Total spending grew 0.9% in June.

It has been a quiet 24 hours in markets with generally small market movements, while the Australian dollar held onto its gains following yesterday RBA rate hike, 0.8% higher against the US dollar.

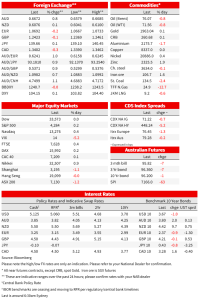

AU: Current account surplus ($b), Q1: 12.3 vs. 15.0 exp.

AU: RBA cash rate target (%): 4.1 vs. 3.85 exp.

GE: Factory orders (m/m%), Apr: -0.4 vs. 2.8 exp.

It has been a quiet 24 hours in markets with generally small market movements. US equities eked out small gains and treasury yields are slightly higher. The AUD is alone at the top of the G10 leaderboard, holding onto its post RBA move to be 0.8% higher to 66.72.

With little news flow to drive markets overnight, US equities are marginally higher. The S&P500 was 0.2% higher and the Nasdaq managed a 0.4% gain. Of note given the concentration of recent equity market gains was some rotation into financials and smaller cap stocks. Gains in the S&P500 were led by Financials and Consumer Discretionary, while the KBW Regional Bank index added 5.4% and the Russell 2000 gained 2.7%. Elsewhere, the Euro Stoxx 50 was flat, the Nikkei gained 0.9% and domestically the ASX200 lost 1.2%.

The RBA delivered a 25bp hike to 4.1% yesterday . Ahead of the meeting markets had been pricing a little below a 40% chance, while 20 of 30 analysts in the Bloomberg Survey picked a pause. AU 3yr yields rose about 10bp on the decision and 3yr futures held onto the move overnight, implied yields 8bp higher over the day to 3.66%. Market pricing almost fully prices another increase, with a peak of 4.34% by September, up 8bp from the day prior, and implies a 78% chance of another increase by August. NAB has updated our monetary policy view, and now see another hike by August and the risks skewed to a higher peak than 4.35% and will publish a full monetary policy update next week following the NAB Business Survey.

The post meeting statement kept the final paragraph unchanged, noting “some further tightening of monetary policy may be required.” But perhaps more importantly, the almost formulaic nod that “medium-term inflation expectations remain well anchored ” that had been in place since July last year has been jettisoned in favour of a longer discussion of the ills of entrenched too-high inflation. Governor Lowe speaks this morning, with the key for the path forward being the extent to which the balance of risks, or the tolerance for upside risks to inflation, have shifted.

Since the April pause, the RBA have hiked at 2 consecutive meetings. That’s despite the decision being to “allow more time to assess the impact of the increases in interest rates to date and the economic outlook ” and Governor Lowe having been explicit that the RBA was deliberately taking a different (less hawkish) path than other central banks by prioritising maintaining gains in the labour market and tolerating evident risks on inflation. Yesterday’s post meeting statement suggests that the RBA is increasingly unsure of its core thesis that inflation expectations remained well anchored and inflation was on a ‘glide path’ back to 2-3% given cumulative tightening so far and the outlook for wages growth. The more inertial parts of the wages process are increasingly reflecting tight labour market conditions and elevated inflation and services inflation overseas is proving stubborn. The Statement noted “ unit labour costs are also rising briskly, with productivity growth remaining subdued” as the RBA’s comfort ebbs with its contention that “wages growth is still consistent with the inflation target.”

The AUD was 0.8% higher on what was otherwise a quiet day for currencies, a beneficiary of the RBA’s decision to increase rates. The aussie is now back comfortably above 66 at 66.73 and more than 3% above last week’s low of 64.58. Elsewhere in currency markets, the dollar is 0.1% higher on the DXY with the EUR is down 0.2% on the day to 1.0692. The yuan is weaker after reports that last week China asked the biggest banks to cut deposit rates. There are also reports that the PBoC might be ready to cut the reserve requirement ratio, which would unleash further liquidity into the market. Such policies signal some tolerance to a weaker yuan and USD/CNH rose to a fresh year-to-date high above 7.14 overnight before settling around 7.13.

In second-tier economic news, an ECB monthly survey showed a marked fall in consumer inflation expectations, with the year-ahead rate down from 5% to 4.1% and the three-years ahead rate down from 2.9% to 2.5%. German factory orders fell 0.4% m/m in Apr following the 10.9% plunge in March, against expectations for a near-3% bounce-back and suggestive of downside risk to the consensus pick of 0.6% for today’s Industrial Production print.

Not helped by that data flow, European rates were contained, with little movement at the 10-year maturity and Germany’s 2-year rate down 5bps. Also of some note were comments from ECB’s Knot that “a short-term financial stability risk looms around the corner.” The US 10-year rate has traded a 3.65-3.73% range and currently sits up slightly for the day at 3.70%. The 2-year rate is up 6bps to 4.52%, ahead of some chunky T-bill auctions this week as the US Treasury looks to rebuild its coffers.

Also of note yesterday was Japanese labour cash earnings data which came in weak in April , up 1.0% y/y from an upwardly revised March read of 1.3% and below the consensus for 1.8%. Analysts had expected early evidence of solid increases negotiated in recent annual pay negotiations to be evident in the data so it is an early indication they could be coming in weak. The data is far from conclusive though, with Spring wage talks (Shunto) likely more fully reflected in the May data. The BoJ had earlier suggested around 40% of the wage negotiation results would be reflected in April, and more than 80% by July. The outcome adds no urgency to a patient BoJ, which meets next Friday.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.