Online retail sales growth slowed in May following a fairly strong April

Insight

European and US equities rebounded overnight with a stronger than expected US Services ISM supporting the view that it’s all good, notwithstanding the ongoing rise in energy prices and supply bottlenecks.

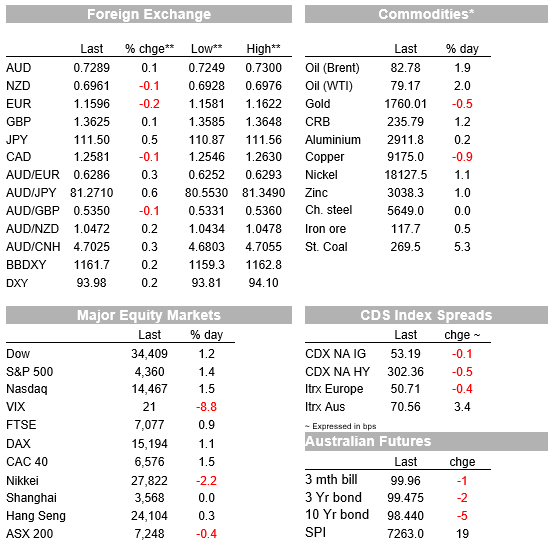

European and US equities rebounded overnight with a stronger than expected US Services ISM supporting the view that it’s all good, notwithstanding the ongoing rise in energy prices and supply bottlenecks. Oil prices have continued their ascendency with Dutch and UK natural gas up around 20% on the day with a surge in inflation expectations lifting core yields overnight. The USD is a tad stronger, gaining ground against the euro and safe-haven pairs while commodity linked currencies outperform with the AUD almost trading with a 73c handle.

Tech and financial stocks have led a rebound in equities overnight with the S&P 500 and NASDAQ up around 1% to 1.25%. Yesterday the NASDAQ lost over 2% not helped by news of an outage that left over 2.9 bn users unable to access Facebook, Instagram, WhatsApp and other tools. Overnight Facebook blamed an engineering error allaying fears of any malicious activity. A look at the S&P 500 sector performance shows IT and Financials leading the gains with the latter helped along by a steepening of the UST curve. Early in the session, Europe’s Stoxx 600 Index closed up 1.2%, with tech and financial sectors also leading the charge in the old continent.

The US Services ISM was the big data event overnight and the survey surprised to the upside, trivially rising to 61.9 vs 61.7 previously and against expectations for a decline to 59.9. The survey revealed business activity and new orders continued to rise at a solid pace in September, pointing to the US economy’s solid resilience notwithstanding the Delta covid wave and supporting the view the Fed will likely announce a QE tapering plan at its next meeting early in November. Details and commentary in the survey also warned that ongoing challenges with labour resources, logistics and materials were affecting the continuity of supply. The order backlog, supplier delivery times, and prices paid were steady in September, but remain at very high levels, meanwhile the employment index slipped less than a point to 53.0.

Also out last night, the US trade deficit widened to a record high of $73.3b in August, driven by a surge in imported consumer goods against a tepid lift in exports

The solid ISM print contributed to lift in sentiment and provided further fuel to the rise in energy prices. Oil prices have continued their ascendency with Brent and WTI up close to 2% with the latter now getting very close to the $80 mark (now at $79.24). Meanwhile there has been no let up to the surge in natural gas in Europe with both Dutch and UK futures up around 20% for the day, reflecting widespread shortages and low stockpiles.

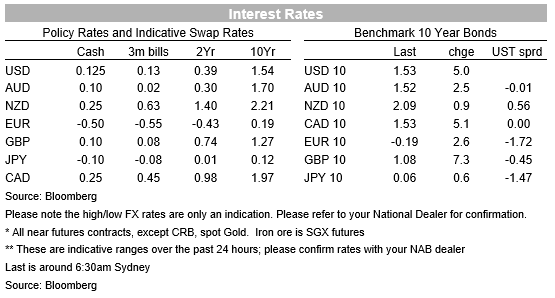

Against this backdrop, core yields lifted overnight with a rise in inflation expectations the main driver. UK breakeven added another 10bps overnight, almost hitting 4.0%, and Germany’s gained 8bps to 1.8%. The US 10-year Treasury rate is up 5bps to 1.53%, driven by a 5bps increase in the break-even inflation rate to 2.44%, taking this back to the top of its 3-month trading range, albeit still below the 2.60% peak in May.

Moving on to the FX market, the USD is up around 0.10% in index terms, primarily reflecting outperformance against safe haven currencies with JPY, CHF down 0.44% and 0.3% respectively. The euro has also underperformed, down 0.14% to 1.1595 and notably real Germany 10-year yields have fallen to a record low of minus 2.1%, with the narrowing in the real Germany-US yield spreads going a long way towards explaining the weaker euro of late. Meanwhile, somewhat surprising given similar energy struggles to Europe and in addition to labour shortages issues, GBP is up 0.21% to 1.3623.

Commodity linked currencies on the other hand, have outperformed the USD overnight with NOK and AUD at the top of the leader board, up 0.5% and 0.25% respectively. The AUD traded to an overnight high of 0.7299 and now trades at 0.7290. Ahead of the RBNZ today the NZD trades at 0.6959, little changed over the past 24 hours.

Yesterday as expected, the RBA’s policy update was a non-event, with no fresh insight from the statement, the Bank remaining optimistic about the post-lockdown recovery but unmoved on its dovish rates outlook through to 2024. With the next taper decision marked for February, the meetings over the rest of the year will also barely be noteworthy.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.