Online retail sales growth slowed in May following a fairly strong April

Insight

US equities struggled for direction on Friday, ending the day marginally lower. After a choppy session, UST yields closed higher across the curve with the USD broadly weaker, ending a three-day winning streak. Debt impasse did not helping sentiment while Fed Chair Powell expressed a bias for pausing rate hikes in June.

Events Round-Up

NZ: Trade balance (ann $b), Apr: -16.8 vs. -16.7 prev.

UK: GfK consumer confidence, May: -27 vs. -27 exp.

JN: CPI (y/y%), Apr: 3.5 vs. 3.5 exp.

JN: CPI ex fr. food, energy (y/y%), Apr: 4.2 vs. 4.1 exp.

CA: Retail sales ex auto (m/m%), Mar: -0.3 vs. -0.8 exp.

The positive debt ceiling vibes lasted about 24 hours, hopes of an imminent deal were dashed with McCarthy negotiators walking out on the talks on Friday. Fed Chair Powell expressed a bias for pausing rate hikes in June while US Treasury Secretary Yellen warned more bank mergers may be needed. US equities struggled for direction ending the day marginally lower and after a choppy session, UST yields closed higher across the curve. The USD was broadly weaker on Friday, ending a three-day winning streak. Over weekend Biden and McCarthy agreed to resume talks and China barred Micron chips, escalating tensions with the US.

Debt ceiling negotiations came to an unexpected halt Friday morning following Republican’s frustrations at the lack of progress on spending caps. McCarthy negotiators walked out of the talks with the House Speaker, who was not at the meeting, blaming President Biden for the lack of progress. Hours later, McCarthy announced Republicans were returning to the negotiating table, but discussions once again ended with an impasse.

According to the New York Times, Republicans appeared particularly discouraged by what they said was White House officials’ refusal to budge on how strictly to cap federal spending. While the Washington Post noted GOP leaders have said they will not support a bill that funds the government at higher levels next year than this year, as lawmakers could decide to reverse any caps on future growth in later years. Over the weekend McCarthy said that the impasse was unlikely to be resolved while the president was still overseas. Then late on Sunday, the two parties agreed to resume talks (have we not seen this movie before?) with President Biden and McCarthy set to meet on Monday. Speaking over the weekend and adding urgency for a resolution, Treasury Secretary Janet Yellen said the US is unlikely to reach mid-June and still be able to pay its bills,

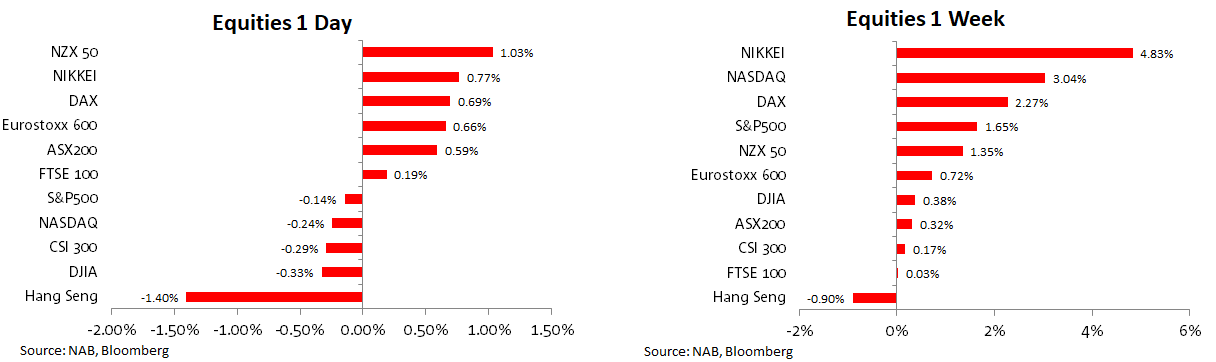

News of a breakdown in the negotiations on Friday weighed on risk sentiment with the S&P 500 losing almost 0.8% from its high of Friday’s session, although in the end the index closed marginally lower at -0.14% while the NASDAQ was -0.24%.

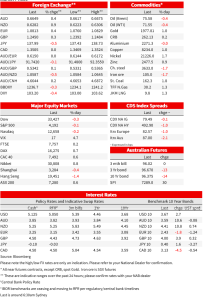

Looking at major equity indices performance over the week, the NIKKEI led the gains up 4.83% while the NASDAQ was 3.04% followed by the S&P 500 at 1.65%. The Eurostoxx 600 gained 0.72% our ASX 200 was 0.17% while China’s CSI was 0.17%.

One take away from the weekly price action is that equity investors remain bullish notwithstanding Debt ceiling concerns and US regional banking struggles. Speaking on Friday, US Treasury Secretary Janet Yellen warned that there may be a need for more bank mergers ahead, a reminder that regional banks are not yet out of the woods and still have the potential to rattle markets ahead. Yellen comments weighed on reginal banks on Friday with the KBW Regional Bank Index closing 2.14% lower on the day. That said on the week the index gained 6.19% with Western Alliance Bancorp positive deposit news halfway through the week the main factor for the weekly gains.

Sticking with bank news, on Friday Fed data revealed that deposits at commercial banks decreased by $26.4bn in the week ended May 10 to $17.1trn. That was a third weekly decline in a row as customers continue seeking higher returns in money-market funds. Lending was little changed.

After a week where different Fed speakers voiced their support for further rate hikes while others expressed a preference to pause. On Friday Fed Chair Powell expressed a bias to pause the tightening cycle at the next meeting in June. Speaking at a Fed conference in Washington the Chair noted that “ We’ve come a long way in policy tightening and the stance of policy is restrictive and we face uncertainty about the lagged effects of our tightening so far and about the extent of credit tightening from recent banking stresses,” adding that “Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments,”

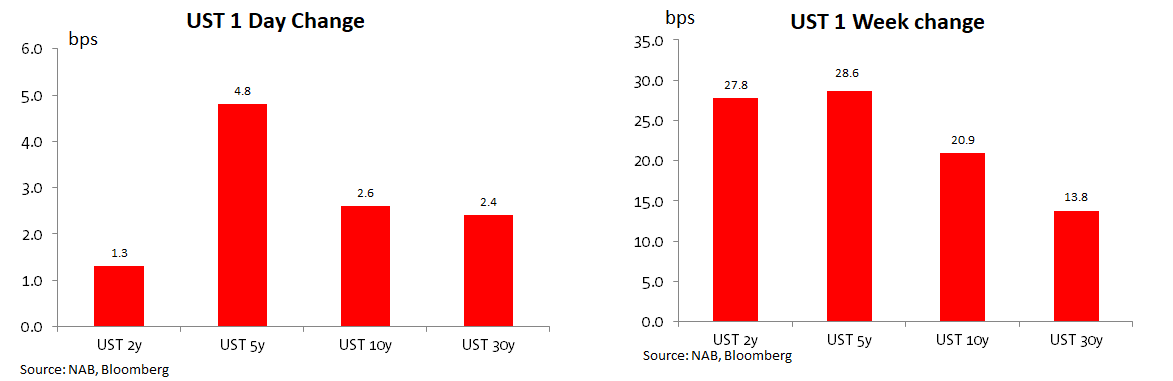

US Treasuries yields endured a choppy session on Friday, after rising in the previous days amid positive debt ceiling soundbites. Yields lost altitude during our APAC Friday session, then rose during the European and early US session. The combo of news from Debt ceiling impasse, Yellen banking concerns and Fed Chair remarks drove yields lower with a partial reversal before the close.

In the end UST yields closed Friday higher across the curve with the moves led by the belly of the curve. The 5y Note gained 5bps to 3.733% and after trading in a 3.6137% to 3.719% daily range, the 10y Note closed the week 2.6bps higher on the day at 3.6726%. Fed Chair’ remarks also triggered a pairing in rate hike expectations for next month with the market now pricing an 18% chance of a 25bps hike compared to 38% in the previous day.

Earlier in Europe, 10y Bund yields fell after briefly rising to 2.50% for the first time since April 24. 10y Bunds closed at 2.423%, 2bp lower on the day. Of note, and following some speculation of an imminent downgrade, after the close Moody’s Investors Service confirmed that they have no plans to issue a report on Italy’s rating. The news means that Italy won’t be losing its investment-grade status just yet, although the rating remains in perilous territory.

Looking at the weekly charts, core yields are higher across the board with AU bond futures leading the move, up around 30bps over the past 5 day (closing NY at 96.3810 – yield of 3.6250). 10y UST yields climbed 20bps with 10y Bunds up 15bps. Data releases over the week support the notion of economic resilience, pushing yields higher and delaying expectations of Central bank rate cuts ahead.

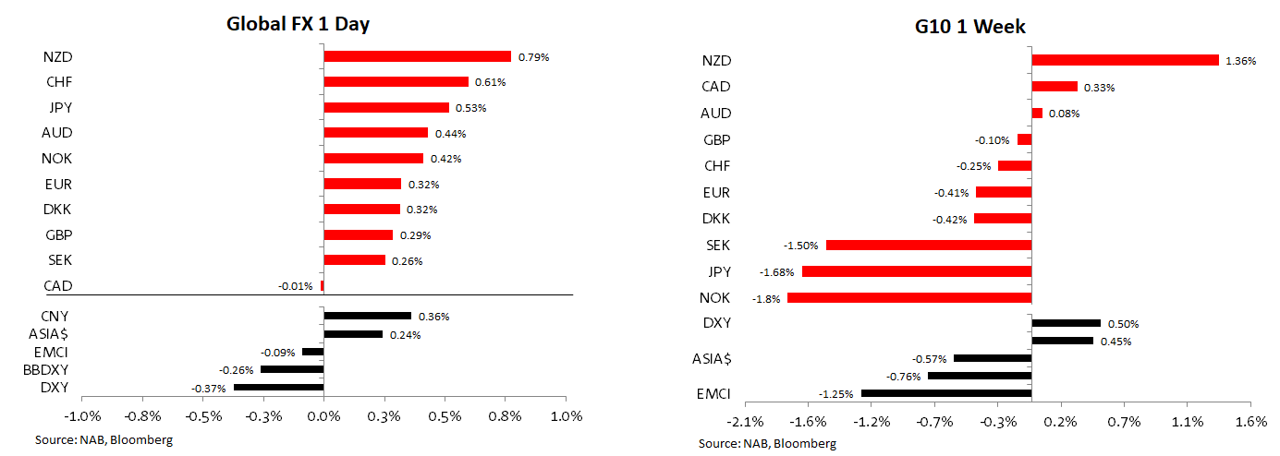

After trading higher in the previous three days, the USD lost altitude on Friday. Debt ceiling news didn’t help the greenback while Fed Chair Powell’s remarks and subsequent impact on Fed pricing also weighed a little . The BBDXY and DXY indices retreated 0.37% and 0.26% on the day, but on the week both indices ended higher (~ +0.5%).

Looking at G10, NZD was the top performing gaining around 0.8% on the day with most of its appreciation coming during the overnight session . The kiwi ended the week at 0.6275, after briefly trading to an overnight high of 0.6306. Over the past week and ahead of the RBNZ meeting this week, the market has increased expectations for a rate hike climbing from 18bps on Monday to 33.9bps on Friday, up 5bps on the day.

The AUD also performed against the USD on Friday, up 0.44% and closing the week at 0.6651 . Over the weekend Australian Employment Minister Tony Burke strongly backed an increase in the minimum wage that matches inflation, arguing the lowest-paid workers couldn’t afford a further erosion of their living standards while dismissing the risk of a wage-price spiral. The RBA has noted in the past how Australia has been different to other economies in this cycle with a relatively more subdued wages growth, but the market remains aware of the risk that a high minimum wage could sets a benchmark for other wage agreements.

The USDCNY was another notable currency mover on Friday with the CNY the gaining as much as 0.5% to 7.0121 following comments from the PBoC and FX regulator noting that they will “strengthen market expectation guidance and take actions to correct pro-cyclical and one-way market behaviours, when necessary,”. The announcement was surprising given recent daily fixing suggested the PBoC was willing to tolerate CNY weakness vs the USD.

Looking at the majors, the move up in UST yields supported USD/JPY with the pair trading down sub ¥138, opening the new week at ¥137.98 (JPY +0.5%). The euro edge up back above 1.08 (+0.35%) with hawkish remark from ECB Lagarde offsetting the move lower in core European yields. Lagarde noted that ‘We have to really buckle up’ on achieving 2% inflation goal adding that the ECB needs to keep persevering with its monetary policy just as consumer-price growth shows signs of slowing. GBP also managed to make inroads against the USD with the pound closing the week at 1.2446, up 0.3% on the day.

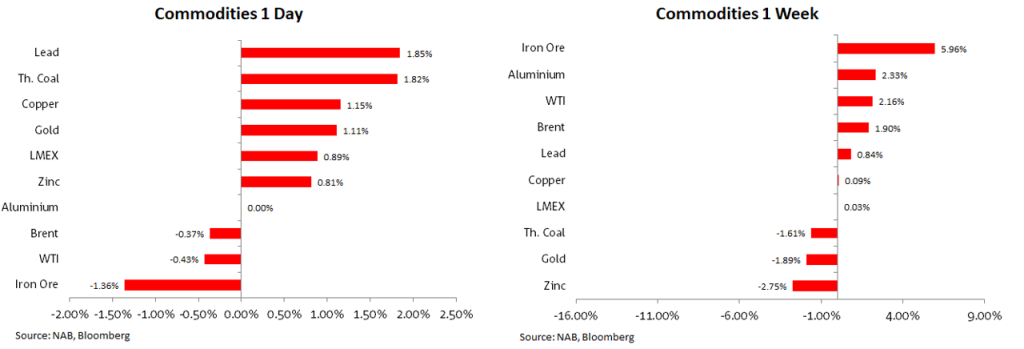

Oil prices struggled on Friday with both Brent and WTI down close to 0.4%. Debt ceiling headlines seemingly providing a source of volatility while the market continues to digest implications from sharpest weekly decline in US oil rigs since Sep’21. Iron Ore fell 1.36% on Friday but was the best performing commodity on the week up 6% to $105.0m, the bulk commodity continues to show a great deal of sensitivity to China economic stimulus news. Copper gains 1.15% on the day but was unchanged on the week. Gold gained 1% on Friday but was down 1.78% on the week.

Lastly early this morning, China-US Semiconductor tensions have escalated yet again with China announcing the banning of Micron Chips , noting that Micron Technology products ( a US company) had failed to pass a cybersecurity review and that the components caused “significant security risks to our critical information infrastructure supply chain,” which would affect national security.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.