Total spending grew 0.9% in June.

The BoE surprises market with 50bps, Norges Bank less so with its 50bps. SNB opts for a ‘hawkish' 25bps

Central bank decisions came thick and fast last night, the highlight being the BoE’s 50-point hike to 5.0% against the better judgment of every UK analyst polled by the newswires, albeit money markets went into the decision attaching about a one-third chance to 50. Norges Bank’s 50bps hike was less of a shock, with a very large minority of analysts expecting it, while the SNB’s 25-point hike (following prior 50-point moves) was in line with consensus (only a few had opted for +50bps) though the messaging surrounding the announcement was hawkish, President Jordan saying it’s ‘most likely’ further tightening will be necessary. US equity markets are closing with gains of 0.4% for the S&P500 and 1% for the NASDAQ, though currencies are trading with more of a risk-off than risk-on feel, the DXY USD index up a third of percent and AUD and NZD amongst the worse performing currencies (after JPY). Bond yields are higher everywhere except the UK long end, the 2/10s gilts curve inverting to its most since 1988.

The BoE, after announcing its decision which it said was ‘required at this meeting’ (singular) it made clear it retained a tightening bias, noting further tightening “would be required” if there were to be evidence of more persistent inflationary pressures. Governor Bailey said, “the economy is doing better than expected, but inflation is still too high and we’ve got to deal with it”. Money markets ended Thursday ascribing a 75% chance to the Bank following up this move with another 50-ponter on 3 August and priced the terminal Bank Rate at a shade over 6% (December OIS is now 6.05% – prior to the upside CPI surprise earlier this week it was 5.80%).

As for the Norges Bank, who raised its benchmark rates from 3.25% to 3.75% (half expected), officials said that the rate will ‘most likely be raised further in August’ and that it currently foresees a peak at 4.25% later this year and that the decision is justified, given that inflation has come in ‘markedly higher than anticipated’.

And for the SNB, whose 25-point hike was in line with consensus, the decision to dial down the scale of hikes after the 50-point moves at the prior two quarterly meetings, while saying further tightening will ‘most likely’ be necessary, came in conjunction with them actually lowering its 2023 inflation forecast, to 2.2% from 2.6%, though 2024 is now 2.2% and 2025 2.1%, up from 2.0% for both years previously.

US data overnight included weekly jobless claims, which held at last week’s 264k (roughly as expected and the third week above 260k from the 230-240k range in prior months) though continuing claims dropped to 1,759k from 1,772k, below the 1,785k expected. May Existing Home Sales continue to be hampered by the lack of supply given the strong disincentives of homeowners to move and lose access to their ultra-low rate 30-year mortgages, steady at 4.3mn after 4.29mn in April. A year ago they were running closer to 6mn per month. The Kansas Fed’s Manufacturing Activity index fell to -12 from -1, more than the -5 expected.

Outside of those central banks making policy decisions on Thursday, Fed chair Powell gave his second semi-annual testimony, this time to the Senate, and in questioning noted that while the Fed doesn’t see a lot of evidence of credit tightening, it might substitute for one rate hike. He said the Fed is trying to avoid the mistake of going too far on rate hikes but doesn’t see rate cuts happening anytime soon. Nothing really new there. He admitted the Fed’s supervision was shown to be lax with regards to SVB. Richmond Fed president Barkin has just been speaking where he notes that demand is still elevated versus its pre-covid trend and that he’s yet to be convinced what weakness there is feeding into (lower) inflation, which is too high despite falling from its peak. Barkin says he’s comfortable with more hikes if inflation is not heading to its goal.

ECB speak has come from the generally hawkish Buba chief Joachim Nagel who said the ECB’s deposit rate hasn’t reached a “high enough” level yet but that the next steps would depend on incoming data, and that “When we’ve reached the peak, interest rates will remain at this level for as long as necessary. Breaking inflation requires vigorous action as well as perseverance”

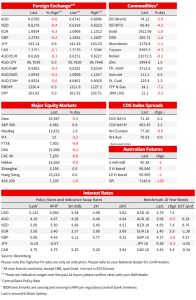

Bond market reaction to the BoE was to see further yield curve inversion, 2-year gilt yield ending the day +2.3bps and 10s -3.8bps. The 2/10s curve at -69bps compares to zero less than a month ago and it the most inverted since 1998. US Treasury yields in contrast are higher across the curve, 2s by 7.6bps and 10s 7.4bps (German bunds also 6-7bps higher out to 10 years). 10-year Aussie bond futures have implied yields 3bps up on Thursday’s local close.

In FX , following the obligatory algo-driven pop higher in GBP on the BoE announcement, the pound fell back, consistent with what we saw post Tuesday’s stronger than expected CPI data, elevated recession concerns driven by ever high policy rates doing some damage and consistent with the further inversion of the UK yield curve. That said, GBP is actually one of the better performers on the day, up slightly on most crosses. The 0.2% drop against the USD exceeded by EUR (-0.3%) NZD (-0.4%) and the AUD (-0.6%). Weaker antipodean currencies come despite the gains eked out by the US equity market – albeit European stock were all lower – and suggest that weaker (global) growth concerns have been the overriding influence on the day. USD/JPY has risen the most in G10, +0.9% to just above ¥142 in line with higher Treasury yields, so entering the terrain above which the BoJ last intervened (around ¥146.50 on 10 November last year).

Finally, deepening global growth concerns driven by ever-higher rates are evident across the commodity complex, led by fall in crude oil of $3 for WTI (Brent similarly) and all base metals (see table below).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.