Online retail sales growth slowed in May following a fairly strong April

Insight

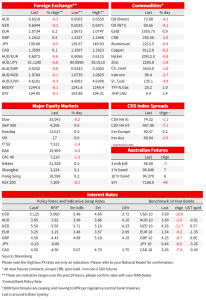

After enjoying a long weekend, the US is back with mixed signals coming from equities and bond markets. US Treasuries have led a move lower in core global bond yields while the S&P 500 is unchanged. Oil prices fall over 4% with OPEC + meeting looming large, the USD is little changed, but AUD and NZD struggle, not helped by Yuan weakness.

NZ: Dwelling consents (m/m%), Apr: -2.6 vs. 6.6 prev.

AU: Dwelling consents (m/m%), Apr: -8.1 vs. 2.0 exp.

EA: Economic confidence, May: 96.5 vs. 98.8 exp.

US: Conf. Board consumer confid., May: 102.3 vs. 98.8 exp.

After enjoying a long weekend, the US is back in business with mixed signals coming from equities and bond markets. US Treasuries have led a move lower in core global bond yields with the market seemingly trying to assess the economic implications from a debt ceiling deal (bigger fiscal drag hampering an already challenged growth outlook?) with softer US and EU data also fuelling the move. Meanwhile US equities seem less concern, the S&P 500 is unchanged while the NASDAQ is a tad higher. Oil prices fall over 4% with OPEC + meeting looming large, the USD is little changed, JPY outperforms post BoJ/MOF warning while AUD and NZD struggle, not helped by Yuan weakness.

US Treasuries have started the new holiday reduced working week very well supported with yields down between 10 and 11bps up to the ten-year part of the curve. The 2y rate is down 10bps to 4.46%, the 10y Notes is 11bps lower to 3.69% while the 30y part of the curve has lagged the move down just 6bps to 3.89%. The in-principle agreement over the weekend on the US debt ceiling has been a major factor at play with the market pricing out the risk of a US Government default, indeed there has been big moves in T Bills maturing in the first half of June (Bills close to the X date), for instance bills due June 6 yielded 5.2%, down from about 7% at one point last week.

Looking at Fed pricing expectations, the market has retained a bias for a potential Fed hike in June ( 64% vs 69% on Friday) but there has been a more notable move on rate cut expectations around the turn of the year and onwards with the Fed funds priced at 4.77% by the end of January next year, down from 4.86% on Friday. So compared to last week, the market is thinking the economic outlook will allow the Fed to be more aggressive in its rate cuts late this year and thereafter.

Overnight US data releases also played a contributing role for the move lower in UST yields. US consumer confidence fell to a six-month low with details in the report also revealing a bearish picture, the Conference Board business expectations index fell to its lowest reading since 2011 while the share of consumers who said jobs were “plentiful” fell to the lowest level in more than two years. Adding to the gloom, the share of respondents expecting more employment opportunities in the coming six months fell to the lowest since 2016. The Conference Board survey follows the University of Michigan consumer sentiment reading which also fell last week.

European core yields also fell last night with 10y Bunds down -9.2bps to 2.34% with Italian BTPS down 14bps to 4.14%. Economic confidence – a composite of consumer and business confidence – fell to 96.5 while other credit readings also revealed a softening in demand. Importantly too for the ECB policy outlook EU country inflation readings surprised to the downside, Belgium’s national CPI moderated from 5.6% yoy in April to 5.2% in May. Spanish (national basis) May CPI inflation moderated to 3.2%yoy (4.1% in April). This was 4-ticks below consensus (HICP inflation moderated from 3.9%oya, to 2.9%oya). Tonight we get France, Germany, and Italy CPI reports, all ahead of the Euro zone aggregate due for release on Thursday. The recent data flow suggests the EZ economy is slowing more rapidly with inflation also potentially declining more quickly.

Moving onto equities, the S&P 500 traded in and out of positive territory ending the day little changed and just above the 4200 mark. Consumer discretionary and IT gained ~ just under 1% while Consumer staples and Energy underperformed, down around 1%. The Energy sector was not helped by a steep decline in oil prices (down ~4%) as the market continues to asses the demand outlook vs a challenging economic backdrop alongside the uncertainty from OPEC +, the market is becoming increasingly worried that OPEC+ will not provide additional price support to oil at the upcoming meeting on June 4. Meanwhile the NASDAQ managed to edge higher again, up 0.32% overnight with Nvidia still enjoying its moment in the sun, up just under 3% overnight.

The USD is little changed in index terms, weaker vs JPY and GBP, but stronger vs commodity FX. The yen is at the top of the leader board, up 0.5% (USD/JPY at ¥139.79) following comments/warnings from Japan’s top currency official Masato Kanda that “It’s important that currency markets reflect fundamentals and move in a stable manner. Excessive moves aren’t desirable,”. Kanda’s comment came after the first meeting of Japan’s Ministry of Finance, the Bank of Japan and Financial Services Agency since March. As my BNZ colleague, Jason Wong noted, the irony of course is that the BoJ’s monetary policy doesn’t reflect fundamentals, with inflation exploding well above target but the central bank insisting the move is temporary and continues to artificially suppress rates.

AUD and NZD are amongst the underperformers over the past 24 hours with most of their decline coming during our APAC trading time yesterday . The AUD starts the new day at 0.6517 ( -0.37% over the past 24 hours) while NZD is 0.642 (-0.2%). We see the antipodean’s under performance linked to Yuan weakness, yesterday USD/CNH scooted up to/through 7.10 ( and USD/CNY from ~7.07 to above 7.09). Both CNH and CNY made new YTD highs, with as yet no sign of displeasure from PBOC (this after an unremarkable pre-open fixing vs expectations but which is the highest since 1 Dec 2022). The market is becoming increasingly concern over the strength, durability and nature of China’s economic recovery with expectations of further fiscal and monetary support not yet met by officials.

Finally, worth pointing out that sometime this morning the House Rules Committee should vote on the US debt-ceiling bill. Expectations are for the bill to pass which would set the stage for a floor vote Wednesday evening.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.