Coming in for landing in a heavy cross wind

Insight

Yields are generally lower globally after a boost to US 2-year yields from lower jobless claims proved short-lived while equities declined.

NZ: Manufacturing volumes (q/q%, Q2: 2.9 vs. -1.8 prev.

AU: Trade balance ($b), Jul: 8.0 vs. 10.0 exp.

CH: Exports (USD, y/y%), Aug: -8.8 vs. -9.0 exp.

CH: Imports (USD, y/y%), Aug: -7.3 vs. 9.0 exp.

GE: Industrial production (m/m%), Jul: -0.8 vs. -0.4 exp.

US: Initial jobless claims (k), wk to Sep 2: 216 vs. 233 exp.

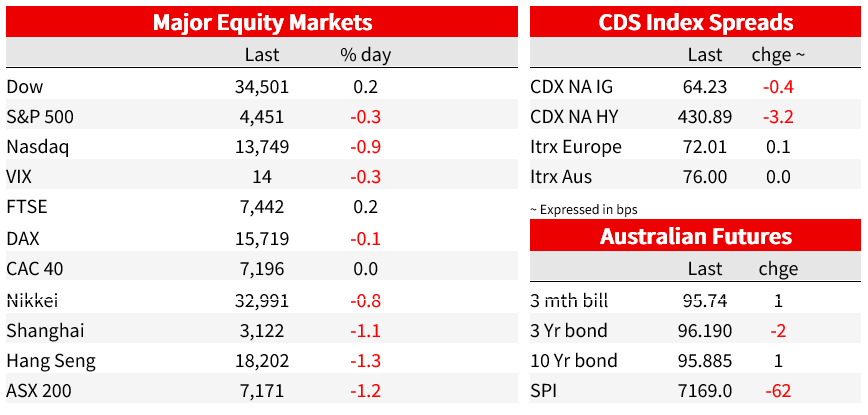

Yields are generally lower globally after a boost to US 2-year yields from lower jobless claims proved short-lived. Equities are lower, though the S&P500 pared earlier losses to be down just 0.3%. The US dollar gained 0.2% on the DXY.

US equities pared earlier losses, with the S&P500 ending the day down 0.3% after being 0.8% lower at the open. The Nasdaq underperformed, losing 0.9%, weighed again by Apple, which has now lost 6.5% in 2 days. Concern about a Chinese plan to expand a ban on the use of iPhones to government-backed agencies and state companies is weighing on big tech. Declines, however, were not broad based, with 6 of 11 sectors in the S&P500 showed gains, led by utilities, while IT led losses.

It was a comparatively light calendar for economic news, though US initial jobless claims fell 13k to 216k, their lowest level since February and below expectations for a small lift. The figures could have been distorted by holiday factors, coming a week before Labour Day, and Hurricane Idalia – where the usual reaction after a natural disaster is lower claims initially, followed by a jump. In other economic news, Germany industrial production fell for a third consecutive month in July, to its lowest level since December.

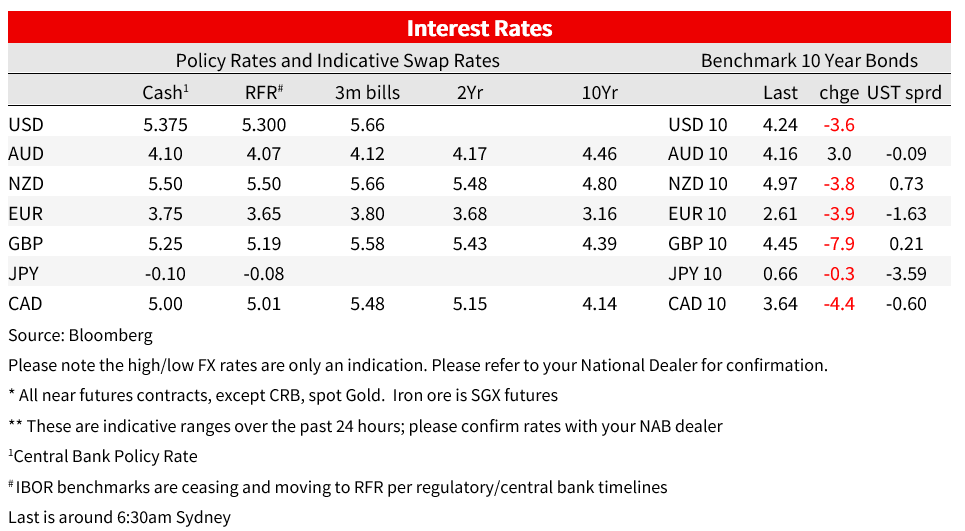

Yields are lower globally. US Treasury yields and the USD moved briefly higher after jobless claims, but the move wasn’t sustained. The 2-year rate rose 4bps to at peak of 5.03%, before a steady fall to the current 4.95%, down 7bps for the day. The curve is a little steeper, with the 10-year rate down 4bps to 4.24%. Yields were also lower elsewhere. UK rates showed falls led by the short end of the curve, with the 2-year Gilt down 10bps to 5.12%, the move supported by data showing lower business inflation expectations. The UK 10-year rate is down 8bps, while Germany’s is down 4bps. Bank of Canada Governor Macklem hinted that the tightening cycle might be over, saying “ with past interest rate increases still working their way through the economy, monetary policy may be sufficiently restrictive to restore price stability.”

Fed speakers were again broadly consistent with a data dependent Fed that is near the peak in rates. New York’s Williams said “We’ve got policy in a good place, but we’re going to need to continue to be data-dependent.” Chicago’s Goolbee made the point that the argument will soon shift from how high they need to go to “how long do we need to keep the rates at this position. ” Atlanta’s Bostic, however, said there is still a lot of momentum in the economy and ‘still work to do’ to bring inflation to target.

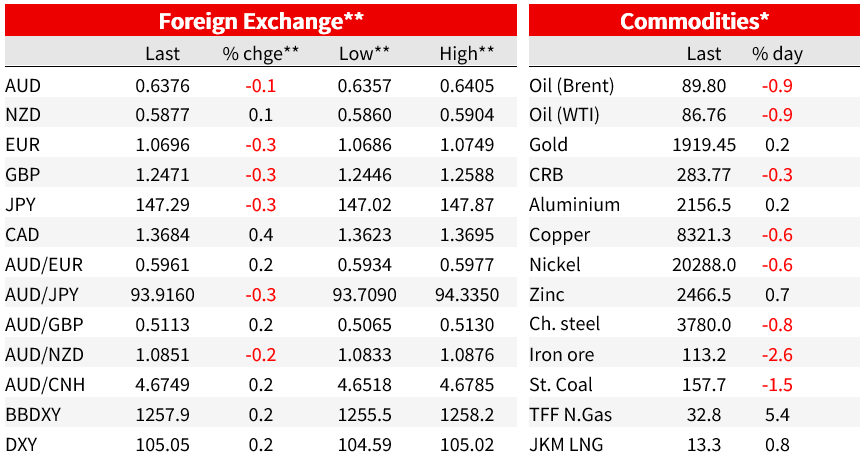

Chinese trade data yesterday showed exports down 8.8%y/y (consensus -9%y/y) in USD term, and imports down 7.3% y/y (consensus -9%y/y). Overall, the numbers were a little better than feared and showed year-ended declines smaller than in July, with price declines a factor in lower trade values. Monthly seasonally adjusted estimates implying some consolidation in exports and a pick-up in imports. Despite the trade data, USD/CNY rose through the late-2022 high, taking the onshore yuan to its weakest level in 16 years at just under 7.33. CNH lost 0.3% but at 7.34 is shy of new highs, having reached 7.3497 intraday on 18 August.

In currency markets, the AUD and NZD haven’t been dragged lower by the weaker yuan. The AUD is down -0.1% at 0.6376 while the kiwi gained 0.1%. The JPY was the best performer of the G10, but gaining just 0.3%. The backdrop of lower global yields was a support for the yen, with USD/JPY pushing down towards 147. The EUR, GBP and CAD all show small falls of 0.3-0.4% against the USD, with the DXY 0.2% higher. The euro fell below 1.07 for the first time since June.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.