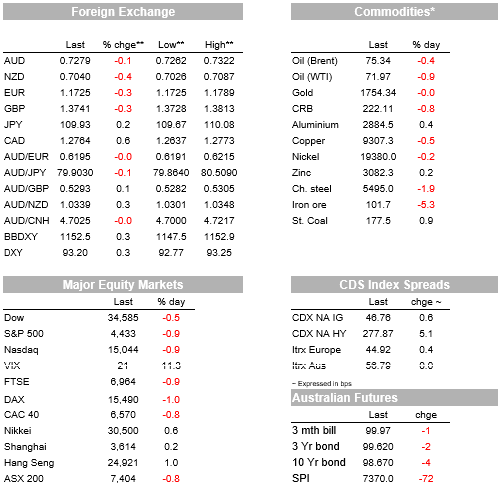

US equities fall on Friday (S&P500 -0.9%) and for September the S&P500 is down 2.0%

Yields rise, but over the week the curve flattens with 5s/30s flatter by 8bps to 103bps

FX a USD story with BBDXY +0.3%, with most FX pairs lower against the big dollar

This week: FOMC, BoE, BoJ, SNB, Riksbank, Norges Bank, Flash PMIs, Evergrande Debt

Coming up today: very quiet Monday with only NZ PSI, ECB’s Schnabel, Canada Election

“Yeah and baby, ooh sweet things that you promised me yeah; They seemed to go up in smoke; Yeah, vanish like a dream, baby;I wonder why you do these things to me; ‘Cause I’m worried”, Rolling Stones 1975

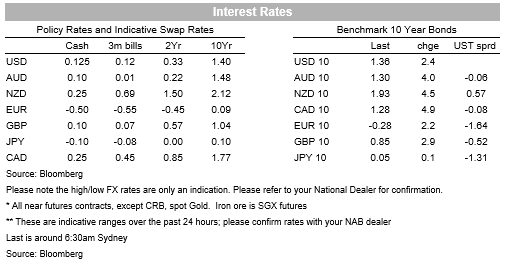

Caution is in the air ahead of the FOMC this week where market moves on Friday tiled towards a mildly hawkish outcome. US 10yr yields rose 2.4bps to 1.36% with an intraday high of 1.38%, driven by the real yield component (+4.3bps to -0.99%) while the implied inflation breakeven actually fell -1.4bps to 2.35%. Upcoming supply was also cited as factor behind the moves. Over the week the inflation breakeven has fallen -4.9bps, while the nominal yield has lifted 2.1bps. The policy sensitive 5yr yield is also up 4.5bps on the week to 0.86%, flattening the 5s30s curve further to be down some 8bps to 103bps. A flatter curve suggests some fears the Fed may overdo the eventual hiking cycle, while steepner trades have also likely been curtailed ahead of the FOMC. Key to fears of a hawkish surprise centre around the dot plot with a low bar to see a 2022 hike being pencilled in (only 2-3 people need to shift the median given 7/18 had a hike pencilled in for 2022), while the Fed will also have dots for 2024 which will give an indication of the steepness of the potential hiking cycle. As for tapering, the consensus is for an announcement to be delayed until the November or December meeting.

Equities fell with the S&P500 down -0.9% on Friday to be down 2.0% on the month so far, though still only 2.5% away from their all-time high. Newsflow has been on the softer side with China’s Evergrande woes continuing and interest payments falling due this week on Monday and Thursday (see below for details). Blue skies policy ahead of Chinese holidays (mid-Autumn this week and National Day in October), as well as ahead of the Winter Olympics in early February has added to growth fears and rising steel inventories. The delta outbreak in Fujian province is also ongoing with 45 new cases on Saturday. In this light commodity prices were generally lower on Friday. The Bloomberg Commodity index, which hit a six-year high mid-week, was down 1%. Of note, iron ore futures traded below $100/tonne on Friday for the first time since July last year. Iron ore prices are down more than 20% last week

Data flow has been modest, though the US University of Michigan Consumer Sentiment Survey highlight consumers remain cautious despite the bounce in retail sales last week. Sentiment came in at 71.0 against 72.0 expected and little moved from its fall to 70.3 last month. The lack of a bounce suggests fears around delta are more persistent. Inflation expectations were also mixed with the 1yr lifting to 4.7% from 4.6%, while the 5-10yr was unchanged at 2.9%. Interestingly buying attitudes for household durables fell again to a low reached only once before in 1980, and long term economic prospects fell to a decade low. Some commentators are drawing the link between higher inflation and reduced appetite to purchase with consumers delaying purchases until transitory inflation normalises. It could also be that delta uncertainty is also leading to higher pre-cautionary savings. Either way it suggests consumers are more cautious then the rebound in retail sales last week suggested. Meanwhile across the pond UK Retail Sales unexpectedly fell with core retail -1.2% m/m against 0.8% expected. Supply chain disruptions were cited as a factor, as well as normalising food sales.

The USD was stronger across the board on Friday, with BBDXY up around 0.3%, against a backdrop of more cautious risk appetite. Commodity and risk-sensitive currencies were among the underperformers, including the NZD (-0.4%), USD/CAD (+0.6%) and USD/NOK (+0.9%). The AUD was a little more stable, down -0.1% to 0.7279. If the Fed dot plot tilts hawkish and markets expect the lift in inflation to be transitory, then that has the potential to lift real yields and give further support to the USD.

Coming up this week:

It’s a big week for central banks with the US Fed, BoE, BoJ, SNB, Riksbank, Norgesbank all meeting. The Fed of course will garner all the attention, but also be wary of hawkish signs from the BoE’s now filled out MPC, as well as the Norgesbank which is set to lead the advanced economies in hiking. Headlines from China are though likely to remain on the weak side with Evergrande’s default closer with two interest payments due on Thursday (default risk is highly priced given one note is trading at 30% of face value). On the data front globally its PMI time again. As for Australia it is only the RBA Minutes of note. Details below:

US Fed: the key risk event for markets with the FOMC announcement on Wednesday (Thursday 4.00am Sydney time). Markets will be watching for three things: (1) will a tapering decision be made at this meeting or be left until November; (2) does the new dot plot show a 2022 hike given the low bar to shift the median given 7/18 had pencilled in a hike back in June; and (3) how steep is the hiking cycle with forecasts being extended out to 2024. NAB’s view is the FOMC will not announce a taper decision at this meeting, instead leaving open a taper announcement to the November or December meetings, timing dependent on whether the pace of jobs growth rebounds after the slowdown seen in August (we think it will). The consensus is also the Fed waits until November (65% of people) to announce a taper or even December (18%). As for the form of the taper, the initial taper is expected to be by $15bn ($10bn USTs and $5bn MBS, with tapering to fish by the end of July 2022 and thus opening up the option of a late 2022 hike. As for the dot plot, it is a very low bar for a 2022 hike, requiring just 2-3 people to shift the median dot plot. The consensus is split with 49% expecting to change, 30% expecting 2022 to show half a hike (i.e. two people shifting), while 18% expect it to show at least one hike (i.e. three people shifting). As for steepness of the cycle the consensus is 2 hikes in 2023 and 4 hikes in 2024 with the longer-run fed funds rate at 2.125% (from 2.375%). If the dot plot moves hawkish, Powell will need to be dovish.

Australia: A very quiet week with only the RBA Minutes on Tuesday and ABS Payrolls on Thursday scheduled. We are unlikely to learn much new from those Minutes given Governor Lowe’s recent speech where he expanded upon his confidence in the economy rebounding once lockdown restrictions ease in NSW, VIC and the ACT. Dr Lowe stated: “while it is hard to be precise about the pace and timing of this bounce-back, in the RBA’s central scenario, economic activity is expected to be back on its pre-Delta track by the second half of next year “. It is widely expected NSW will reach its re-opening hurdle of 70% full adult vaccination by October 8-10, and VIC by October 26 (see The Age: Victoria v New South Wales: How does the road map differ for details). Most states are within 1-1½ months of each other.

China/Evergrande: Headlines from China are likely to remain on the weak side with Evergrande’s default closer with interest payments on bank loans due Monday and interest payments on two bonds due on Thursday (whether default happens on Thursday or 30 days after the payment is due is of moot. Default and then restructuring is already well priced given one note is trading at 30% of face value and China’s Ministry of Housing and Urban Rural Development informed banks last week that Evergrande will stop paying interest on its outstanding loans starting on September 20 – i.e. Chinese officials are already helping to manage the situation. It is estimated Evergrande has around US$90bn in interest-bearing debt, while total liabilities are in excess of US$300bn (see Bloomberg: Evergrande Moment of Truth Arrives With Bond Payment Deadlines for details). The central government’s priority of social stability makes restructuring likely with haircuts for debt holders, but spillovers to other listed property developers means there will likely be a real economy impact on the real estate sector. To what extent Evergrande slows the growth momentum remains unclear. The virus situation is also problematic given the zero tolerance strategy with 43 new locally transmitted cases in Fujian province on Saturday ahead of the mid-Autumn holidays.

New Zealand: RBNZ Assistant Governor Christian Hawkesby will release a speech at 9am tomorrow on the RBNZ’s “least regrets” approach to policy and how it shaped the August MPS decision. As we all know, the RBNZ kept the OCR on hold in August due to the nationwide lockdown announcement the previous evening. However, we also know the Monetary Policy Committee discussed a 50bps increase (presumably before the lockdown announcement) alongside a 25bp hike. In explaining the thought process behind the August decision, the speech might provide the market with a sense as to whether the RBNZ might lean towards a 25bp OCR hike in October or a 50bp move. The market is finely balanced, with a 40% chance of a 50bp increase priced in for October, so there could be a meaningful market reaction if Hawkesby suggests the RBNZ is leaning one way

BoE MPC: The BoE meets on Thursday with the MPC tiling hawkish as incoming member Huw Pill casts his first vote as chief economist – he is believed to lean to the hawkish side, while four other members already see the conditions (though importantly not the need yet) for a hike. We expect the BoE to repeat it believes the rise in inflation is temporary, with an eye to rate hikes in 2022..

Coming up today:

Very quiet apart from the Canadian election. NZ has the PSI, the ECB’s Schnabel speaks on

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.