Total spending grew 0.9% in June.

Words from politicians of various stripes have gone a little way to alleviating two of the major concerns currently plaguing global markets, namely the ongoing energy crisis centred on Europe and the looming deadline for lifting or scrapping the US debt ceiling

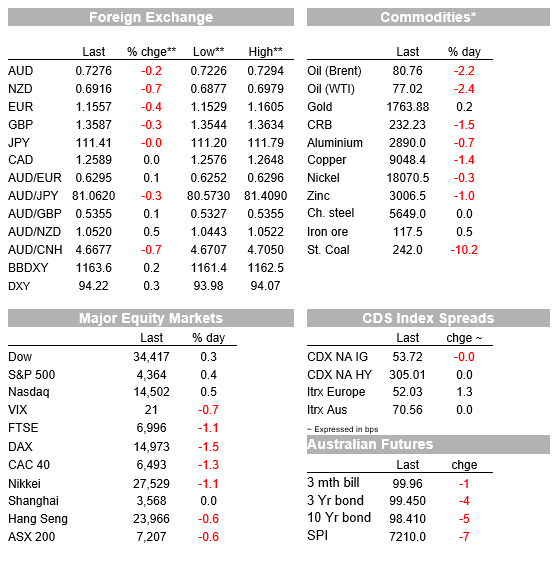

Words from politicians of various stripes have gone a little way to alleviating two of the major concerns currently plaguing global markets, namely the ongoing energy crisis centred on Europe and the looming deadline for lifting or scrapping the US debt ceiling. This had helped pull US equity indices back into the green and brought the US dollar off its intra-day highs, in turn seeing AUD about half a percent up from its lows to around 0.7270. In addition, US ADP payrolls report has gone some way to allaying fears (or maybe hopes in some quarters) for a very soft US payrolls report tomorrow night that might then delay the onset of Fed QE tapering.

The price and availability of gas has been front and centre of global markets so far this week. In Europe, benchmark Dutch gas futures rose as much as 40% in morning trading to touch EUR162.13 a megawatt-hour. Gas futures then skidded by around 10% after Russian President Vladimir Putin said Moscow was ready to work on stabilizing the global energy market. Putin said Wednesday that Moscow was a reliable supplier that always fulfills all its obligations. “We can reach another record of deliveries of our energy resources to Europe, including gas” this year, he said. Even with the fall back though, European gas prices remain more than twice as high as they were a month ago and have risen more than fivefold this year. This crisis is far from over.

And in the last hour or so, US energy secretary Jennifer Granholm speaking at FT Energy Transition Strategies Summit, raised the prospect of releasing crude oil from the government’s strategic petroleum reserve, declaring that “all tools are on the table” as the Biden administration confronts a politically perilous surge in the price of gasoline. “It’s a tool that’s under consideration,” Granholm said of a release of crude supplies from the national strategic petroleum reserve, which analysts say could calm oil markets and bring prices down. Granholm also did not rule out a ban on crude oil exports. “That’s a tool that we have not used, but it is a tool as well.”

In combination, these comments have pulled crude oil prices lower, WTI futures currently off 2.6% to $76.89. they have also helped the S&P futures rcoup an early day loss of some 1.3% to trade just in the green, finishing the NYSE day just now +0.4% with the NASDAQ +0.5%). Within the S&P, Energy has been the main drag (-1.1%) and Utilities the biggest gainer (+1.5%).

Also helpful to the risk rebound cause, U.S. Senate Republican minority leader Mitch McConnell has been out saying his party would allow an extension of the federal debt ceiling into December. “We will … allow Democrats to use normal procedures to pass an emergency debt limit extension at a fixed dollar amount to cover current spending levels into December,” McConnell said. It’s not clear whether Democrats will accept this, their proposal being to scrap the debt limit until next December 2022 (so to beyond next year’s mid-term elections).

Democrats may yet decide to go it alone via the reconciliation process, if they can cobble together an agreement on the size of President Biden’s proposed social safety net and climate change bill, currently priced at $3.5bn but which President Biden yesterday admitted may need to come down to closer to $2tn. to have a chance of placating moderate democrats Manchin and Sinema. Incidentally, Manchin has just been out saying he won’t support one idea Biden has floated, namely a vote to temporarily abolish the filibuster that would then prevent Republican Senators from running down the clock on a debt ceiling discussion on the floor of the Senate by talking incessantly (a ploy that prevented ‘Obamacare’ being approved the first time round in 2009).

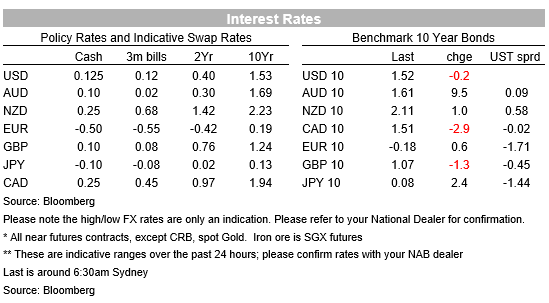

In truth markets haven’t been travelling with any real trepidation that the US might default on its obligations, but the news has at least played with the grain of the market turnaround. Bond yields have been little changed overnight, 10-year Treasuries currently 1.52%, while 10-year break-evens (market-implied inflation expectations) are 2bps lower versus Tuesday’s close, at 2.44%, after having been as high as 2.50% earlier in the day. The bigger news in break-evens this week has been in Europe, which in 10 year gilts jumped above 4% Wednesday for the first time ever and in Germany to above 1.8% for the first time since 2017. Both have eased back somewhat, in the UK from a high of 4.1% to 3.9% and in Germany from a high of 1.84% to 1.75%. Doubtless NAB’s inflation trader will be very excitable in today’s morning meeting.

In economic data, US ADP private payrolls beat market expectations with a 568k lift in September, a three month high. The data don’t always give a good steer for the key non-farm payrolls report due Friday night, but it won’t sway the consensus from its pick of 500k, a figure likely good enough to trigger the Fed into a QE tapering announcement next month.

In currency markets, the intraday turnaround in risk sentiment still leaves the JPY and CHF as the best performing G10 currencies, both fractionally higher against a USD that in BBDXY index terms is currently 0.2% up on Tuesday’s New York close. All other major currencies are softer against the greenback, with NOK -0.6% (on lower oil) NZD (-0.7%) and SEK (-0.7%) leading the way own. AUD had fared less badly, pulling up from an intra-night low of 0.7226 to around 0.7275 now, a fall of just 0.2%. So the NZD as fared particularly badly on a day when the RBNZ became the second G10 central bank to lift interest rates, but which was already very well anticipated by market. In contrast, a rate rise in Poland (from 0.1% to 0.5%) was wholly unexpected, lifting the Zloty by around 1%. A salutatory reminder that central bank thinking can turn on a dime, something central market watchers will need to be attuned to next yar.

Finally and for good order, yesterday, in a letter to authorised deposit-taking institutions (ADIs), APRA told lenders it expects they will assess new borrowers’ ability to meet their loan repayments at an interest rate that is at least 3.0 percentage points above the loan product rate. This compares to a buffer of 2.5 percentage points that is commonly used by ADIs today. In making the announcement, APRA noted that ‘ Putting aside the impact from other aspects of serviceability assessment (read: the forthcoming review about potential macro-prudential rules – currently expected centre on debt/income ratios (my words not APRA’s)) a 50 basis points increase in the serviceability buffer will reduce maximum borrowing capacity for the typical borrower by around 5 per cent. Given some borrowers are already constrained by the floor rates that lenders use, and that many borrowers do not borrow at their maximum capacity, the overall impact on aggregate housing credit growth flowing from this is expected to be fairly modest.”

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.