On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Yields tumbled and risk assets soared as US CPI came in much softer than expected

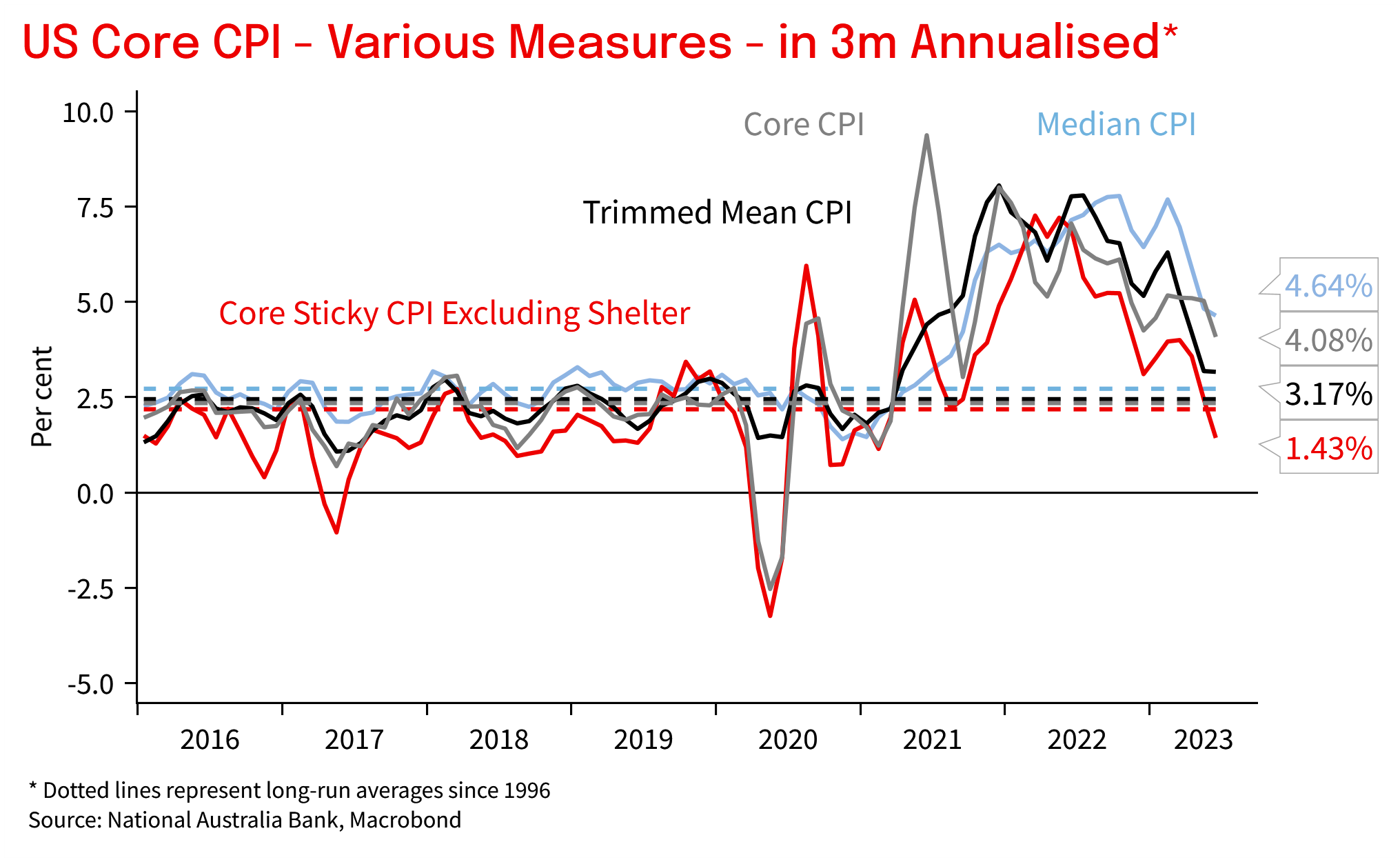

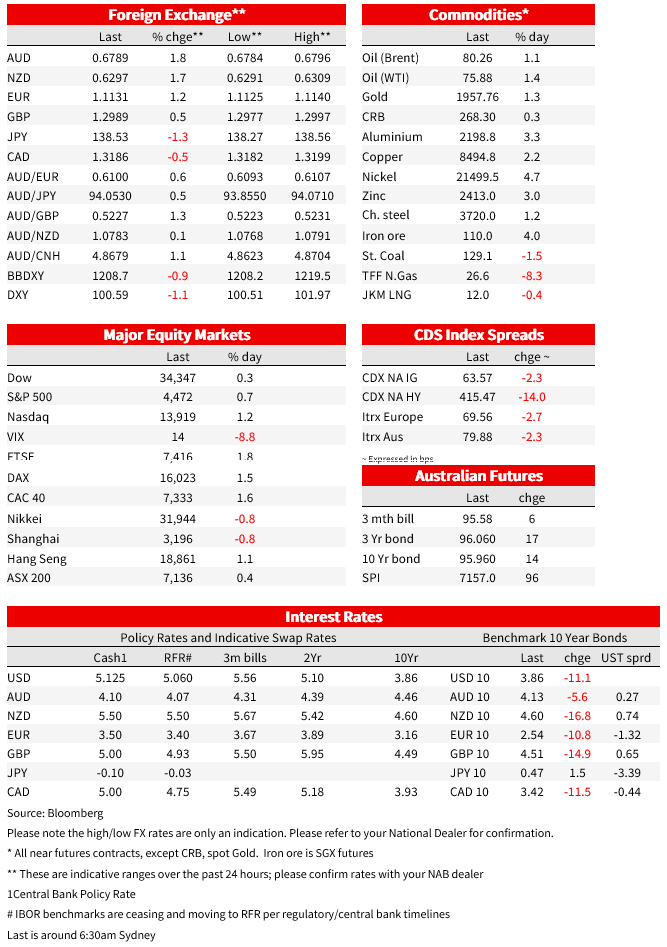

Yields tumbled and risk assets soared as US CPI came in much softer than expected. Core CPI printed at 0.2% m/m vs. 0.3% expected, and in unrounded terms was even softer at 0.158%. That takes the y/y rate to 4.8% and in 3m annualised terms is now running at 4.1%. Some alternative core measures have shown even more progress over recent months with the Cleveland Fed Trimmed Mean 3m annualised running at 3.2% and the Atlanta Fed’s Core Sticky excluding shelter is at 1.4%, though the Cleveland Weighted Median is not showing as much progress at 4.6%. US yields fell sharply in reaction with the 2yr ‑9.7bps to 4.75% (low 4.71%) with a similar fall seen in 10yrs at -8.2bps to 3.86% (low 3.84%). Interestingly the decline in yields was more than fully reflected in real yields with the 10yr TIP yield -12.4bps to 1.59%, while the implied inflation breakeven rose 3bps to 2.28%. As for Fed pricing, July rate hike pricing was little moved at 89% (same as yesterday), while cumulative hikes by November was pared to 30.9bps from 35.7bps yesterday. The biggest change is in regards to pricing of cuts with 147bps worth of rate cuts priced by end 2024, up from 133bps yesterday. Equities rose with the S&P500 +0.7%, while commodity prices were also higher alongside a weaker USD (Brent Oil +1.1% to $80.26 and Gold +1.3% to $1,957).

The USD (DXY) fell 0.9% and over the past 24 hours is -1.1%. The AUD (+1.8% to 0.6789) outperformed, along with the NZD (+1.7% to 0.6297). Lagging was the CAD (USD/CAD -0.5%) where the BoC hiked as expected by 25bps, but had also discussed the possibility of pausing, and the discussion around the outlook sounded more neutral. Governor Macklem noted “These decisions are difficult, and we did discuss the possibility of holding rates unchanged and gathering more information to confirm the need to raise the policy rate. On balance, our assessment was that the cost of delaying action was larger than the benefit of waiting ”. On the outlook, the BoC is forecasting inflation getting back to around 2% by mid-2025 (previously end 2024). If the BoC sees progress on demand growth slowing, wage pressures moderating and inflation expectations and measures of core inflation coming down further, the BoC is likely to be on hold. Markets now price a 56% chance of a follow up hike by October, down from 63% prior to today’s hike (see BoC: Monetary Policy Report Press Conference Opening Statement for details).

As for the US CPI in detail, Headline was 0.2% m/m vs. 0.3% expected, with the annualised rate falling to 3.0% y/y (and the slowest annual rate since March 2021). Core was also 0.2% m/m vs. 0.3% expected, with the annualised rate falling to 4.8% y/y. As noted above the Core unrounded was even softer at 0.158%. Driving the decline was a 8.1% plunge in airline fares, a 2.0% decline in hotel room rates, and a 0.5% fall in used vehicle prices. Alternative core measures which try and strip out volatile prices moves also came in softer with the Cleveland Fed’s Trimmed Mean at 0.2% m/m – a rate which it has average since March. Looking at the 3m annualised, there has been a greater than expected disinflation on some measures over recent months with Core annualising at 4.1%, Trimmed Mean at 3.2% and Core Sticky excluding shelter at 1.4%. With used car prices transacted in the market having fallen sharply over recent months, it is possible more subdued core rates will follow.

How will Fed officials react? It is likely officials wont want to overact to one positive data print, having been head-faked in 2021. Most officials think for inflation to keep declining, the economy will have to weaken and wages growth needs to slow. Barkin spoke post the numbers and said it is “still a question whether inflation can settle while labor market remains as strong as it is”, and that “if you back off too soon, inflation comes back strong, which then requires the Fed to do even more.” The Fed’s Mester also noted earlier this week that wages growth of 4½-5% as it is currently is well above the level consistent with the 2% inflation goal given current estimates of trend productivity growth: “ Indeed, for wage growth at the current pace to be consistent with price stability, trend productivity growth would need to be 2-1/2 to 3 percent, instead of the current estimates of 1 to 1-1/2 percent”. The WSJ’s Fed Whisperer Timiraos penned an article post the data, noting Fed officials are still likely to raise rates when they meet later this month (see WSJ: Inflation Eased to 3% in June, Slowest Pace in More Than Two Years for details). Also out was the Fed’s Beige Book, with the main takeaway being: ” overall economic activity increased slightly since late May. Five districts reported slight or modest growth, five noted no change, and two reported slight and modest declines”.

Across the Ditch, the RBNZ met yesterday and held rates steady at 5.5% after 12 consecutive hikes that began in October 2021. The accompanying statement noted “inflation is expected to continue to decline from its peak” and “there are signs of labour market pressures dissipating”, increasing the likelihood that the OCR has peaked for the cycle. The economy is evolving in line with the Bank’s expectation, and they are ‘confident’ that inflation will return to the target range, if interest rates remain at a restrictive level, for some time. Despite being in line with expectations, the NZ rates markets extended the move lower in yields.

Also yesterday, RBA Governor Lowe gave a speech on “The Reserve Bank Review and Monetary Policy”, detailing how the RBA Board will adopt the recommendations of the recent RBA Review. Adoption will begin from February 2024. The most important change in the near-term for markets is that the RBA Board will meet eight times a year, rather than 11 times as is currently the case. Four of the meetings will be on the first Tuesday of February, May, August and November. The other four meetings will be held midway between these meetings. Exact dates will be published soon. Importantly, not discussed in this speech was the RBA Review’s recommendation that the Board target the mid-point of the 2-3% target. If adopted, this would likely require even tighter policy than currently, given this is a more onerous target in the near term. Dr Lowe re-iterated that the RBA’s approach relative to other central banks has been a slower return of inflation to target, which has been framed as returning inflation to 3% by mid-2025. On the outlook for rates, Dr Lowe sounded less definitive (compared to prior speeches) and in Q&A Dr Lowe said he had “a completely open mind”, and the “issue is do we have to do more, remains to be determined” and that he was “confident that higher rates are working”. At the August meeting, the Board will have an updated set of forecasts as well as a revised assessment of the balance of risks (Q2 CPI on 26 July will be important).

In NAB’s view, the RBA August decision will again likely be finely balanced. The RBA seems to be weighing emerging signs of slower growth reasonably significantly, however as we saw in May and June, upside risks to inflation saw the RBA act and further raise interest rates. NAB’s view remains that incoming inflation data in coming months will pressure the RBA’s confidence in returning inflation to target by the mid-2025 timeframe, forcing the Board to take out a little more insurance, even as growth slows. Our preview of the Q2 and Q3 CPIs suggests trimmed mean inflation of around 1.1-1.2% q/q. This will bring the y/y rate down noticeably but doesn’t signal much ongoing progress from last quarter and the core services components, which central banks typically think of as stickier (but which may well not be this cycle), in Q2, are likely to print uncomfortably high. These elements are also likely to be pressured quite strongly in Q3 as rents, wages, insurance, rates, postal and telco services and energy prices all rise sharply.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.