We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Fed Chair Powell’s speech at Jackson Hole did not break new ground. US equities closed the day in positive territory with both the S&P 500 and the NASDAQ recording their first positive week since July. The UST curve flatten with front end yields ticking higher while the USD closed a tad stronger.

Events Round-Up

UK: GfK consumer confidence, Aug: -25 vs. -29 exp.

JN: Tokyo CPI (y/y%), Aug: 2.9 vs. 3.0 exp.

JN: Tokyo CPI ex-food, energy (y/y%), Aug: 4.0 vs. 4.0 exp.

GE: IFO current assessment, Aug: 89.0 vs. 90.0 exp.

GE: IFO expectations, Aug: 82.6 vs. 83.7 exp.

Fed Chair Powell’s speech at Jackson Hole did not break new ground. The Chair stuck to his guns reiterating the message that the Bank is prepared to lift the funds rate further, if needed, and that policy will remain restrictive until there is convincing evidence inflation is heading toward the Bank’s 2% inflation target. On the latter, amid calls from prominent economists to consider a higher target, Powell was categorical, stating that “2% is and will remain our inflation target.”

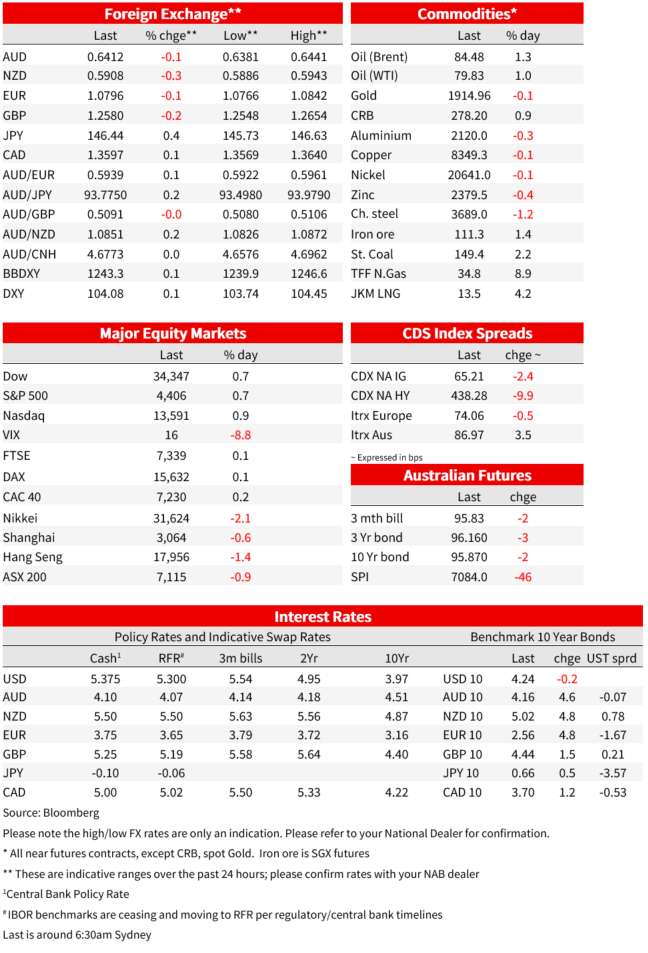

After a short spike in volatility, triggered by Powell’s speech, US equities closed the day in positive territory with both the S&P 500 and the NASDAQ recording their first positive week since July. The UST curve flatten with front end yields ticking higher while the 10y tenor was steady, closing the week at 4.23%. The USD closed a tad stronger across the board, but notably both the AUD and CNY were unchanged on the week while GBP and JPY were the notable weekly underperformers.

Whilst determined on his quest to bring inflation to heal, Fed Chair Powell offered a cautiously optimistic assessment of the inflation outlook. Powell noted “The lower monthly readings for core inflation in June and July were welcome” but then warned that “We can’t yet know the extent to which these lower readings will continue or where underlying inflation will settle over coming quarters.”.

The Fed chair also noted that restrictive policy should show on further decline in goods inflation while housing services inflation (mostly rent, more than 40% of the core CPI and nearly a fifth of the core PCE) should decline toward its toward its pre-pandemic level. But again, he cautioned that additional evidence of persistently above trend growth could put further progress in pulling down inflation at risk and could warrant further policy tightening. Powell then noted that there is still a great deal of uncertainty on the outlook for core services inflation ex housing , remarking these components are “…relatively labor intensive, and the labor market remains tight”. Thus, although the Fed expects the labour market to continue to rebalance, evidence that the tightness here is no longer easing could also call for a monetary policy response.

Overall Powell’s speech essentially reiterated the Fed remains data dependent and will proceed carefully from here , if the data continues to show an ease in labour market tightness and price pressures, then the Fed is likely done with its tightening cycle. If the data doesn’t play ball, then further tightening should be expected. Thus, upcoming key market data releases (inflation and labour market) are likely to set the tone for markets over coming months.

ECB Lagarde speech at Jackson Hole was the other major event to watch and like Powell the President did not deviate much from previous rhetoric. Activity readings in the eurozone have taken a turn for the worse with many wondering whether the softer data could be a trigger for the ECB to soften its stance. Not yet it seems, Lagarde acknowledged Europe is enduring an “era of uncertainty”, but then noted central banks need to provide an anchor for the economy and ensure price stability in line with their respective mandates. Hence, for the ECB this mean setting interest rates at a restrictive level to achieve a timely return of inflation to our 2% medium-term target.

BoJ Governor Ueda was yet again the odd one out, defending the Bank’s ultra-easy policy . Ueda noted that “underlying inflation is still a bit below our target of 2%, adding that Japan’s core CPI (excluding fresh food), printed at 3.1%yoy in July and the rate “is expected to decline toward the end of the year”. On Friday, the Tokyo CPI for August (a reliable leading indicator for the national gauge) printed at 2.9%yoy down from 3.2%, but the core-core reading (ex-fresh food and energy) was unchanged at 4%yoy, potentially challenging Ueda’s expectations for an ease in inflationary pressures over coming months. As for economic growth the Governor noted that “We think domestic demand is still on a healthy trend, although that’s something that needs to be checked with” third-quarter data. Ueda made no reference to JPY but given unwavering support to the Bank’s ultra-easy policy, the currency is likely to remain at the mercy of US rates dynamics.

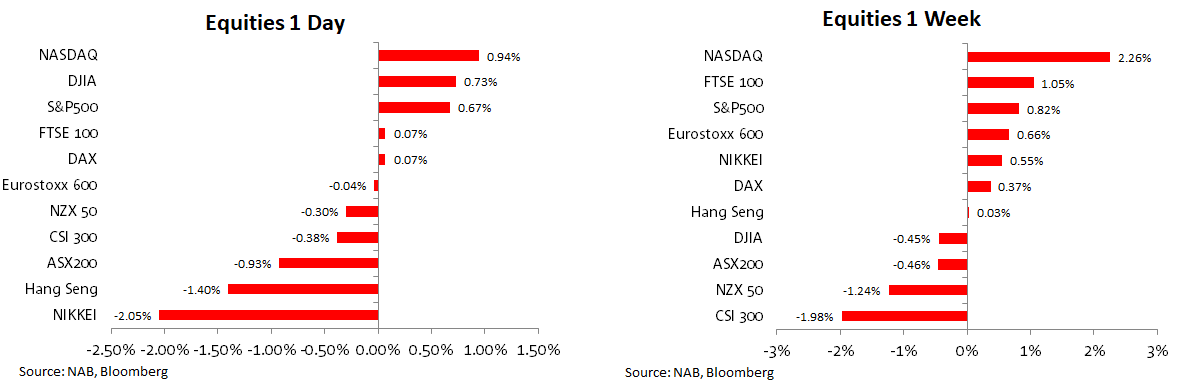

Looking at equity markets performance in more detail. Powell speech only elicited a short-lived spike in volatility. On the day the S&P 500 climbed 0.7% while the NASDAQ was 0.94%. Gains on Friday helped both equity indices record their first weekly gain since July, 0.86% and 2.26% respectively . Meanwhile European shares had a subdued Friday with both the EuroStoxx 600 and UK FTSE 100 little changed on the day, but on the week both indices managed to record gains, up 0.66% and 1.05% respectively.

As for stocks specific news, Boeing shares gained 2.8% after Bloomberg reported the manufacturer is preparing to restart delivery of 737 Max jets to China for the first time in four years. on the week after touching an all-time high earlier this week. on the week ending a record 11-day losing streak.

During our afternoon on Friday, China unveiled a new round of property stimulus, but the positive impact on its domestic equity market was short lived . Beijing is proposing that local governments can abandon a rule that disqualifies people who’ve ever had a mortgage – even if fully repaid – from being considered a first-time homebuyer in major cities (first home buyers can access lower mortgage rates). The government also plans to extend the personal income tax rebates for people who buy new homes within one year after selling old homes till the end of 2025. Friday’s announcement followed government initiatives in previous days incentivising financial institutions to buy equities, encouraged companies to boost buybacks, and asked mutual funds to stop selling.

Overall, these piecemeal measures have failed to arrest the CSI 300 decline. On Friday, the index climbed close to 0.3% on the property stimulus news but ended the day down 0.38% and close 2% lower on the week. Investors are still waiting/hoping for a meaningful fiscal stimulus, but for now the economic downturn has not yet been enough to force the government’s hand. Over the weekend China’s released industrial profits stats for July, revealing profits fell 6.7% from a year earlier. For the first seven months of 2023 (YTD figures), profits declined 15.5%, easing from a 16.8% decrease a year earlier.

Equities Performance

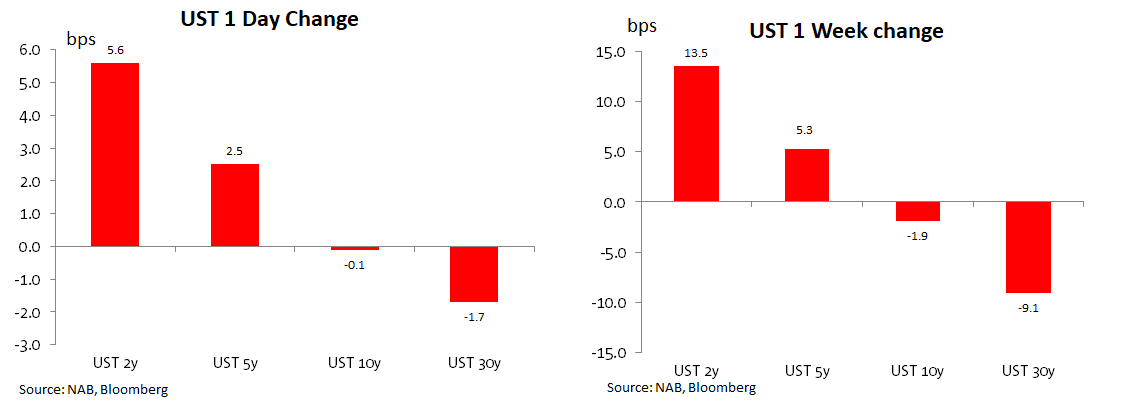

Moving on to rates, the lack of any major surprises from Fed Chair Powell’s speech left market expectations for the Fed funds rate path little changed. Market pricing for the September FOMC was little changed with a near 20% chance of a 25bps hike with a cumulative 15bp of tightening priced for the next 2 meetings. The UST curve flattened on the day, primarily driven by an uptick in front end yields. The 2y tenor gained 6bps to 5.08% while the 10y Noted closed the week little changed at 4.24%. A flattening bias was also evident on the weekly changes with the 2y note up 13.5bps on the week while the 10y note was 2bps lower relative to levels a week ago.

European yields closed higher on Friday, but lower on the week. 10y Bunds gained 4.8% bps to 2.56% while 10y UK gilts climbed 1.5bps to 4.44%. the latter was the big mover on the week, down 23.4bps. The OIS market in Europe is pricing 8.5bps of ECB hikes for next month and a 3.92% peak by year-end while 65bps of rate cuts are priced next year compared to 71bps on Thursday.

US Treasuries over the past week

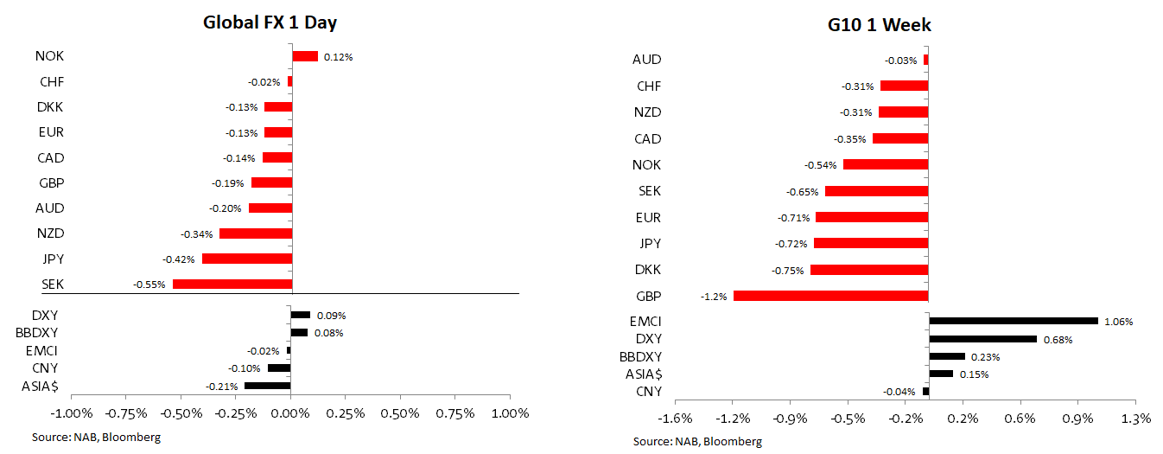

Like the equity and rates markets, Powell’s speech triggered a short-lived spike in FX volatility with the USD briefly falling on the speech, recovering sharply, and ending the day a tad stronger. In index terms BBDXY and DXY gained ~0.09% on the day and for the week climbed 0.23% and 0.68% respectively.

Looking at G10 pairs, JPY was the notable underperformer within the majors on Friday with the move up in short-dated UST yields the main factor. USD/JPY close the week at ¥146.44, printing an intraday high of ¥146.63, a level not seen since November last year. Hawkish remarks from Lagarde failed to support the Euro with the pair closing Friday 0.13% lower on the day and now starts the new week sub 1.08 (1.0796 as I type).

The AUD/USD traded to an overnight low of 0.6381 post Powell’s speech, but then recovered a little bit of ground, opening the new week at 0.6406. In a similar pattern NZD/USD slipped below 0.5900 to make fresh lows for the year before recovering into the weekly close and now starts Monday at 0.5902.

The latest CFTC currency futures positioning data, reveals that the speculative community have been selling Australasian currencies, likely related in part to weak activity in the Chinese economy. Of note however looking at G10 performance for the week, the AUD sits at the top of the leader board, essentially unchanged over the past week, CNY is also unchanged notwithstanding weak domestic data releases over the past week. Maybe all the bad China are already in the price? Meanwhile GBP was the big weekly underperformer as the market reassesses the BoE rates outlook following a string of soft data releases.

FX Performance

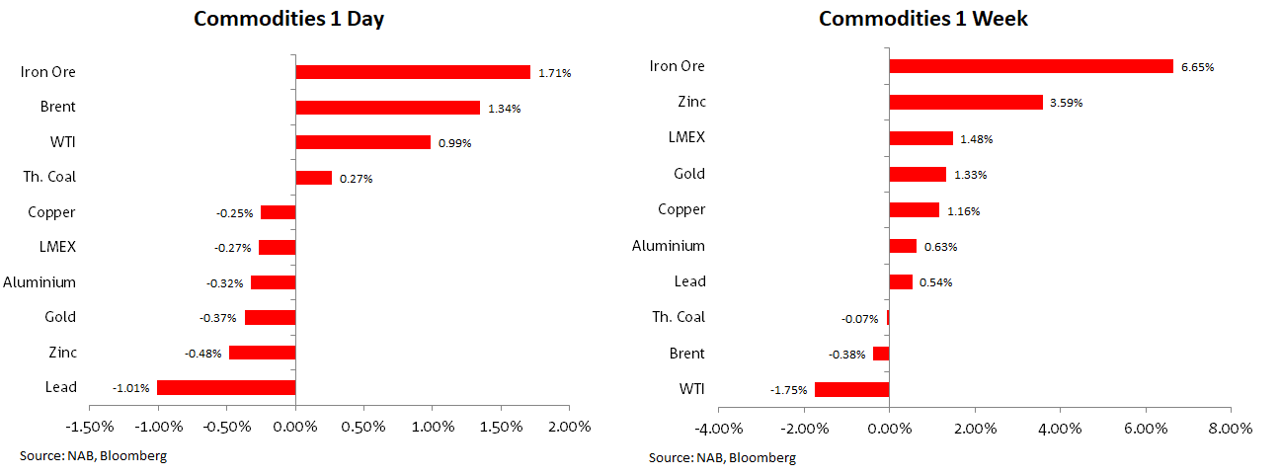

Moving onto commodities, iron ore was the top performer on Friday (+1.71%) and on the week (6.65%). Oil prices also gained on Friday (WTI 0.99%, Brent 1.34%), but were softer over the past 5 trading days. Meanwhile European natural gas prices rebounded (8.89%), trimming their first weekly drop this month, with traders weighing further labour talks in Australia and heavy maintenance in Norway.

Commodities Performance

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.