Online retail sales growth slowed in May following a fairly strong April

Insight

It was a subdued market reaction to the highly anticipated US CPI print.

US: CPI ex food and energy (m/m%) Aug: 0.3 vs. 0.2 exp.

US: CPI (m/m%) Aug: 0.6 vs. 0.6 exp.

US: CPI (y/y%) Aug: 3.7 vs. 3.6 exp.

US: CPI ex food and energy (y/y%) Aug: 4.3 vs. 4.3 exp.

UK: GDP (m/m%) Jul: -0.5 vs. -0.2 exp.

EC: Industrial production (m/m%) Jul: -1.1 vs. -0.8 exp.

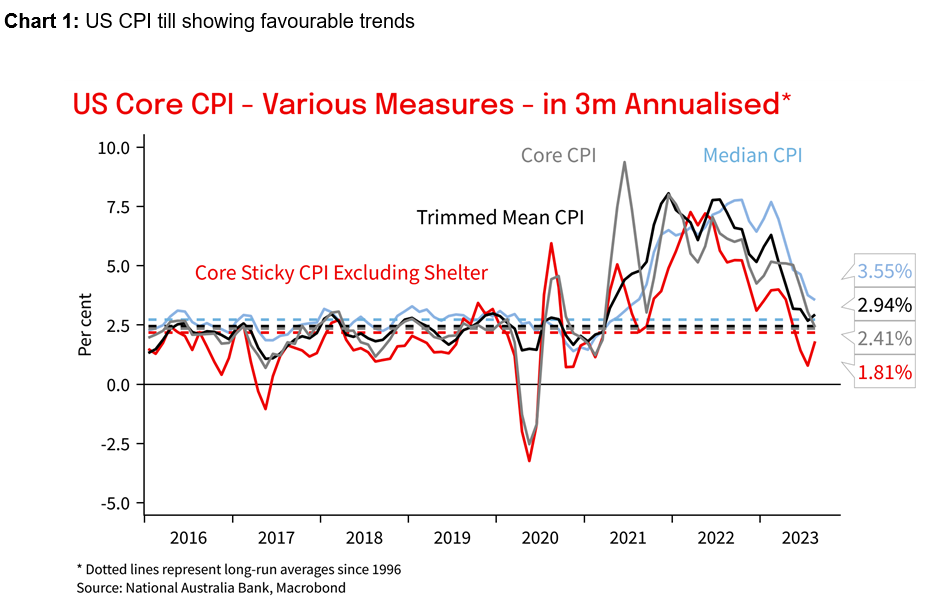

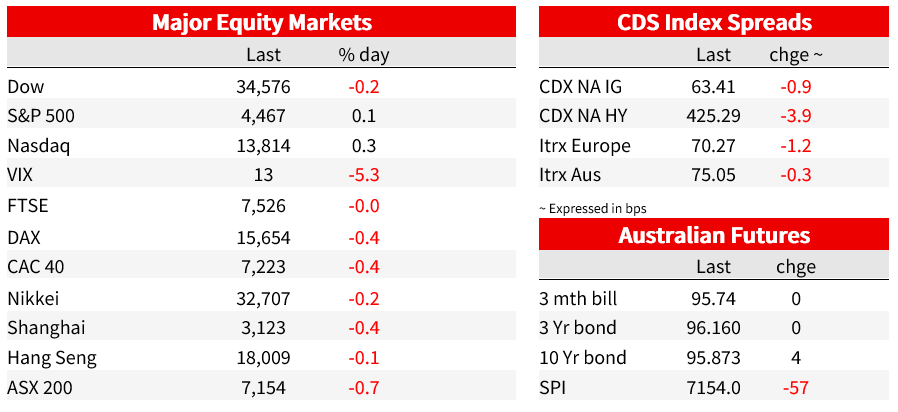

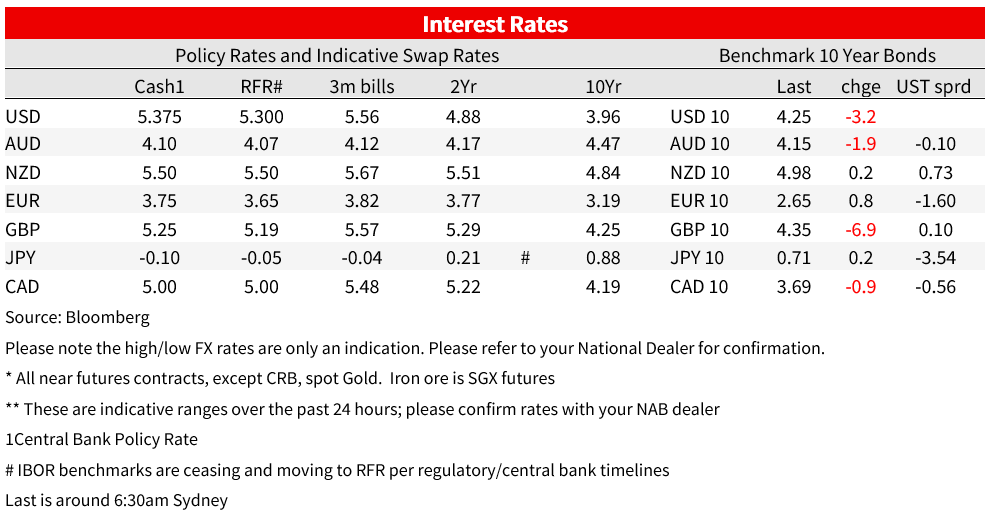

It was a subdued market reaction to the highly anticipated US CPI print. Core CPI printed at 0.278% m/m vs. 0.2% expected, though the whisper number was likely higher. The initial market reaction was of higher yields, but the moves were more than retracted soon after. US 2yr yields rose to as high as 5.08% from 5.04% prior to the figures, before then reversing to end the day at 4.98%. Ditto US 10yr yields which spiked to 4.34% from 4.31% prior to the figures, but then retraced to end 4.25%. The rally lost momentum, coinciding with a 30-year note auction where demand stats were lacklustre The USD was similar, lifting initially in line with higher yields and then falling back to be broadly unchanged (DXY 0.0%). Equities showed the same moves with the S&P500 closing up 0.1%. Overall Fed funds pricing was little moved with only a 2.4% chance of a rate hike next week, and a 40% chance of a hike by November

Why the quick turnaround in market reaction? Buy the dip might have been one factor, but more likely the marginally higher core CPI print does not change thinking around the Fed. The WSJ’s Fed Whisperer Timiraos in a co-written piece noted “The monthly core reading likely keeps Federal Reserve officials on course to hold interest rates steady at their meeting next week without resolving a bigger debate over whether they will need to raise them again this year to slow the economy and maintain recent progress on inflation” (see WSJ: U.S. Inflation Accelerated in August as Gasoline Prices Jumped ). Looking at the details of the report the miss on Core CPI relative to consensus (0.278% m/m vs. 0.2% expected) looks like it was due to airfares (+4.9% m/m) and car insurance (+2.4% m/m). As for Headline CPI it was as expected at 0.6% m/m.

In 3m annualised terms the trend on Core CPI is looking better at 2.4% and when mapping to the Fed’s preferred PCE measure it is likely running at 1.9%. Nothing then to dissuade the Fed that they are likely close to the end of the hiking cycle, but will still likely be wary about prematurely declaring inflation has slowed sufficiently given the headfakes in 2021 and 2022 which saw inflation reaccelerate after a couple of soft prints. Within the above Timiraos piece, there is also a reference to NY Fed President Williams who spoke last week, pointing to measures of inflation that incorporate a widely anticipated slowdown in rent growth, which suggests underlying price pressures are near 2.5%. “ I’m not saying that the job is done or we’re at 2.5%, but it is showing us there’s some favorable, if you will, tailwinds bringing inflation” down.

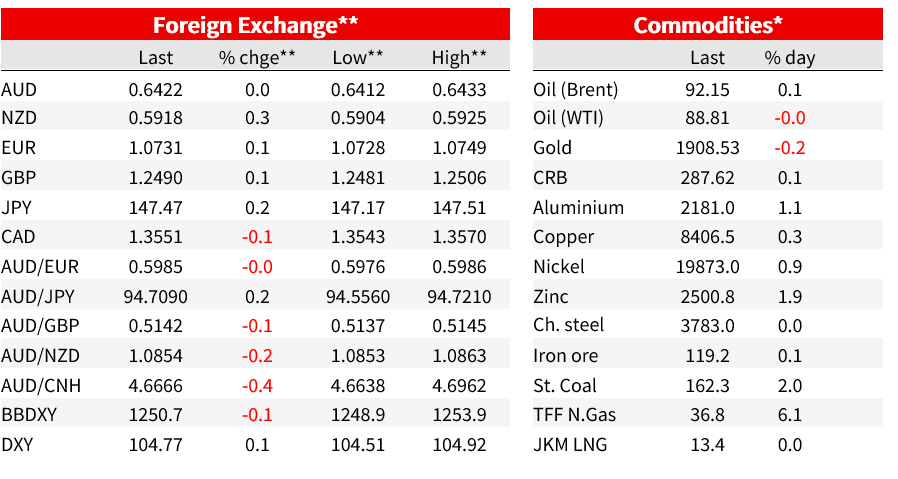

Other data flow overnight included UK Monthly GDP which was much softer than expected at -0.5% m/m vs. -0.2% expected. Output was depressed (both directly and indirectly) by strikes and by unusually wet weather in July, with some rebound likely next month. GBP/USD fell to fresh 3-month lows following the weaker than expect growth data before retracing the losses with GBP now +0.1% to 1.2490. Gilt yields were lower with 10yr -6.9bps to 4.35%. Markets still price around a 72% chance of the BoE lifting rates in September, marginally lower then the 78% price prior to the data. Also in Europe was Industrial Production, also weaker than expected at -1.1% m/m vs. 0.9% expected.

As for other FX moves the US Dollar was little changed despite the upside inflation surprise. EUR/USD was stable near 1.0750, while a brief spike in USD/JPY to 147.70 was short lived. The AUD was also little moved at 0.0% to 0.6422.The Yuan made gains in Asian trade yesterday which extended overnight. China will increase bill sales in Hong Kong to soak up yuan liquidity making it more expensive to short the currency. Implied 3-month CNH interest rates have moved sharply higher and are now above 4%. This is the latest in a series of measures undertaken by the PBOC aimed at stabilising the Yuan and to discourage speculative short positions.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.