Todays podcast Tesla leads gains within in US equities Core global yields tick higher USD broadly weaker with JPY and CNY the notable movers JPY gains following Ueda’s interview suggesting openness to policy move this year CNY gains on PBoC strong fix, push against speculators and better data AUD and NZD benefit from spill over […]

USD broadly weaker with JPY and CNY the notable movers

JPY gains following Ueda’s interview suggesting openness to policy move this year

CNY gains on PBoC strong fix, push against speculators and better data

AUD and NZD benefit from spill over effects

EC downgrades the euro areas economic outlook with Germany the drag

BoE Mann favours further hikes. Prudent to err on the side of tightening too much

Coming Up: NAB Business Survey, UK labour stats, ZEW, NFIB

Events Round-Up

CH: New yuan loans (CNYb), Aug: 1360 vs. 1250 exp.

CH: Aggregate financing (CNYb), Aug: 3120 vs. 2690 exp.

Breathe, breathe in the air, Don’t be afraid to care- Pink Floyd

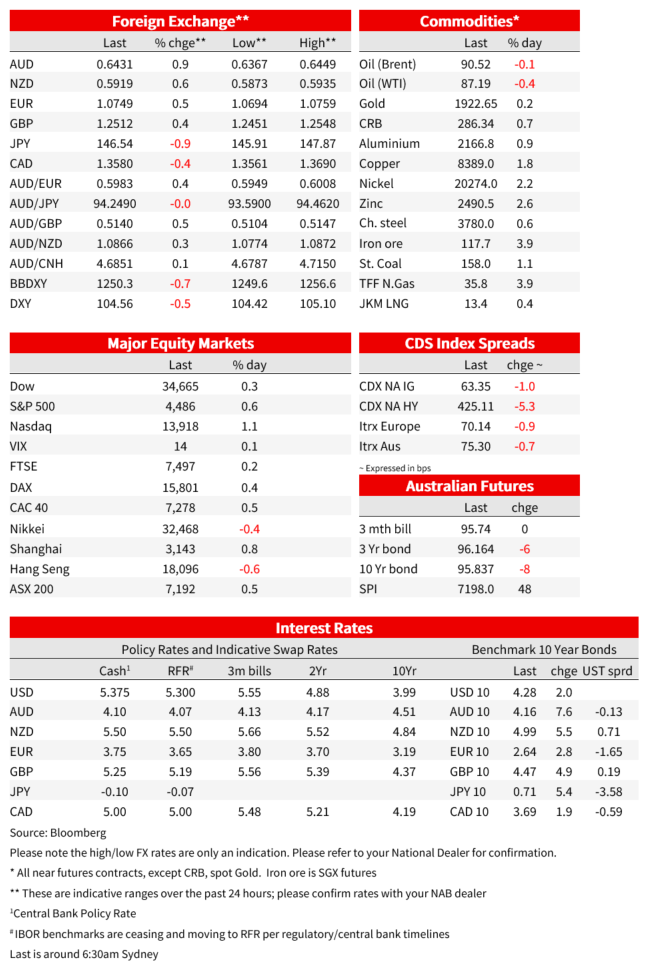

US equities have started the new week on a positive note with big tech leading the gains. Core global yields have edged a little bit higher with the UST curve showing a steepening bias.Meanwhile the USD looks to be taking a breather after 8 consecutive weeks of gains. The Greenback is broadly weaker with JPY and CNY retaining most of yesterday’s gains after Governor Ueda’s weekend interview and PBoC moves to arrest CNY weakness.

Big tech has led the gains in US equities with the S&P 500 closing Monday 0.67% stronger while the NASDAQ was +1.14%. Tesla was one of the big movers gaining ~10% following an upgrade by Morgan Stanley noting the company could get a valuation boost of as much as $500bn from its Dojo supercomputer. Qualcomm shares also gained after Apple extended a deal with the chipmaker. Earlier in the session, European equities also closed in the green with the Eurostoxx 600 up 0.34%.

FX markets are usually sedated at the start of a new week, but yesterday for a change, we had some significant moves in JPY and CNY with the USD broadly weaker as a result ( DXY -0.5% and BBDXY -0.65%). Indeed, JPY is the big G10 outperformer over the past 24 hours, 0.88% against the USD and retaining most of its gains recorded during our day trading session yesterday. JPY appreciation was triggered by a weekend Yomiuri newspaper interview with BoJ Governor Ueda. The Governor said that it’s possible the central bank will have enough information and data by the year-end to judge if wages will continue to rise, a condition for adjusting stimulus. Ueda did caveat this observation noting the central bank is still some distance away from achieving its price stability target and would continue its patient monetary easing. But if the BOJ becomes confident prices and wages will keep going up sustainably, ending its negative interest rate is among the options available. After trading down to an overnight low of 145.9, USDJPY starts the new day at 146.55, over one big figure lower relative to its Monday’s opening level.

China’s Yuan was the other big mover on Monday, boosted by a combination of PBoC initiatives and also supported by better-than-expected China credit data . Yesterday morning, the PBoC stepped up its defence of the yuan by publishing the strongest ever CNY reference rate relative to market estimates. A few hours later the PBoC said in a statement that it will take action to correct one-sided moves in the market whenever it’s needed and they are confident in keeping the yuan basically stable. Bloomberg also reported that state-owned banks were also seen actively selling dollars.

The yuan received an extra tailwind from better-than-expected credit and loan data for August. China’s banks extended ¥,360bn in new local currency loans in August on a net basis, higher than most people had expected. Aggregate financing, the PBOC’s measure of broad credit, was also above consensus expectations, rising by ¥,120bn. Looking at the year-on-year stats bank loan growth held steady at 11.1% y/y, but of note it ended a three-month string of declines. Mortgage demand remained anaemic but given the recent ease in mortgage rules (lower rates and deposit requirements) there are good reasons to expect an uptick in demand over coming months. Another bright spot was the acceleration in corporate bond issuance, however shadow credit fell back, likely due to the recent turmoil in the trust sector. All told, broad credit growth edged up from 8.9% y/y to 9.0%, the first acceleration since March.

The improvement in risk appetite, evident by the gains in equity markets along side the appreciation in JPY and CNY, triggered positive spill over effects for the AUD and NZD. The AUD, in particular, is the second best performing G10 pair over the past 24 hours, up 0.87% to 0.6432, after trading to an overnight high of 0.6449 while the NZD is up 0.6% from last week’s close to 0.5920.

The euro also managed to edge higher against the USD, +0.46% to 1.0749, notwithstanding news of an economic downgrade by the European Commission (EC). Ahead of the ECB meeting later this week, the EC downgraded its growth projection for the euro area economy by three-tenths for 2023 and 2024 to 0.8% and 1.4% respectively, dragged down by a contraction in Germany’s economy, with GDP falling 0.4% this year and only growing 1.1% next year. While the inflation projection for this year was downgraded slightly to 5.6%, it was upgraded slightly to 2.9% next year. Economists are evenly split on whether the ECB will hike by 25bps on Thursday night while the market is about 40% priced for a hike.

GBP also managed to tick a little bit higher, up 0,35% to 1.2512 with the moves supported by hawkish comments from BoE Mann . Speaking in Canada, Catherine Mann said she supported further rate hikes given that not only inflation in the UK is more embedded, but that inflation generally will be more volatile in the future. Any policy decision carries risks, but in the current scenario Mann figures that it would be prudent to risk an error that would be more easily rectified and right now that means erring on the side of further tightening.

Moving onto the rates markets, core global yields are a couple of bps higher across the board with the UST curve showing a steepening bias . The 10y UST Note ended the session at 4.287%, up ~2bp while the 30y Bond climbed 3.7bps to 4.376%. The 3-year note auction tailed by 1bp to begin cycle that includes 10- and 30-year reopenings Tuesday and Wednesday. Bloomberg also noted corporate issuance expected to be concentrated before Wednesday’s US CPI release put upward pressure on long-dated yields.

Coming Up

This morning Australia gets the NAB Business survey for August and the monthly Consumer Confidence reading for September. In July, the NAB survey revealed that business conditions stayed resilient while inflation-related measures rose, challenging expectations that the economy would continue to cool over coming months. We will be looking if these trends remained evident in August.

Later today the UK releases labour market data for July with the ILO Unemployment Rate 3Mths seen ticking up one tenth to 4.3% alongside a -185k employment change. Meanwhile complicating the BoE decision to hike or not to hike next week, the Average Weekly Earnings 3M/YoY is seen unchanged at 8.2%.

Germany publishes its ZEW Survey for September (Expectations seen at -15 vs -12.3 prev.), and the US releases the August NFIB small business optimism survey 91.5 exp. vs 91.9 prev.).

Creating cost-effective choices for consumers while forging business success is nothing new for Chemist Warehouse co-founder Jack Gance. As special guest at a recent NAB Transaction Banking event series, he looks at a new way to pay for businesses and customers.