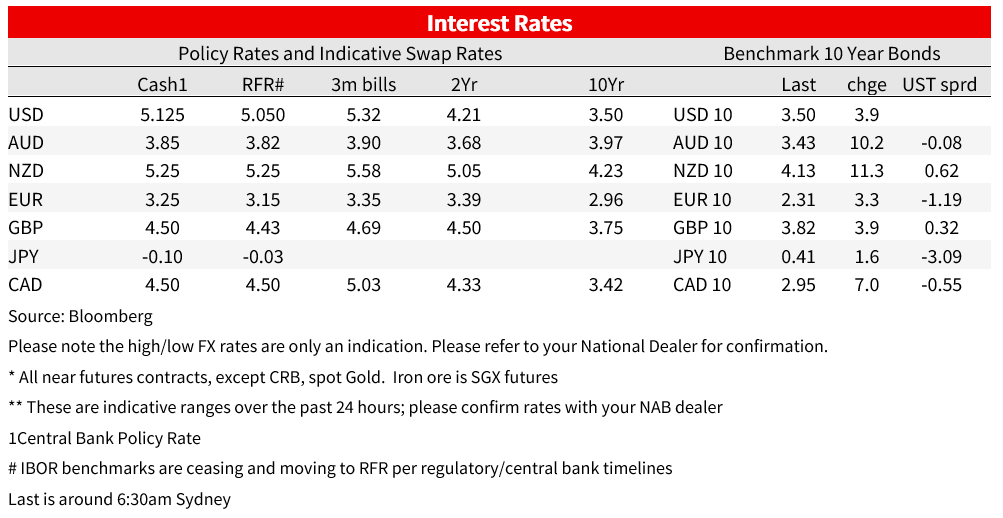

A quiet start to the week with little in the way of new news or top-tier data. The second-tier NY Fed Empire Manufacturing Index missed big (-31.8 vs.-3.9 expected), but given its extreme volatility since January it did not have an enduring impact. Debt ceiling headlines also abound, but with little progress. Fed speak was mixed, while all speakers continue to push back on market pricing for cuts in H2 2023. Meanwhile a surge in corporate issuance (nearly $18bn issued on Monday, and $30bn scheduled for the week) kept pressure on rates. Yields rose with the US 10yr up 3.9bps to 3.50% and 2yr also up 2.3bps to 4.01%. Fed funds pricing inched slightly higher with now a 19% chance of a June rate hike, up from 12.8% yesterday, while there is still around 70bps worth of cuts priced in H2 2023. Equity markets were calm with the S7P500 +0.3%. In oil, the US is reportedly preparing to buy up to 3m barrels to begin refilling its Strategic Petroleum Reserves; WTI oil is up 1.8% to $71.31. The USD meanwhile fell (DXY -0.2%) with strong gains seen in AUD (+0.8%) and NZD (+0.7%). Finally, banks in AU/NZ revised their central bank calls with NAB seeing the RBA at 4.1% and risk of 4.35%, while in NZ this morning WBC sees the RBNZ at 6.0%.

First to Fed speak which was mixed, though all speakers did push back against the market pricing for cuts in H2 2023. Bostic said his “baseline case is we won’t really be thinking about cutting until well into 2024” and that “if I had a bias between going up and going down as our next action, I would say we might have to go up”. Note Bostic seemed to support pausing in June (see CNBC: Interview with Bostic). Goolsbee was more dovish, emphasising the uncertainty around credit conditions and they need to figure out to what extent “credit is doing the work of monetary policy ” on activity and inflation. Goolsbee again cited private sector estimates of the potential impact of tighter credit conditions ranging “from 25bps to 150bps and every in-between” (see CNBC: Interview with Goolsbee). In contrast Kashkari was very hawkish, noting “the labor market is still hot, and we have not seen much softening in the labor market. So, that tells me that we have a long way to go before we get inflation back down”. Rounding out Fed talk, Barkin gave a FT interview where he doesn’t see financial stability concerns as a challenge to higher rates ( FT: Federal Reserve’s Barkin sees ‘no barrier’ to higher rates if inflation persists).

Debt ceiling talks are now a more focal point for markets, though there was little in new development on this front. Treasury Secretary Yellen again re-iterated the 1 June ‘x-date’ for when the Treasury could run out of funds, though the actual date could be a number of days or weeks later than this. President Biden remains optimistic, but overnight Republican House Speaker McCarthy painted a less optimistic picture, stating he thinks he is “far apart” on a debt ceiling solution. This weekend is shaping up to be important with McCarthy also noting: “I think we’ve got to have a deal done by this weekend to have a timeline to be able to pass it in both houses ” – note both chambers of Congress are only scheduled to be in session together for only four days ahead of 1 Jun. In addition, Biden is currently scheduled to fly out on Wednesday for the G7 meeting in Japan but the White House has suggested that his subsequent trip to Australia and Papua New Guinea may be cut if progress on the debt ceiling hasn’t been made. It has been reported that Biden will want significant progress made in the debt limit talks before he leaves out to avoid criticism of him traveling ahead of a potential debt limit breach.

As for data, it was mostly second-tier. The NY Empire Fed Manufacturing Survey missed sharply at -31.8 vs.-3.9 expected. There was little sustained market reaction given the survey has been very extremely volatile of late (since January the survey has gone from -32.9, to -5.8, to -24.6, to +10.8, and now -31.8). The survey write-up noted sharp falls in new orders (-28.0 from 25.1) and shipments (-16.4 from 23.9), reversing the significant increase seen last month (for more details please see NY Fed: Empire State Manufacturing Survey). Across the pond, Euro area Industrial Production also missed sharply in March at -4.1% m/m vs. -2.8% expected. Details though showed almost 3 percentage points of that was driven by a sharp 26% fall in Ireland. The main implication is that Q1 GDP which on the flash was marginally positive at 0.1%, could be revised down later tonight.

In FX, after the strong recovery in the USD late last week, which we thought was driven more by technical and positioning than fundamental factors, a modest reversal has been in play to start the week. Upcoming China activity indicators will be important to see whether that recovery is sustained today. Commodity currencies have outperformed, seeing the AUD up 0.8% from last week’s close to nudge back above 0.67 and the NZD up 0.7% to 0.6235. Other major currency pairs were mostly higher with EUR +0.2%, GBP +0.5, though Yen was weak with USD/JPY +0.3%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.