Online retail sales growth slowed in May following a fairly strong April

Insight

A positive night for risk sentiment with equities up (S&P500 +1.0%; Eurostoxx50 +0.9%), USD down (DXY -0.7%), and yields lower (US 10yr -3.8bps to 3.60% and 2yr -6.4bps to 4.34%).

A positive night for risk sentiment with equities up (S&P500 +1.0%; Eurostoxx50 +0.9%), USD down (DXY -0.7%), and yields lower (US 10yr -3.8bps to 3.60% and 2yr -6.4bps to 4.34%). Driving sentiment has been a paring back of Fed rate hike expectations amid Fed commentary pointing to skipping June, along with mixed dataflow. Pricing for a June hike now sits at just 24%, well down from the 69% it reached last Friday, and a full rate hike by July is now only 62% priced after having been more than fully priced. The WSJ’s Fed whisperer after the close on Wednesday pencilled a piece called Fed Prepares to Skip June Rate Rise but Hike Later . That was followed overnight by similar comments by the Fed’s Harker (“we should at least skip this meeting in terms of an increase”). As for data, Euro area inflation came in lower than expected (5.3% y/y/ vs. 5.5% expected), US unit labour cost figures were revised lower (Q1 2023 now 4.2% annualised from an initial 6.3%) alongside a softer wages narrative within ADP Employment offsetting headline strength (278k vs. 170k), and the US ISM Manufacturing showed positive inflation developments as well as highlighting ongoing recession concerns (New Orders 42.6 from 45.7).

Not overnight, but also worth highlighting was data out of China yesterday. The Caixin Manufacturing PMI came in at 50.9 vs. 49.5 expected, and better than the alternative Official version earlier this week which fell to 48.8. S&P Global noted that “helping to push the headline index higher was a strong and accelerated rise in production during May” with “greater intakes of new business…the rate of new order growth was the second-quickest seen over the past two years” (see S&P Global ). The data suggests there may be some glimmers of light amid the uncertainty around the recovery. Commodities lifted in the wake of the data, and over the past 24 hours iron ore futures are up 3.7%, copper +2.0% and Brent Oil +2.3% to $74.24 a barrel. The moves in commodities helped send commodity currencies to the top of the FX leader board in what was already a weak night for the USD (DXY -0.7%). The AUD was +1.7% to 0.6572, NZD +1.3% to 0.6069 and USD/CAD -1.1% to 1.3453. Also adding to overall sentiment just prior to the Chinese data was news yesterday that the US House passed the bill suspending the US debt ceiling in a 314-117 vote (expected given bi-partisan support). It now goes to the Senate.

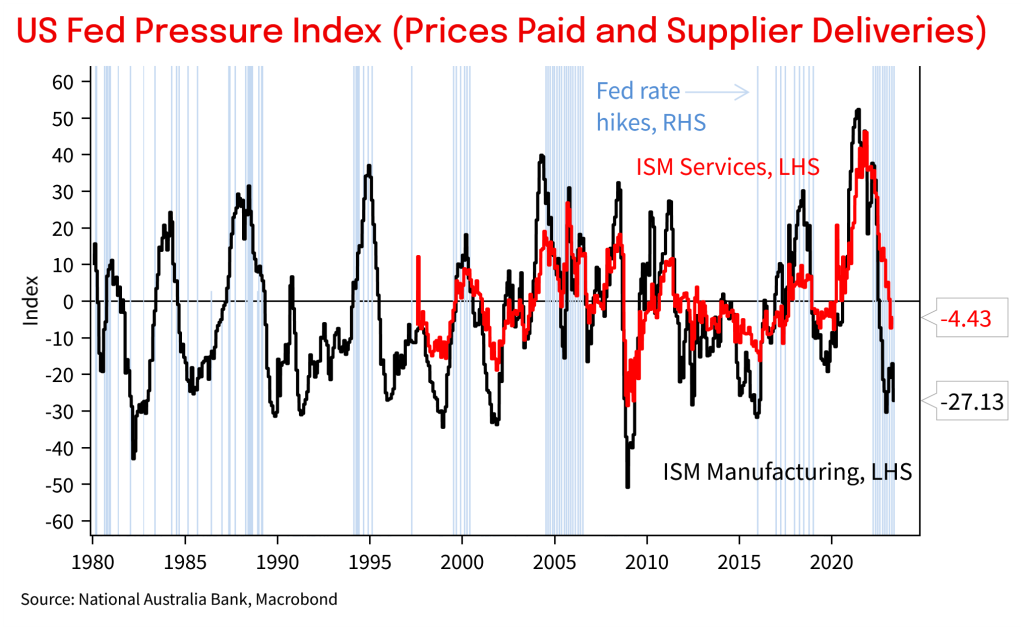

Dataflow over the past 24 hours has been generally supportive for risk sentiment. As forewarned by country-level data earlier in the week, Euro area CPI inflation came in lower than expected. Headline was 6.1% y/y vs. 6.3% expected, and Core was 5.3% y/y vs. 5.5% expected. The data suggest that inflation is heading in the right direction but ECB President Lagarde played down the figures in a speech, repeating the line that “we still have ground to cover to bring interest rates to sufficiently restrictive levels ”. Across the pond in the US the manufacturing sector remains in a recession (unlike services) with the ISM Manufacturing at 46.9 vs. 47.0 expected. Although close to the consensus, the details were less favourable with New Orders slipping to 42.6 from 45.7. On the other hand in terms of inflation it was favourable with Prices Paid falling to 44.2 from 53.2, and Supplier Deliveries 43.5 from 44.6 and lowest since 2009 (see ISM Manufacturing for details ). At NAB we combine the prices paid and supplier deliveries indexes into what we term the Fed Pressure Index, and that is pointing to the Fed no longer needing to hike rates, and if anything is in easing territory (see chart below).

On the less supportive side for risk was continued resilience in the US labour market. ADP Employment +278k vs. 170k expected, led by leisure/hospitality and points to some upside risks to tonight’s more important non-farm payrolls where expectations sit for a 195k increase (see Coming Up for details). The wages information though was more market-friendly, with the commentary noting “This is the second month we’ve seen a full percentage point decline in pay growth for job changers. Pay growth is slowing substantially, and wage-driven inflation may be less of a concern for the economy despite robust hiring ”. Pay rises for those changing jobs fell a full percentage point to 12.1% and a year ago this was running at over 16%, while job stayers saw a smaller 6.5% pay increase (see ADP Employment Report for details). In a separate report, unit labour cost inflation was revised down over 2 percentage points to an annualised 4.2% in Q1, supported by an upward revision to productivity. Meanwhile Jobless Claims were close to consensus at 232k vs. 235k expected.

Finally on US Fed talk, there were three speakers out overnight. That came in the wake of the WSJ’s Fed Whisperer’s missive of Fed Prepares to Skip June Rate Rise but Hike Later which noted “Federal Reserve officials signalled they are increasingly likely to hold interest rates steady at their June meeting before preparing to raise them again later this summer”. The Fed’s Harker was explicit about wanting to pause in June, noting “ we should at least skip this meeting in terms of an increase. We can let some of these things resolve themselves, at least to the extent they can, before we consider — at all — another increase”. The Fed’s Mester meanwhile remained hawkish and repeated her comments that featured in the FT earlier in the week, this time in the WSJ. Mester said “I would push back on this waiting until we get more information ’cause there’s never — There’s always more information…. Once I formulate a view of…that rate that I want to get to where I think that I’m balancing the risk…of over-tightening, under-tightening then hold there for a while…If my judgment tells me and my analysis tells me that we have to do more, then I would rather do that and then hold there for a while”. The Fed’s Bullard meanwhile repeated his view that rates need to go higher.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.