NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

If the market is rethinking how soon the Fed might lift rates, there was nothing from incoming Fed speakers overnight to support this view.

https://soundcloud.com/user-291029717/earnings-anything-but-a-damp-squid?in=user-291029717/sets/the-morning-call

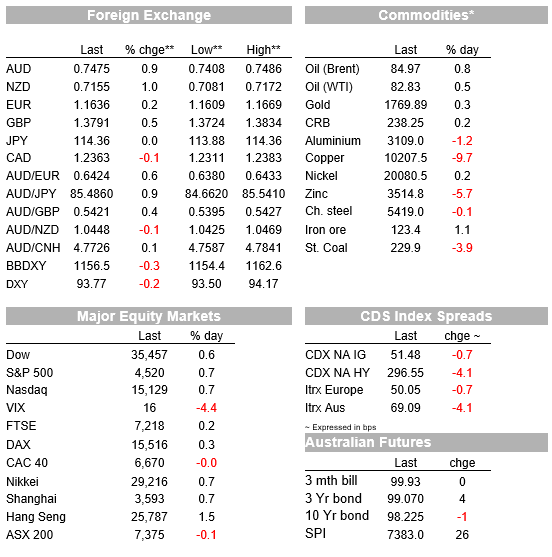

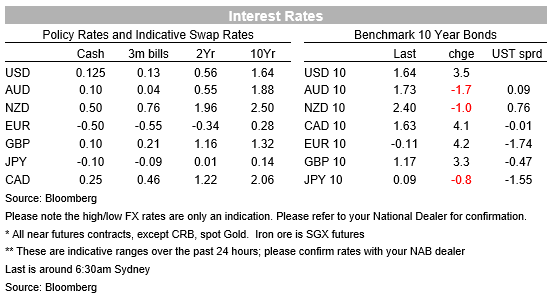

Risk sentiment remains in the ascendancy with US stocks just closing with gains of 0.6-0.7% for the main board indices in front of Netflix’s earnings , reported right on the closing bell and which show an increase in its Q3 steaming subscribers of 4.38m well above the 3.75m street estimate, and its Q4 estimate at 8.50m against 8.32m expected (doubtless the Squid Games effect). Earlier, Travelers and Johnson & Johnson both beat their street estimates while P&G did not, lamenting high freight costs as imposing a squeeze on its margins. Stocks might also have been helped – and in foreign exchange market the USD hurt – by a fall-back in front-end US yields (e.g. by 3bps at 2-years) so symptomatic of a slight paring back in expectations for when Fed rates ‘lift-off’ might occur. 10-year Treasuries in contrast have reversed their earlier yield declines to be finishing the New York day +4bps at 1.64%, their highest level since 20 May.

If the market is rethinking how soon the Fed might lift rates, there was nothing from incoming Fed speakers overnight to support this view. Fed Governor Christopher Waller has in the last hour been out saying he’s “’greatly concerned” about upside inflation risks, and while he still believes rate lift-off “is still some time off” adds that the next several months will be “critical” for assessing inflation dynamics and that if inflation doesn’t moderate by year end, (the Fed) ‘could bring forward rate hikes”.

Earlier Tuesday, Fed Governor Michelle Bowman said she supported a start of tapering this year (and preferably in November) to end in mid-2022, saying she thought the remaining benefits to the economy from Fed asset purchases are now likely outweighed by the potential costs, in particular, that they could now be contributing to valuation pressures, especially in housing and equity markets. She says she sees a “material risk that supply-related pricing pressures could last longer than expected” and which if they continue into and through the next year, “may begin to see an imprint on longer-run inflation expectations”.

The message from incoming Fed speak seems pretty clear. Inflation is going to have to be seen to be moderating, and quite significantly so, either side of year-end for markets – and indeed the majority of Fed members – to be convinced that late in 2022 is the absolute earlier that rates lift-off is likely to occur.

If Fed speak is doing nothing to discourage thinking about 2022 Fed rate hike(s), some of the incoming US real economy might. US Housing Starts for September came in weaker than expected, falling by 1.6% to an annual rate of 1.555 million (1.615m expected) and permits by much more, down 7.7% to a 1.589m annual rate. Also catching your scribe’s eye and more telling perhaps, the Federal Reserve Bank of Atlanta’s GDPNow index suggests U.S. GDP expanded by just 0.5% in Q3 (that’s an annualised rate) down from their prior estimate of 1.2% and a 3.5% consensus in the latest Bloomberg survey. Readily dismissed as ‘covid-related’ perhaps, but if so we will need to see hard evidence of a strong bounce back in Q4 data.

Back to central banks, and in this part of the world, yesterday’s RBA Minutes revealed a further push back against market pricing, that is currently little different for the RBA next year than it is for the Fed, the Minutes saying, “Members noted that patterns in wages growth differed across advanced economies. Some economies that were experiencing a pick-up in wages growth, such as the United States and the United Kingdom, were also those that had experienced relatively fast wages growth and higher inflation prior to the pandemic.” We’ve had ECB chief economist Philip Lane out stealing a recent line from RBA Governor, saying, “If you look at market pricing of the forward interest rate curve, I think it’s challenging to reconcile some of the market views with our pretty clear rate forward guidance”.

An interesting 24 hours in FX markets. Last week, the DXY USD index was pushing to new 2021 highs above 94.50, but on Thursday was at one point more than 1% down on this level (93.50). The aforementioned rethink on the Fed was being mentioned in some quartesr, an too the (highly belated) realisation that whether the Fed raises rate in 2022 or not until later, other central banks are getting in ahead of them – In New Zealand and Norway already of course – plus large parts of the Emerging Markets universe – and with the Bank of England likely next cab off the rank as early as next month.

GBP continues to get no love from BoE repricing beyond what is coming from a weaker USD . Tightening into significant economic headwinds is never a great look for a currency, and on top of the various ones blowing in the UK economy’s face and slated for next year (tax rises), a Bloomberg source report overnight says the U.K. Treasury is resisting pressure to increase spending in next week’s budget because of concern that doing so would backfire by prompting the Bank of England to raise interest rates more aggressively. Government spending itself can cause inflationary pressures that would add to pressure on the BOE to tighten monetary policy, a Treasury official ‘familiar with the government’s thinking’ said.

Partly in the context of a weakening USD but also ongoing strength in energy prices and so the positive terms of trade effect for Australia, AUD could do no wrong yesterday, pushing just above the early September high of 0.7478 to 0.7486, though has pulled back 10 pips or so into the New York close. On fuel prices, yesterday Russia has, perhaps unsurprisingly, been out saying that Europe won’t be getting a step up min gas supply in the absence of it approving the sue of the Nordstream 2 pipeline.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.