Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

BoE meeting more hawkish than expected, seen opening door to hikes by year’s end.

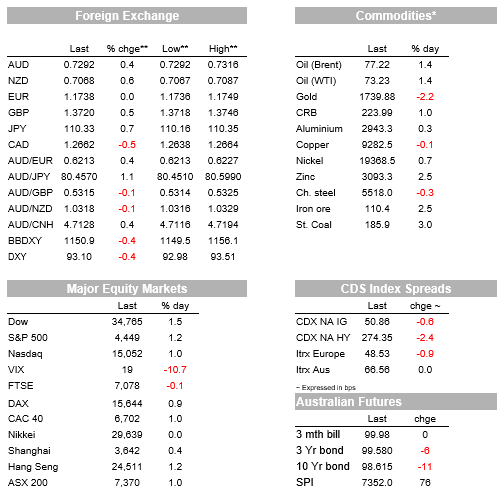

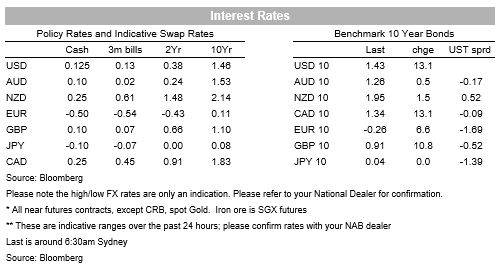

Global yields leapt overnight with the US 10yr yield up 13.1bps to 1.43%. The move in yields came in the wake of a more hawkish BoE overnight which flagged the possibility of hikes even before the end of its QE program and also concluded the case for some modest tightening had strengthened. UK markets now price 15bps of hikes by February with 50bps of hikes priced for 2022, while 10yr Gilt yields led the global bond sell-off with UK 10yr yields +10.8bps to 0.91%. Also adding to the hawkish theme was the Norgesbank which hiked as expected, but also slightly lifted their rate hike path compared to June and flagged December 2021 as the date for the next hike. The hawkish soundings from the BoE and Norgesbank reinforce the hawkish tilt in the Fed’s dot plot on Wednesday which saw the committee evenly split on a 2022 hike (at 9 vs. 9).

Risk sentiment was unperturbed by the move in yields, instead taking its lead from news around Evergrande alleviating fears of a ‘Lehman’s’ type moment. The S&P500 rose 1.2% overnight and is now in the green for the week up 0.3%. By the dip no doubt the main driver, while energy outperformed (energy sub-index +3.4%) alongside the oil price (Brent oil +1.4% to $77.22). The USD fell (BBDXY -0.4%) as did the Yen (USD/Yen +0.7%), with risk-sensitive currencies higher such as the AUD (+0.4%) and NZD (+0.6%). Two big near-term issues that have weighed on investors’ minds recently – Evergrande ‘Lehman fears’ and the US Debt Ceiling. Both issues have eased somewhat (see Evergrande and Debt Ceiling paras below). Economic data though has moved the other way, coming in below expectations mostly.

First to Evergrande. Evergrande made interest payments on a local currency bond, though it is unclear whether US$83.5m in coupon payments were made on its USD bond– there is a 30 day grace period before technical default is considered (Chinese regulators had encouraged Evergrande to take all possible measures). More importantly, Chinese authorities are readying restructuring teams, alleviating fears of a Lehman’s type moment. The WSJ notes “ local governments have been ordered to assemble groups of accountants and legal experts to examine the finances around Evergrande’s operations in their respective regions, talk to local state-owned and private property developers to prepare to take over local real-estate projects…). (see WSJ: China Makes Preparations for Evergrande’s Demise for details). Evergrande’s share price jumped 18% yesterday while its 2022 USD bond increased over $3, to a still distressed price of $32.70.

As for the move in rates, the Bank of England appeared to open the door to an interest rate hike before the end of the year, noting “any future initial tightening of monetary policy should be implemented by an increase in Bank Rate, even if that tightening became appropriate before the end of the existing UK government bond asset purchase programme [which is due to end around the end of the year]”. The BoE Minutes also note the case for a “modest tightening” in policy had “strengthened” due to the persistence in inflation (se BoE MPC Summary and Minutes for details). The market moved to price a 15bp rate increase by February and over 50bps of tightening by the end of next year. UK bond yields were up by a uniform 11bps from 2 to 10-year maturities, with the 10-year rate closing at its highest level since mid-2019, at 0.91%.

US yields took their que from the move in Gilts , with the hawkish BoE (and Norgesbank which hiked rates as expected, but also lifted the forecast policy path marginally) perhaps adding to the hawkish wake of the FOMC on Wednesday. The US 10-year rate broke above 1.40% overnight for the first time since mid-July, up 13.2bps to 1.43%. The yield curve also reversed yesterday’s flattening move in the wake of the Fed meeting, though the overall move in the 5s30s over recent weeks suggests markets still think the Fed could overdo the eventual hiking cycle. Also on the rates front Norway’s Norges Bank became the first advanced economy central bank to hike rates by 25bps in this cycle. The Norges Bank added that a further rate increase in December was “most likely ” while it lifted its policy path marginally with the cash rate getting to 1.25% by the end of next year. The overall message from central banks over the past two days has been hawkish.

FX has moved in a risk-on fashion overnight. The BBDXY USD index is down -0.4% while the Yen is also lower (USD/Yen +0.7%). Risk sensitive commodity currencies have led the charge, with the AUD +0.4% and NZD +0.6%. The currency market reaction to the more hawkish-than-expected Fed meeting is so far playing out very differently to that in June, which led to a sustained period of USD strength, though importantly this also coming on the back of alleviating Evergrande fears.

Finally US debt ceiling and funding the government angst also appears to be moderating slightly. Democratic House Leader Pelosi gave the first indications that she may decouple the government’s proposed funding from a debt ceiling increase. Pelosi noted: “We put this bill together in a very bipartisan way and when we added the debt ceiling is when” it became contentious, Mrs. Pelosi said. “We don’t think it will really be any problem to pass the [spending] legislation. ” Nevertheless the government is preparing for the contingency in the event that funding runs out on Oct. 1. (see WSJ: Pelosi Says Government Funding Won’t Lapse for details).

Economic data in contrast to the positivity overnight moved the other way with Eurozone PMIs weaker than expected (Composite 56.1 vs. 58.1 expected; 5 month low) and US Jobless Claims higher than expected (351k vs. 320k expected). The PMIs point to slower production growth due to supply chain issues, while rising input costs (in manufacturing highest since September 2000) were being passed onto consumers –selling prices were the 3rd highest over the past two decades.

It is a very quiet day domestically with no data scheduled. Offshore it is also quiet with only the German IFO and Fed Speakers of note. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Our global forecasts are unchanged and we continue to expect soft global growth of only 3.0 to 3.1% between 2024 and 2026.

Insight

Conditions ease as slow growth weighs on firms

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.