Total spending grew 0.9% in June.

Northern hemisphere summer holidays and a lack of data has seen markets treading water ahead of US CPI figures on Thursday.

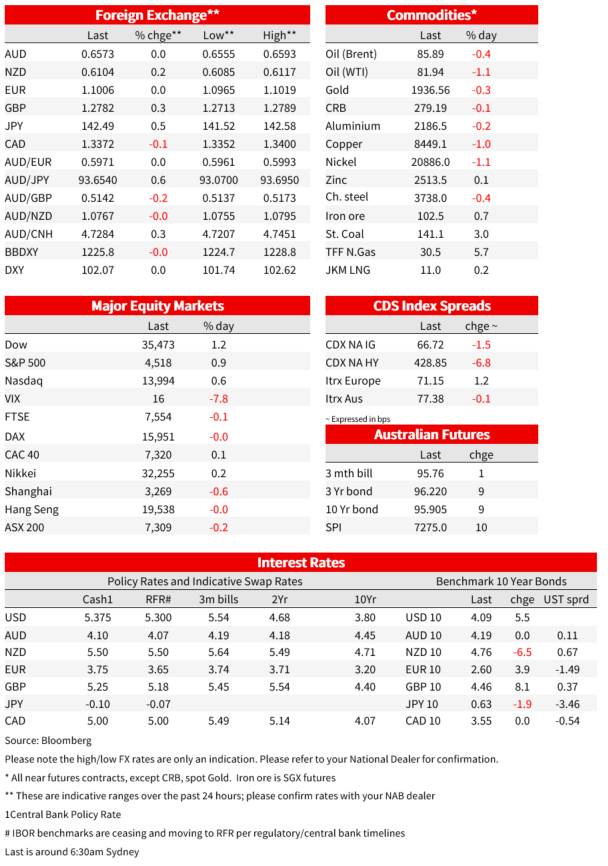

Northern hemisphere summer holidays and a lack of data has seen markets treading water ahead of US CPI figures on Thursday. This week’s Treasury auctions will also likely be closely watched given the increase in planned issuance. Risk sentiment was positive with US equities up (S&P500 +0.9%, following last week’s -2.3%). Global yields rose in APAC and continued overnight, reversing some of the sharp moves seen on Friday post-payrolls. The US 10yr rose 5.5bps to 4.09% (high 4.12%), but is still below the pre-payrolls level of 4.20%. the curve bear steepened with 2yr yields up 2.0bps to 4.78% with the 2/10s curve now at -69.2bps. The USD rose slightly with DXY +0.1% with most majors little moved apart from the Yen (USD/JPY +0.5%) and GBP (+0.3%). The AUD was little moved and currently trades at 0.6572.

The only noteworthy piece of US news overnight was the Fed’s Williams who said whether another rate hike is needed is an “open question”. And in keeping with Powell’s post-FOMC presser, that as inflation comes down and real rates rise “to keep maintaining a restrictive stance may very well involved cutting the federal funds rate next year, or year after, but really it’s about how are we affecting real interest rates — not nominal rates” (see NY Times: The New York Fed President Sees Interest Rates Coming Down With Inflation). The Fed’s Bowman though repeated her weekend remarks that she “ expect[s] that additional increases will likely be needed to lower inflation” (note plural). Markets continue to only price a small 36% chance of another rate hike by November, and thereafter have 140bps worth of cuts by the end of 2024.

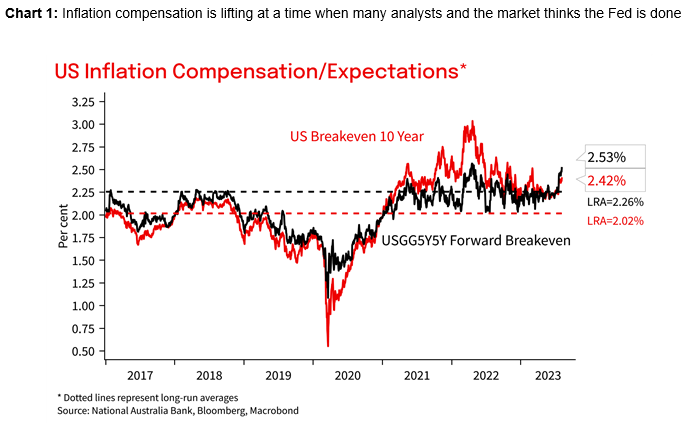

Reflecting on the above Fed comments, until recently the rise in US nominal yields was more reflected in real yields, but more recently inflation compensation has been lifting. Overnight the implied 10yr inflation breakeven rose 4.4bps to 2.42%. Since the end of June, implied breakevens have risen 18.3bps against a 25.2bps move in nominal yields. Other measures of inflation compensation have also risen strongly – 5Y5Y FWD Breakevens now sit at 2.53% and is the highest since April 2022. The market it seems doubts the resolve of the Fed to return inflation to 2% amid the talk of a soft landing and notions the Fed may be done. Something to watch, especially for how Fed officials may react.

Across the pond, German short-term debt was in high demand after the Bundesbank’s late-Friday announcement that it would slash the rate paid on domestic government deposits to 0% from 1 October (currently around 3.45%). Investors flocked to German bills, 2-year notes and other short-term securities, seeing Germany’s 2-year bunds rate down 5bps against a backdrop of higher rates, as the 30-year rate rose as much as 9bps to 2.72%, its highest rate since early 2014. The economic calendar has been light, but Germany industrial production fell by a larger than expected 1.5% m/m in June (-0.5% expected), a second consecutive monthly decline and extending the general malaise for the manufacturing sector.

In other news, analysts are alluding to the risk of a possible US government shutdown after fiscal year-end 30 September, a re-run of 2018-19 and 1995, when federal funding runs out at that date. Unlike the debt-limit fight, a threat of debt default is not at risk, but a government shutdown would result in things like closed government facilities and delays to economic releases. The media report that Republicans are emboldened by the ratings downgrade by Fitch Ratings, to cut spending and bring the deficit under control. For the market, this issue could gather steam just as we head towards the next FOMC policy meeting in late-September, and it could be a factor in the Fed’s decision on rates. Previous government shutdowns have been a factor in reducing US Treasury yields.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.