Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

US equities were higher on Friday as hopes grew of a debt ceiling deal, ahead of news on the weekend that an agreement in principle had indeed been found. US data was strong and Fed tightening expectations firmed.

NZ: ANZ consumer confidence, May: 79.2 vs. 79.3 prev.

JN: Tokyo CPI (y/y%), May: 3.2 vs. 3.4% exp.

JN: Tokyo CPI x-fr.food, energy (y/y%), May: 3.9 vs. 3.9 exp.

AU: Retail sales (m/m%), Apr: 0.0 vs. 0.3 exp.

UK: Retail sales ex auto fuel (m/m%), Apr: 0.8 vs. 0.4 exp

US: Personal income (m/m%), Apr: 0.4 vs. 0.4 exp

US: Real personal spending (m/m%), Apr: 0.8 vs. 0.5 exp

US: PCE core deflator (m/m%), Apr: 0.4 vs. 0.3 exp

US: PCE core deflator (y/y%), Apr: 4.7 vs. 4.6 exp

US: Goods trade balance ($b), Apr: -96.8 vs. -85.9 exp

US: Durable goods orders (m/m%), Apr: 1.1 vs. -1.0 exp

US: Durables ex transport (m/m%), Apr: -0.2 vs. -0.1 exp

US: U. of Mich. cons. Sentiment, May: 59.2 vs. 58.0 exp

It was a positive tone for equities on Friday as hopes grew that negotiators were nearing a deal on the US debt ceiling. News on Saturday night (US time) was that those hopes were well founded, with an in-principle agreement struck, though the deal still has to make its way through Congress. The relief over the tentative deal will be met with thin markets to start the week with US and UK markets both closed on Monday, though US Treasuries futures and S&P500 Index futures will trade. Outside of the debt ceiling developments, US data on Friday showed stronger-than-expected consumer spending and faster-than-expected core inflation. Fed pricing moved higher and the US yield curve flattened.

The major news over the weekend was an in-principle agreement on the debt ceiling reached by President Biden and Speaker McCarthy . Improving hopes of a relatively orderly lift to the debt ceiling ahead of the x-date should boost risk sentiment into the start of the week, though the deal still needs to pass both chambers of Congress. McCarthy said a vote in the House could come on Wednesday. Biden and McCarthy both voiced confidence that their tentative deal will pass. Giving only a little breathing room for the passage of the bill was Friday’s updated 5 June estimate for X-date from Treasury Secretary Yellen. The deal would raise the debt ceiling for 2 years, until after the 2024 presidential election. Reports are that the deal would keep non-defence spending roughly flat in the 2024 fiscal year, increase it by just 1% in 2025, but contain no further caps after that. In terms of the fiscal impulse, that would be a relatively small change from the status quo, and a smaller drag than earlier negotiation positions. Republicans once demanded steep spending cuts and Democrats proposed tax increases.

US data on Friday showed the core PCE deflator up 0.4% m/m, a tenth higher than the 0.3% consensus. Despite faster-than-expected price rises, real consumer spending was up 0.5% m/m against 0.3% expected , helped by a surge in vehicle sales. The core PCE deflator continues to show little progress on the current phase of the inflation fight. In 3m-annualised terms the core PCE deflator is 4.3%, the same rate it was a year ago in April 2022. The core-services ex housing measure the Fed is watching was up 0.4% m/m and 4.9% 3m-annualised. Looking only at ‘market’ core services ex housing which excludes imputed components offers a little more hope that there is slowing recently, but you have to look hard at the data to find it. In other data, but very much second tier relative to PCE, the final U of Mich. Consumer Sentiment was revised up slightly to 59.2 from 57.7 and the bounce in the 5-10yr inflation expectation to 3.2% reported in the preliminary was pared to 3.1%, still up from 2.9% in March, but within its recent ranges.

The combination of stronger spending and faster price increases boosted bets that the Fed will be raising rates in June. Speaking after the data, the Cleveland Fed’s Mester said “Everything is on the table in June” and that “ the data that came in this morning suggests we have more work to do.” Markets now price a 69% chance of an increase, from around 50% a day prior and just 18% a week ago, with an increase by July now more than priced. While the debt ceiling has been dominating headlines, Fed hike expectations have been firming. May Payrolls on Friday and May CPI on 13 June are the key data ahead of the 14 June meeting. Just 7bp of cuts (from current levels) are now priced by year end, the year-end implied fed funds rate at 5.0% has risen more than 25bp over the week. Stronger data and fading tail risks from the banking sector stress have underpinned the change in Fed outlook.

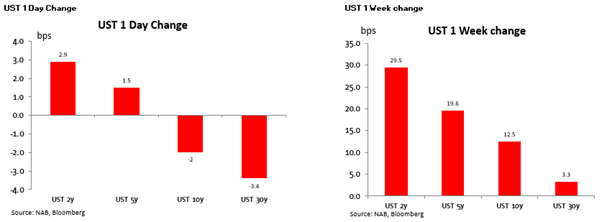

US short end yields were higher and curves flatter on Friday. The 2yr yield rose 3bp to 4.56% while the 10yr fell 2bp to 3.80%. Over the week, US 2yr yields rose 30bp, while the 10yr rose 13, seeing the 2s10s spread widen to 77bps, the deepest inversion since before the banking ructions in early March.

In Europe, German Bund yields rose 11bp to 2.54%, while the chunky upside surprise to UK CPI on Wednesday saw a larger selloff in Gilts. The UK 10yr yield some 34bp higher over the week at 4.33%, despite a 4bp drop on Friday. The policy-sensitive 2yr yield is up over 50bps at 4.48%, compared to the high of 4.68% briefly touched in September after the Truss-Kwarteng mini-budget. UK Retail Sales ex fuel on Friday showed a 0.8% m/m gain in April, higher than the +0.4% expected, but countered by a March downward revision to -1.4% from -1.0%.

Locally, news over the weekend were more reports in the AFR from RBA Governor Lowe’s briefing of politicians last week. An anonymous source said the Governor had been more strident on the inflationary impact of wage rises that aren’t accompanied by productivity increases. ( RBA interest rates: Governor Philip Lowe warns Labor over wages (afr.com)). Governor Lowe appears publicly before the Senate Economics Committee on Wednesday

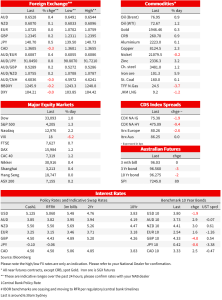

On Friday, US equities were higher, buoyed by reports negotiators were nearing a debt deal. The S&P500 was up 1.3%, with the Nasdaq again outperforming, up another 2.2% on Friday to be up 2.5% over the week . The week was a tale of two halves for equity markets, with risk assets out of favour in the first half of the week and the S&P500 down around 2.6% by mid Wednesday before the AI and tech surge, and relief on signs of debt ceiling progress, turned fortunes around. The S&P500 was 0.3% higher over the week. While Thursday’s equity market gains were very narrowly based in AI-related tech, Friday’s were broader with 8 of 11 S&P500 sectors in the green. Meanwhile the KBW Regional Banking index is showing signs of stabilisation having made two consecutive weeks of gains and is currently 11% above the lows from earlier in the month.

The WSJ notes the largest divergence between large and small cap companies since 1997 so far this year. The Russell 1000 index of large companies has gained 9.2% this year, compared to just 0.7% for the small cap concentrated Russell 2000 (Tech Stock Rally Leaves Small-Caps in the Dust – WSJ)

The positive tone for equities on Friday was shared across most markets. In Europe, the Euro Stoxx 50 rose 1.6%, but was still 1.3% lower over the week. The Nikkei was up 0.4% over the week, but Chinese equities underperformed, the CSI 300 losing 2.4%, while the Hang Seng was down 3.6% prior to a Friday holiday.

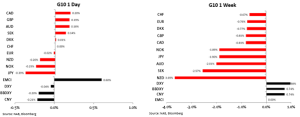

FX moves on Friday were relatively modest on net , the dollar little changed on the DXY at 104.21, having gained 1.0% over the week. The DXY was down as much as 0.4% as hopes of a deal grew before paring losses after the PCE data. Weekly gains in the US dollar were broad-based, and while the currency does seem to have benefitted from debt ceiling angst, a more important driver has been the shifting expectations for the Fed. Indeed, USDJPY rose above 140 as the yen lost 1.9% over the week, towards the bottom of the G10 leader board alongside higher yields. The euro was little changed on Friday and 0.8% lower over the week.

NZD was the G10 underperformer, with a more-dovish-than-expected 25bp hike from the RBNZ on Wednesday catching markets by surprise. The NZD was down 3.7% over the week and the weakest of the G10 currencies by some margin. The AUD is 2.0% lower over the week to 0.6517, having broken its excruciatingly small trading range that had persisted since March to the low side. The AUD did manage a 0.2% gain on Friday, but only after hitting a fresh 2023 low of 0.6491 intraday. The move lower in the NZD and a softer CNY have weighed on the AUD, which having depreciated earlier in the week alongside the broader falls in risk assets, didn’t participate alongside the tech-led bounce higher in equities on Thursday and Friday. The USD gained 0.7% against the CNY over the week and has traded back comfortably above 7. USDCNH climbed for a third straight week, rising as high as 7.0986 on Friday before paring gains amid reports of dollar-selling from Chinese state banks.

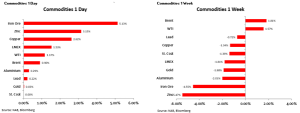

In commodities, oil posted its second weekly gain. Brent was up 1.8% over the week to 76.95. Conflicting statements on the potential for more cuts from OPEC and its allies kept supply dynamics on focus. The Russian Deputy Prime Minister said that OPEC+ wasn’t likely to take further measures in June, contrasting the Saudi Energy Minister earlier in the week who warned that speculators should “watch out.” A rebound in iron ore prices on Friday still left iron ore down almost 5% over the week, weighed by Chinese steelmaking demand .

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.