Coming in for landing in a heavy cross wind

Insight

The bond sell-off that dominated the early part of the week has been put on pause. Why? NAB’s Taylor Nugent says there are a number of factors, but it’s tomorrow’s non-farm payrolls that will really set the direction for early next week.

Events round-up

EC Retail Sales MoM/YoY August: -1.2% vs fcst -0.5% (-1.0%), previous -0.2% (-1.0%)

EC PPI MoM/YoY August: 0.6% vs fcst 0.6% (-11.6%), previous -0.5% (-7.6%)

US MBA Mortgage Applications September 29: X, previous -1.3%

US ADP Employment Change September: 89k vs fcst 150k, previous 180k

US Factory Orders August: 1.2% vs fcst 0.3%, previous -2.1%

US ISM Services Index September: 53.6 vs fcst 53.5, previous 54.5

US ISM Services New Orders September: 51.8, previous 57.5

US ISM Services Employment September: 53.4, previous 54.7

US ISM Services Prices Paid September: 58.9, previous 58.9

“Oh, we need to let it breathe” – Years and Years

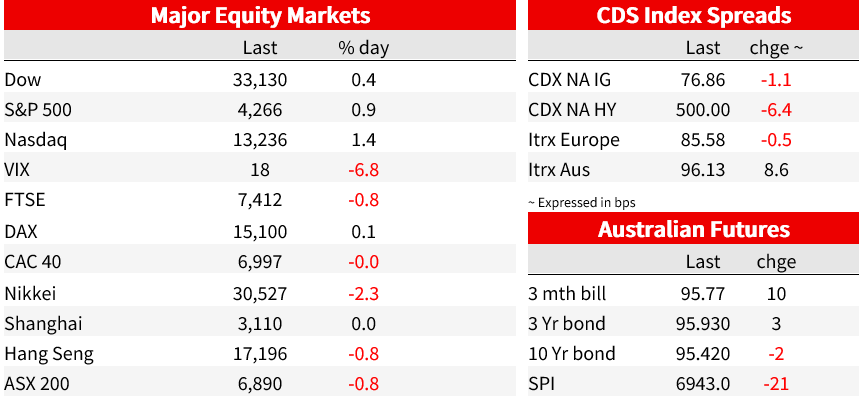

The selloff in bonds took a reprieve with yields lower across the curve after pulling back from new highs in European trade. The US Services ISM came in in line with expectations, while a softer-than-expected ADP employment change looks to have supported the move lower in yields despite its unreliability as a Payrolls indicator. The US dollar is a little softer on the DXY, equities are higher, and oil was 5% lower. The S&P500 closed up 0.8% rallying late in the session, fuelled by big tech. The Nasdaq was 1.5% higher.

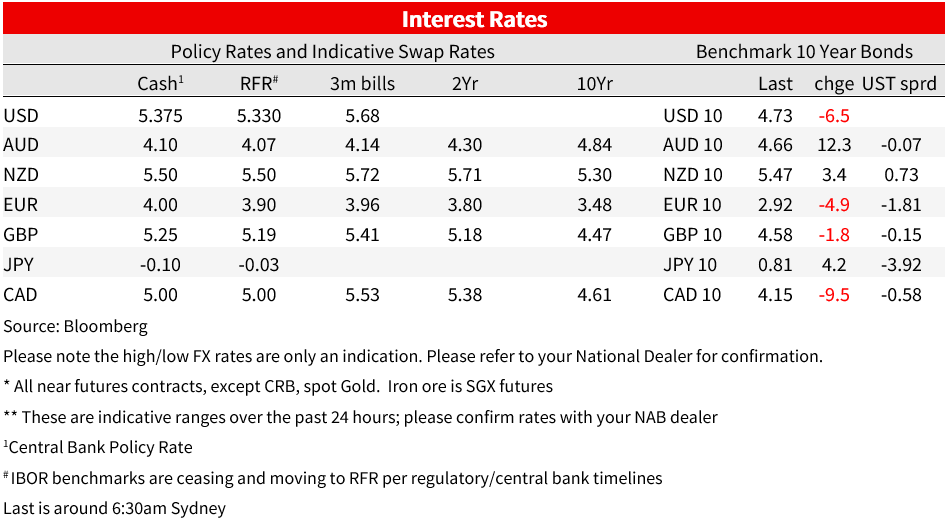

The pullback in bond yields came only after new highs were reached in European trade, with the 30yr yield briefly above 5%, and German 10yr bund yields above 3% for the first time in 12 years before retracing. The 30yr yield is 7bp lower over the day at 4.85%. US 10yr yields were 7bp lower to 4.73%. But contrasting the recent theme, the pullback in yields was led by the 2yr, the 2s10s curve continued to steepen, now at -32.3bp. The 2yr yield was 10bp lower at 5.05%. Near-term Fed pricing was also pared, with a November hike now priced at 24% from 30% yesterday.

ADP employment data was softer than expected at +89k. That’s a smaller increase than the 150k expected and 180k previous gain. While the contrast to stronger August JOLTS data the prior day helped support the move in yields, the rally had begun well ahead of the data and caution is warranted in reading into the ADP data. It has been an unreliable indicator for Friday’s official payrolls outcome, where consensus is for a 170k gain after 187k in August.

The US Services ISM was broadly in line with consensus, falling to 53.6 from 54.5. The contrast to the S&P Global Services PMI remains, the latter coming it at 50.1 in September (from the 50.2 preliminary read). Resilience in the services picture out of the ISM also contrasts the deeper softening, and recent recovery, in the Manufacturing ISM. Business activity was strong, up 1.5ppt to 58.8, though new orders slipped 5.7ppt to 51.8. Prices paid was stable at 58.9.

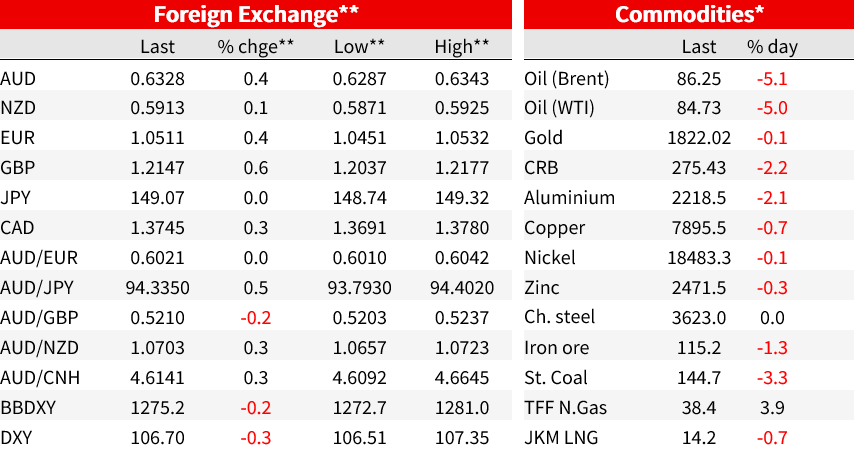

In currency markets, the US dollar lost 0.3% on the DXY. The euro was 0.4% higher to 1.0513. The AUD briefly dipped to 0.6287 intraday yesterday afternoon (Sydney time), around its year-to-date low of 0.6286 the prior day, though is higher on the day. The AUD gained 0.4% to 0.6332.

Oil prices slipped. Brent was down 5.1% to $86.25, to be down some 10.8% since 27 September. That’s welcome relief for near-term inflation if sustained, but for context only takes oil back to where it was at the end of August. Lower oil weighed on CAD and NOK, which were the worst performing G10 currencies with CAD down 0.2% against a broader weaker dollar.

USDJPY was little changed at 149.08. Japan’s top currency official, Masato Kanda yesterday wouldn’t confirm if there had been intervention to support the Yen after the rapid appreciation the prior day, where USD/JPY dropped from above 150 to 147.50 in a matter of seconds before staging a recovery. After the sudden bout the volatility, the market will be cautious particularly if USD/JPY moves back above 150.

The RBNZ left the Official Cash Rate unchanged at 5.5% at the Monetary Policy Review yesterday. The accompanying statement suggested there is little change in the Bank’s assessment from the August Monetary Policy Statement. While noting ‘interest rates are constraining economic activity and reducing inflationary pressure as required’, there was some suggestion that rates may need to stay elevated for longer than it had previously forecast, “ Interest rates may need to remain at a restrictive level for a more sustained period of time.”

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.