Online retail sales growth slowed in May following a fairly strong April

Insight

A rise in Services activity last month confirms the US economy still sits firmly on top of the world

A comfortable beat versus expectations for the headline ISM Services release, for now underscoring US economic supremacy versus the rest of the developed work, has seen the US yield curve bear flatten. FX market fallout has though been limited by an even bigger rise in core Eurozone yields and a resilient EUR after warnings from the ECB’s Knot that markets are under-pricing rate hike risk out of next week’s Governing Council meeting. In contrast, GBP has been hit by comments from BoE Governor Bailey that UK rates are near the peak. The Bank of Canada was unchanged as expected but with no fall-out on the CAD, the bank indicating it is still willing to tighten again on underlying inflation concerns. Outgoing RBA Governor Phil Lowe speaks at lunchtime today, and before that we should get August China trade numbers – they were a big (CNY and AUD-negative) market mover last month.

The stronger than expected ISM services repor t has captured much, but not all, of the overnight headlines and market price action, coming in at 54.5 up from 52.7 and a consensus expectation for a dip to 52.5. Within the report, New Orders rose to 57.5 from 55.0, Employment to 54.7 from 50.7 and Prices Paid to 58.9 from 56.8. Strength in consumer spending in recent months looks to be the main driver of the improvement, but whether this can be sustained in coming months is debatable, especially with student loan repayments due to commence in October (and which have been accruing since July). The numbers have nevertheless been taken at face value with the headline strength now in even starker contrast to the rest of the world (47.9 in the Eurozone, 49.5 in the UK and 51.4 taking an average of the China official and Caixin versions). Post the release, market pricing for one more rate rise in this Fed cycle has gone from 40:60 to 50:50.

Other US data overnight saw the final US S&PGlobal PMIs a touch lower than the preliminary at 50.5 from 51.0, so sharply at odds with the ISM read and as such adding to the need for caution in interpreting the ISM result. The July US trade deficit little changed at $65.0bn (from -$65.5bn in Jun), some $3bn smaller than expected, while MBA mortgage applications fell 2.9% last wek, more than countering the 2.3% prior week’s rise.

The Fed’s Beige Book , released ahead of this month’s FOMC meeting, showed growth in the US economy and jobs market slowed in July and August, while many businesses expect wage increases to ease broadly in the near term. “Contacts from most districts indicated economic growth was modest,” the report said, while nearly all districts indicated businesses “renewed their previously unfulfilled expectations that wage growth will slow broadly in the near term.” The Fed’s report indicated US consumers remain robust, especially when it comes to spending on travel and other services, but also showed signs of fraying at the edges of the economy (Bloomberg reporting).

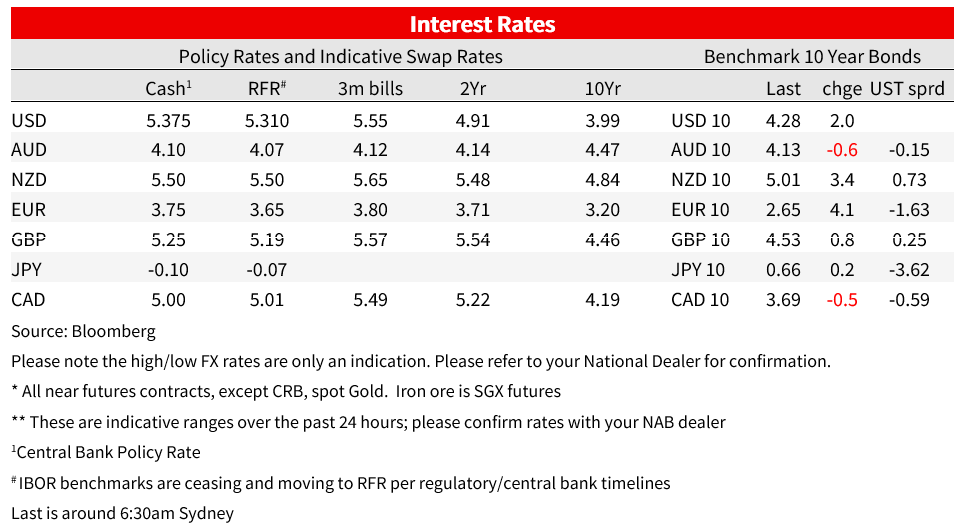

The Bank of Canada stayed on hold at 5% as expected. BoC said the economy had shifted into a weaker phase and labour market pressure have eased, but that it remains concerned about the persistence of underlying inflation and is prepared to raise rate again should conditions not improve. Markets went into the BoC pricing about a 25% chance of a hike out either this or the October meeting, and October is currently priced at about 26%. Hence no real fall-out on the CAD beyond some normal knee jerk volatility.

In Europe, the day started with a very ugly headline that German Factory Goods Orders has slumped 11.7% in July against a fall of 4.3% expected, though orders have been very volatile in recent month due to lumpy large-scale orders, the stats. office noted that the “The less volatile three-month on three-month comparison showed that new orders were 3.1% higher in the period from May to July 2023 than in the previous three months. New orders excluding large-scale orders were up 0.3% in July 2023 compared with the previous month.”

More relevant for market were comments from ECB Governing council member Klaas Knot that market may be underestimating the chances of a rate hike next week. He cautioned against too much pessimism on the Eurozone economy and that he wouldn’t be happy if inflation only reached 2% by as late as 2025. Earlier, the Banque de France chief Villeroy said the ECB’s options were open regarding the Sep 14 decision but that he is convinced rates are near a peak. ECB rate hike pricing for next week went from 25% to 33% post Knot’s comments.

Bank of England governor Andrew Bailey meanwhile, in parliamentary testimony, said UK interest rates are probably “near the top of the cycle” because a further “marked” drop in inflation is likely this year”. Bailey said much of the surge in the key rate to 5.25% from 0.1% at the end of 2021 is yet to be felt. The impact of soaring mortgage costs and the sharpest cost-of-living squeeze in generations is weighing heavily on households, darkening an already gloomy outlook. “We’ve definitely got a substantial amount of transmission to come,” Bailey said. “It appears that there is a longer transmission, that the lags are longer. We have to factor that in our policy decision.” Bailey said he didn’t know how the BoE would come down at its next (Sep 21) meeting. Market pricing for 25-point hike is now at about 90%, in from 95% before Bailey spoke.

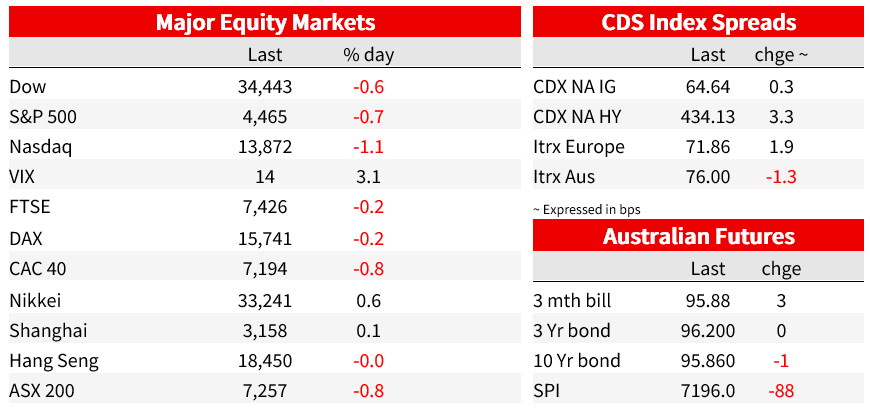

In Markets, US equities were perturbed not cheered by the economic strength implicit in the ISM report with the S&P500 off 0.7% and the more interest rate sensitive NASDAQ -1.06%, alongside which US 2-year Treasury yields have risen by 6bps and 10s by just over 3bps. IT (-1.4%) and consumer discretionary stocks (-1.0%) were the worst performing S&P sub-sectors.

Eurozone bond markets have taken an even bigger hit than US equivalents, the Knot comments at least partly responsible, French and German 2-year yields finishing the day up 8.5bps, 10s 4bps higher. UK gilts in contrast were down 3bps at 2-years and up only 1bps in 10s, post Bailey’s testimony.

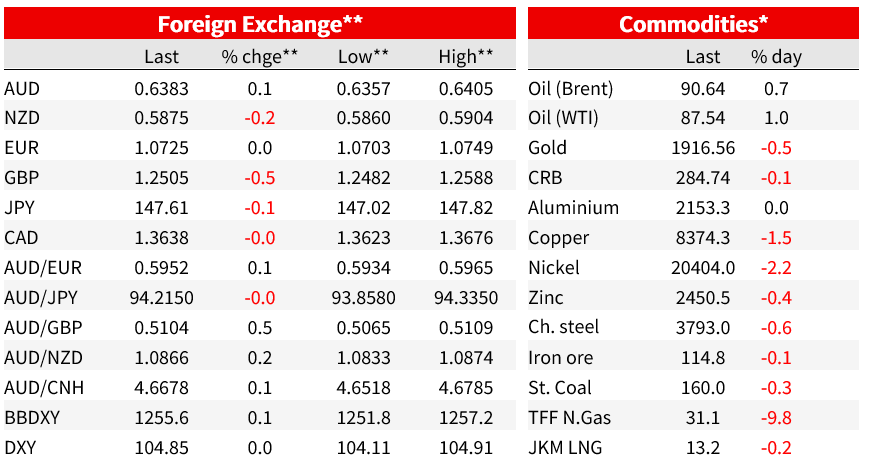

In FX, with EUR/US virtually unchanged on the day the DXY USD index is similarly little moved (just +0.03%) AUD, CAD and JPY are also little changed on the past 24-hpours, the only notable mover being GBP (-0.4%), again a response to the BoE’s Bailey’s remarks.

In commodities oil has continued to push ahead, with gains of +/- 1% for WETI and Brent crude (latter now $90.70) while gold is down 0.5%, base metals mostly lower bar aluminium, and iron ore flat.

Coming Up

Market prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.