We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Soft risk sentiment overall last night which was mostly China driven.

Soft risk sentiment overall last night which was mostly China driven. While China’s 5yr loan prime rate was cut by 10bps to 4.20% yesterday, consensus was for a larger 15bps cut. This lower than expected cut combined with no firm announcements of a sizeable stimulus package after last Friday’s State Council Meeting, despite much media hype, has many wondering how willing China is to stimulate its economy. USD/CNH is up 0.3% and currently trades at 7.1824. CNH has weighed on the AUD (-0.8%) and NZD (-0.5%), with these underperforming given the USD DXY was +0.1%, while the AUD itself was pulled lower by a less hawkish RBA Minutes. Markets now price a 51% chance of a July RBA hike and fully price two hikes by November.

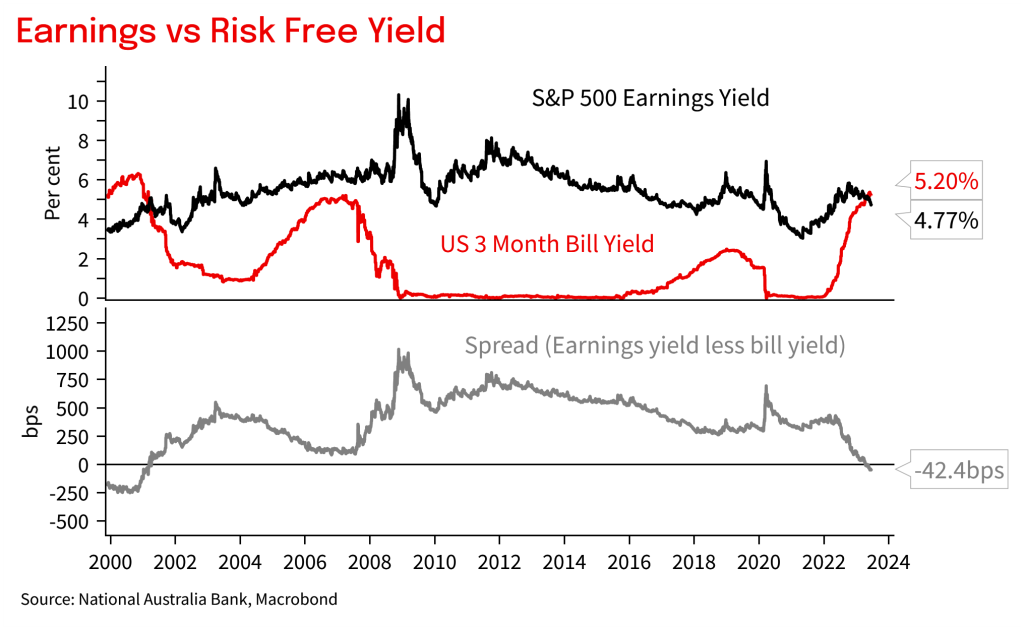

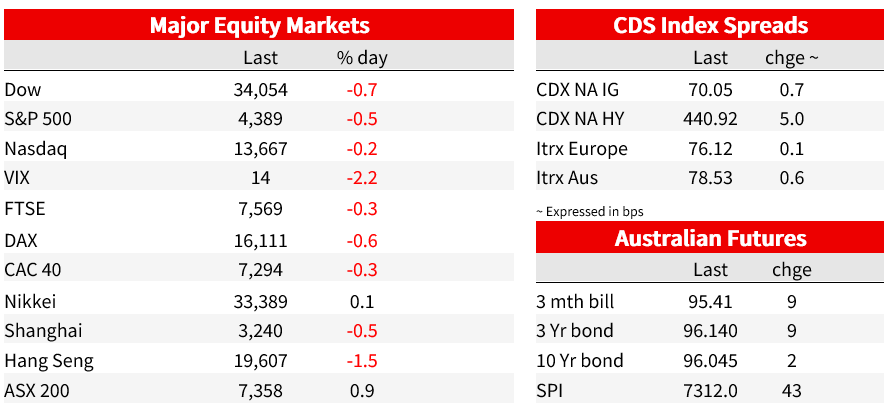

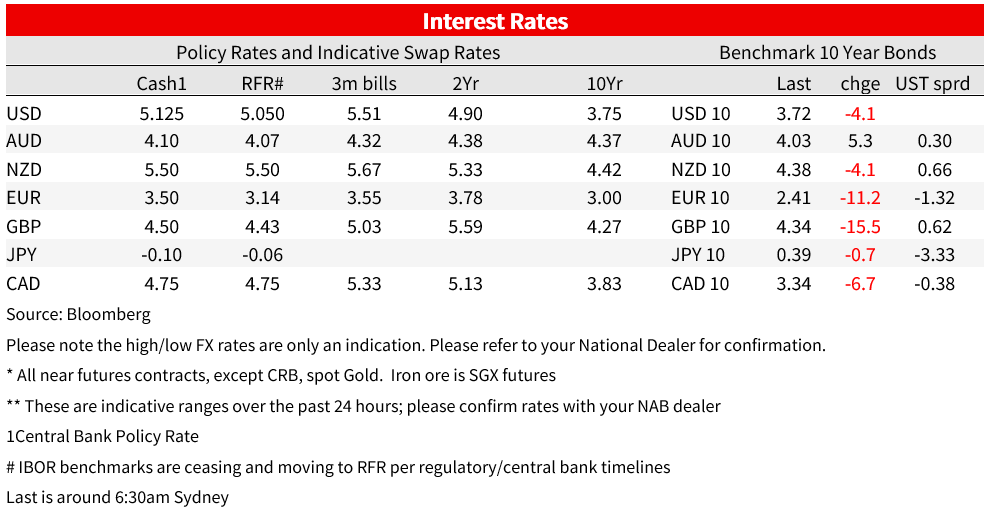

Datawise it has been quiet with only US housing data which was dangerously strong, and was heavily discounted (housing starts 21.7% vs. ‑0.1% expected; housing permits 5.2% vs. 0.6% expected). Global yields are lower with the US 10yr -4.1bps to 3.71%, with larger falls in UK (10yr -15.5bps to 4.34% ahead of CPI tonight and BoE on Thursday) and Germany (10yr -11.2bps to 2.41%). Global equities were on the softer side – S&P500 -0.5%. Early rebalancing ahead of month/quarter end a likely factor behind moves, as are bill/bond yields relative to equity yields (see chart of the day).

First the RBA Minutes yesterday which at one point saw front end bill futures up some 8.9bps. The Minutes at first glance read less hawkish for two reasons: (1) There was no mention of the “some further tightening” may be needed in the Minutes, which had been in every Minutes in some version since the tightening cycle began in May 2022. However we caution not to read too much into this as this phrase was in the post-Meeting Statement and was also mentioned in Governor Lowe’s subsequent hawkish speech, the Minutes themselves even note that the speech would flesh out the Board’s thinking; and (2) ambiguous phrasing that could imply a pause was more likely in July – this surrounded this sentence: “ in light of these considerations, members discussed the possibility of holding the cash rate unchanged at this meeting and then reconsidering at subsequent meetings, with the benefit of additional data.” NAB continues to see the RBA needing to hike rates to 4.60%, having pencilled in July and August. Next week’s Monthly CPI Indicator will be important.

As an aside, if it wasn’t for those two observations above, the Minutes would have read very hawkishly given the discussion around the risks of inflation expectations becoming de-anchored: “members discussed the possibility of implicit indexation of wages to past high inflation and the potential for this to become widespread. Similarly, members observed that some firms were indexing their prices, either implicitly or directly, to past inflation. These developments created an increased risk that high inflation would be persistent…” ). Elsewhere in the Minutes, discussion was made of Australian services price pressures including energy, wages and rents. This reinforces to us, the view that further interest rate rises are likely to be required. RBA Deputy Governor Bullock also spoke separately after the Minutes. Her speech more explicitly acknowledged that unemployment will need to rise somewhat in order to get inflation back to target: “our goal is to return the labour market (and the market for goods and services) back to a level more consistent with full employment” and that some model estimates of NAIRU are around 4½%, broadly where the RBA expects unemployment to get to by late 2024.

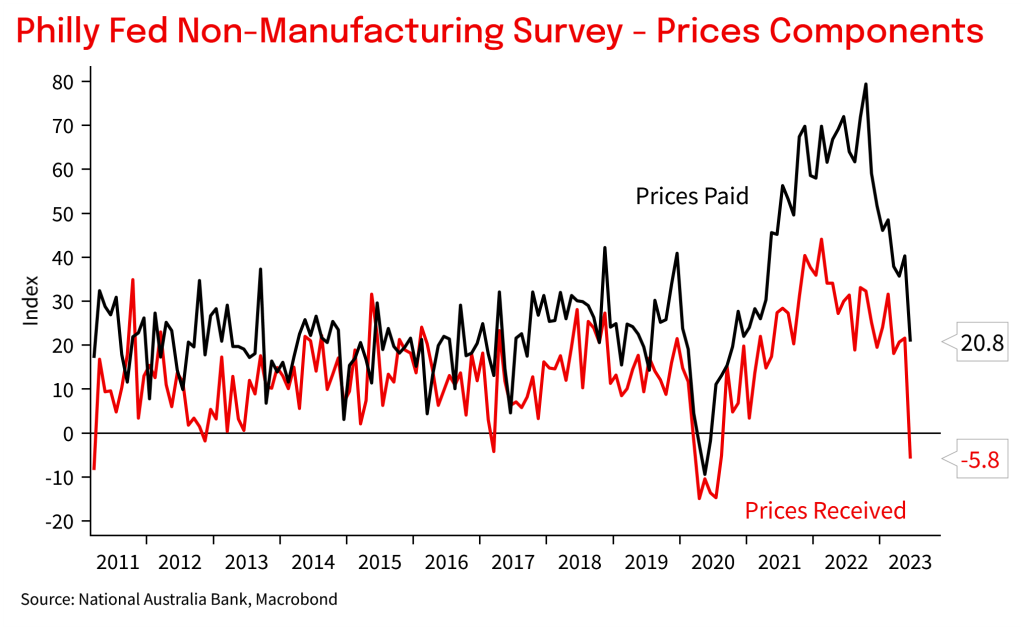

There was no top-tier data overnight. The most notable of the second-tier was US Housing Starts which unexpectedly surged 21.7% m/m in May vs. -0.1% expected, to be at their highest in over a year . Building permits also showed a much stronger than expected 5.2% m/m gain. The stellar figures were discounted given starts must be preceded by permits, and starts were just so much stronger than permits. What the data does show though is the dislocation in global housing markets, with the existing housing market having low volumes as owners are reluctant to sell – in the case of the US households have locked in lower rates for 30yr years. This should help support residential construction even in the face of high mortgage rates, and construction cost inflation has also eased dramatically in the US over the past year. Also out overnight, but not garnering as much attention was the Philly Fed Non-Manufacturing Survey. The prices questions in this survey fell to very low levels – prices paid now at its lowest since October 2020 and priced received is now at its first negative reading since August 2020 (see chart of the day below and June 2023 Nonmanufacturing Business Outlook Survey).

There has been some central bank speak. Bank of France Governor Villeroy de Galhau remained on the dovish side of the spectrum, saying “we have done most of the path” in reference to the tightening cycle and suggesting an earlier fall in inflation to the 2% target than the official forecasts show. Reports from other GC members overnight weren’t as dovish though. In the US, Fed Governor Jefferson who was selected by President Joe Biden to be elevated to vice chair, noted in his Senate nomination hearing that: “inflation has started to abate, and I remain focused on returning it to our 2% target”, but nothing really to write home about, and most focus will be on Fed Chair Powell who is giving testimony later tonight.

Markets chart of the day: Risk free yield now above S&P500 earnings yield

Eco chart of the day: Prices received falls back according to the Philly Fed Non-Manufacturing Survey

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.