Online retail sales growth slowed in May following a fairly strong April

Insight

The BoC shocked markets overnight, hiking by 25bps to 4.75%.

The BoC shocked markets overnight, hiking by 25bps to 4.75%. Heading into the meeting only eight out of 37 people surveyed were expecting a hike and markets were around 45% priced. Further, the BoC assessed “monetary policy was not sufficiently restrictive ”, a hint of a follow up move in July with markets now 70% priced. The surprise hike comes after the RBA earlier this week and highlights central banks aren’t done with the hiking cycle. Yields leapt with the Canadian 2yr yield +22bps to 4.60% and the 10yr yield +18bps to 3.445%. Global yields also rose with the US Treasury 2yr yield +8.2bps to 4.56% and 10yr yield +13.1bps to 3.79%. Those moves in yields were broadly reflect in Australian bond futures with the implied 3yr yield +12bps since 4pm yesterday. US Fed Funds pricing inched higher with a move by July now 81% priced from 72% yesterday. Next week’s US CPI will be pivotal for whether the Fed goes in June, or skips as widely telegraphed. Also weighing on yields were details of refiling the TGA following the debt ceiling deal with an aim to get end-of-June cash balances to about $425bn, meaning roughly $350bn would have to be added to the TGA over the coming three weeks (see US Treasury).

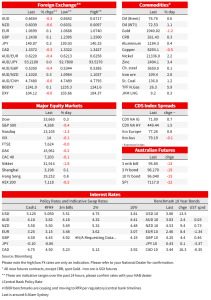

The lift in yields saw mild declines in equities with the S&P500 -0.4% and NASDAQ -1.3%. In FX an initial spurt higher in the Loonie of 0.7% was pared with USD/CAD now just -0.3%. The rise in US Treasury yields alongside the rise in Canadian yields a likely factor. The broader USD meanwhile was flat with DXY 0.0%. Underperforming was the AUD -0.3% to 0.6652, with weak Chinese trade data providing little support and keeping the AUD in the narrow range it has been in for some time (note Chinese exports were -7.5% y/y vs. -1.8% expected; and imports were -4.5% y/y vs. -8.0% expected). Over the past 24 hours USD/CNH is up +0.2% to 7.148 (briefly breaking 7.15 for the first time this year), while AUD/CNH was little changed at 4.7480. Also on the weak side was the Yen with USD/Yen +0.4% to 140.16 and reflective of the global rates backdrop. The other majors were EUR +0.1% and GBP +0.1%. The biggest move in FX has been in EM where the Turkish Lira has plunged 7.9% over the past 24 hours to a record low with USD/TRY now 23.26. Traders reported state lenders halted dollar sales to defend it.

As for details around the BoC which shocked markets overnight by hiking overnight. That hike to 4.75% came after the BoC had paused for two consecutive meetings (March and April). The post-Meeting Statement noted that “monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target”. Of key concern was that CPI inflation had ticked up more than expected despite lower energy prices (“ CPI inflation ticked up in April to 4.4%, the first increase in 10 months, with prices for a broad range of goods and services coming in higher than expected. Goods price inflation increased, despite lower energy costs. Services price inflation remained elevated, reflecting strong demand and a tight labour market”) at a time that growth was stronger than expected (see BoC: Meeting Decision for details). While the Statement didn’t provide explicit forward guidance, it is widely expected the BoC will follow up with another hike with markets 70% priced for July, and in total there is a cumulative 39bps priced by December.

Closer to home yesterday, RBA Governor Lowe gave hawkish remarks yesterday which affirmed his recent hawkish tilt. Dr Lowe noted that the back to back increases in May and in June, following the April pause, reflected a reassessment of the upside risks to the inflation outlook, which clash or threaten the objective of getting inflation back to target in that reasonable timeframe: “the Board is particularly attentive to the risk that inflation stays too high for too long”. Adding to this hawkishness was a clarification on the weighting he was puting on activity vs. bringing inflation down with the desire to preserve a low unemployment rate “ not mean[ing] that the RBA board will tolerate higher inflation persisting. There is a limit to how long inflation can stay above the band”. When asked about QT, he downplayed the chatter for now, stating QT isn’t really an effective tool when you have rates. Datawise, Q1 GDP was broadly as expected (0.2% q/q vs. 0.3% expected), but the more interesting detail was on labour costs and woeful productivity. Several banks revised up their RBA calls to around 4.60-4.85%. Markets currently price a peak RBA cash rate of around 4.39%.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.