NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Still no sign of breakthrough on US debt ceiling talks, souring risk sentiment.

And Vale Tina Turner, who has sadly passed away at the age of 83

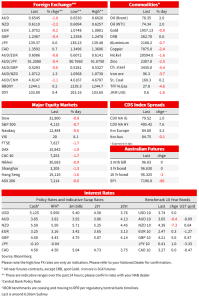

US stocks are down for the second day running with no signs of a debt ceiling deal in Washington and the clock ticking louder ahead of the ‘X-date’ which Treasury Secretary Yellen has reaffirmed to be June 1 on current calculations. This has sen the yield on US Treasury Bill maturing on 1 June jump to 7% the USD is back with safely bid alongside slightly higher US treasury yields. The NZD has extended its onshore slump following the RBNZ’s signal yesterday it thinks it’s now done on the OCR at 5.5%, while sizeable knee jerk gains for GBP after much worse than expected CPI figures and associated BoE repricing have not held, the growth implications of Bank Rate lifting to above 5% seemingly taking a toll. AUD/USD meanwhile, initially suffering in the slipstream of the weaker NZD, has seen losses accelerate after the 0.6565 year to date low was taken out. The 0.6530 o/n low is the weakest since 10 November 2022.

FOMC Minutes have been released in the last couple of hours and reflect the somewhat divided nature of much of the post-May meeting commentary from an array of FOMC officials. “Some” officials saw additional tightening as likely warranted, while “several” figured it may be time to stop hiking. Those advocating for the Fed to not be done at the current 5.0-5.25% do seem open to at least a pause in June though, citing concerns about how much tightening is in train from the banking sector and which will be tightening monetary conditions. One standout sentence in the Minutes supporting the need for still tighter policy was that nominal wages growth, even after accounting for the trend productivity growth, was running ‘well above’ what’s consistent with the 2% inflation goal.

Fed Governor Waller, speaking ahead of the Minutes, and who sits at the more hawkish end of the spectrum, said that he didn’t support stopping rate hikes until “we get clear evidence” that inflation is moving down towards 2% but added “whether we should hike or skip at the June meeting will depend on how the data come in over the next three weeks”.

No significant US data overnight, while the German Ifo business climate index headline dropped to 91.7 from 93.4, with the current assessment index easing a little to 94.8 from 95.1 and the expectations measure falling back to 88.6 from 91.7. All of this reflecting the picture from the prior day’s PMIs and which highlighted the current weakness of the German manufacturing sector at the moment, and where latest trade numbers highlight the softening in export growth – particularly to China. IFO’s President noted that “the mood in the German economy has taken a significant hit”.

The other big European economic news yesterday and just before our local market ended the day, was for UK inflation. May CPI far exceeded expectations, headline only dropping to 8.7% from 10.1% (on favourable energy price base affects) against 8.2% expected while more disconcerting, the core reading lifting to 6.8% from 6.2% against no change expected (this measure excludes food, energy, alcohol and tobacco). Particularly disappointing, food and non-alcoholic beverage inflation held above 19% last month (19.1% from 19.2%).

Speaking after the release, BoE Governor Bailey denied that the UK was suffering from a wage-price spiral but he noted the “stickiness” of inflation. Another full rate hike was priced into the curve for this year, with the chance that the BoE might step up to a 50bps hike at the next meeting. The curve prices in another 90bps or so of hikes that would take Bank Rate to between 5.25-5.5% later this year. UK 2-year gilt rose 23bps to 4.33% and the 10-year rate 6bps to 4.21%.

As for the RBNZ, while the 25bps hike to 5.5% was widely anticipated, what surprised the market was the RBNZ’s outlook, which was consistent with the end of the tightening cycle being reached – the MPC now “confident” that policy was restrictive enough to meet its inflation objective. The Bank wasn’t particularly perturbed by possible inflation consequences of the expansionary Budget (Governor Orr insisted it is actually contractionary) nor the recent steep lift in net migration (which he views as adding to (labour) supply, notwithstanding any positive demand implications). These were two factors which had prompted the market to consider that the RBNZ would likely revise up its projected peak in the OCR. Adding to the dovish overtones, two of the seven members voted to keep policy unchanged. Governor Orr is speaking to a parliamentary committee right now, noting that interest rates are restrictive (‘well above’ neutral) with economic growth and inflation weaker than expected (the fall in Q1 retail spending clear evidence of this – our parenthesis)

And as for the RBA, the AFR’s Phillip Coorey writing yesterday evening last night says Reserve Bank of Australia governor Philip Lowe has left federal MPs in little doubt he is not done lifting interest rates, after telling them he had no tolerance for lingering high inflation and would do what he believed needed to be done to bring it down. Dr Lowe delivered the message yesterday to members of parliament’s economics committee in a briefing that multiple sources described as pessimistic. “He stressed that he doesn’t have any tolerance for (high) inflation lasting for a long time, and he will do what he believes needs to be done, “ Coorey writes.

Market wise, lack of progress on the debt ceiling has soured equity market sentiment for the second day running, the S&P500 ending Wednesday down 0.7% and the NASDAQ -0.6%. All bar one of the eleven S&P sub-sectors finished in the red, led by a 2.2% decline in Real Estate (energy the exception, boosted by crude oil up as much as $1.50). Post close Nvidia, benefiting from the AI craze, reported Q1 earnings $0.66bn above its street estimate but projects Q2 revenue of $11.0bn +/- against an estimate of just $7.1bn. Its stock is up close to 20% after hours.

In FX the USD is stronger across the G10 board (DXY +0.4%), gains led by the 2.2% loss for the NZD, so extending its post-RBNZ crunch lower by the best half of half a cent. AUD/USD was dragged lower by the NZD, as is often the case when one of the antipodean currencies makes a big move, but the break of the 0.6565 YTD low, together with USD/CNY seemingly establishing a firmer foothold above 7.0, have further weighed overnight to produce a low of 0.6530 (weakest since 10 November 2022). Of some note, GBP failed to hold its post-CPI bounce, ending in New York -0.4%. The growth implications of BoE rates potentially headed above 5% is evidently weighing, while the weaker IFO survey took a small bite out of the EUR (-0.2%).

US treasury yields are finishing up in New York with 2s up 6bps and 10s 5bps. Eurozone bond ended not much changed, in contrast to gilts where the 2-year jumped more than 20bps post the CPI data.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.