Total spending grew 0.9% in June.

Inflation fears continued to build amid the backdrop of a strong Q3 earnings season which is showing firms have some pricing power to pass on higher transitory inflation

https://soundcloud.com/user-291029717/banks-ready-to-tighten-biden-ready-to-spend?in=user-291029717/sets/the-morning-call

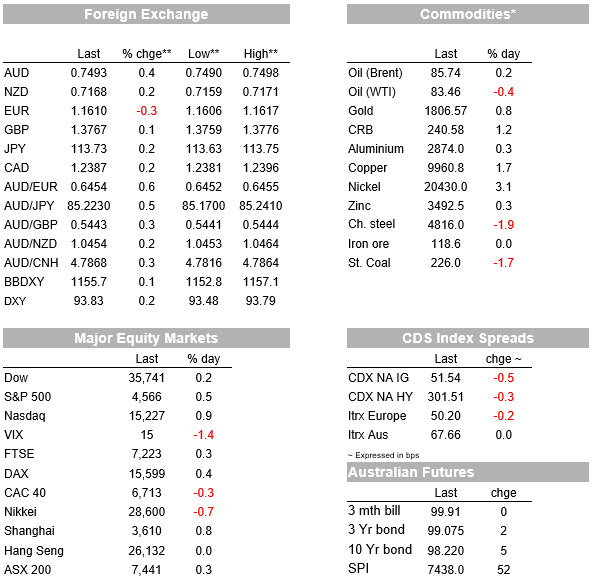

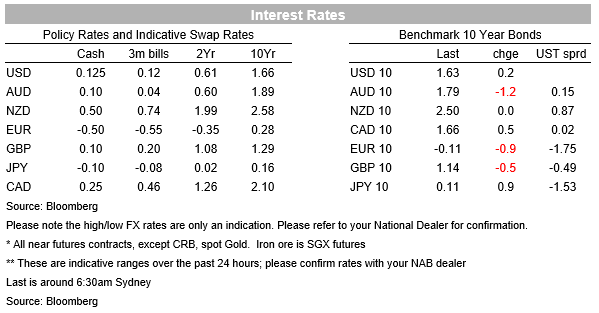

Market sentiment was broadly stable overnight with no top-tier data or significant news events of note. Inflation fears though continued to build amid the backdrop of a strong Q3 earnings season which is showing firms have some pricing power to pass on higher transitory inflation (note firms also said they would be focusing on enhanced cost management). Breakevens lifted with the US 10yr implied inflation breakeven up 4bps to 2.68%, driven by a fall in the real yield of -3.8bps to -1.04% (note the nominal 10yr was flat at 1.63%). Across the pond the UK 10yr breakeven hit a 25 year high at 4.2% and the closely watched Euro 5Y5Y inflation swap hit 2.0% to be its highest since 2014. Markets are still expecting central banks to respond to these pressures with the BoE still well priced for a rate hike at the next meeting in November, while for the US Fed a rate hike is fully priced by July/August 2022 and for the RBA by August 2022.

Equity markets so far have been little fazed by yield moves with the S&P500 so far up +0.5% overnight to be at a new record high. Driving the strength was materials and energy on the back of commodity prices amid signs of progress on the US infrastructure packages. Senator Manchin, one of two centrist Democrats opposed to the huge price tag on Biden’s social spending bill, said he expects to agree a framework on the package this week. That may also pave the way for a vote in Congress on the $550m infrastructure package. Manchin continues to insist the larger social spending bill shouldn’t exceed $1.5tn, which is well below the initial want of $3.5tn. Equity markets have also shown little reaction to China’s latest virus cases which has seen some parts of Inner Mongolia under enhanced restrictions. China continues to pursue a zero-COVID strategy which threatens to keep disrupting supply chains.

Also helping to drive equities higher was Tesla which rose 12% to a new record and surpassing $1 trillion in market cap after Hertz said it would buy 100k tesla’s to transition its rental fleet towards electric. Focus will likely remain on equities with 316 S&P500 companies reporting over the coming fortnight. Key names include Facebook which reports after the bell, followed by Twitter and Alphabet later today, and on Thursday Amazon, Apple. Of the 117 companies in the S&P 500 that have reported earnings to date, 84% posted numbers that beat expectations.

Energy prices still appear to show no let up to the current rally with Brent oil rallying above $86/bbl after Saudi Arabia urged caution in boosting supply. Brent oil is currently trading at $85.74. Saudi Prince Abdulaziz bin Salman said oil producers shouldn’t take the rise in prices for granted because “we are not yet out of the woods” regarding the pandemic and that “We need to be careful. The crisis is contained but is not necessarily over. ” At the moment at least it doesn’t appear OPEC will ramp up production greater than its current schedule. Reports of the energy crisis in China starting to ease and of Evergrande making its USD interest payments also appear to have supported sentiment overall.

FX markets have been relatively calm with the broad USD BBDXY +0.1%, mainly driven by EUR which fell -0.3%. Most major pairs are within +/-0.3% against the USD. Commodity currencies outperformed given the rise in oil with the AUD +0.4% to 0.7493 and NZD +0.2% to 0.7168. GBP (+0.1%) showed little reaction to the BoE’s Tenreyro who pushed back on the need for rate hikes. Tenreyro noted “ If the effects of supply-chain disruption on CPI inflation are short-lived, then attempting to use monetary policy to offset them would only serve to add additional volatility, since the effects would be fading by the time policy was having a major impact on inflation.” Alongside Catherine Mann and Jonathan Haskel, there could be three possible dissenters to a near-term BoE rate hike amid the nine member MPC.

Note inflation is starting to bite in the UK with low-paid workers in the UK set to receive a 6.6% pay rise from next April as ministers seek to soften the impact of rising living costs by lifting the national living wage. Data has been sparse. The German IFO Busines Climate missed expectations at 97.7 against 98.0 expected. The survey highlighted supply problems are giving businesses headaches and that capacity utilization in manufacturing is falling. Friday’s European PMIs highlighted similar themes, although the Eurozone manufacturing index remains relatively elevated on a historical basis, at 58.5.

A very quiet day with no top tier data in Australia or globally. Domestically there is the usual Weekly Consumer Sentiment reading with a rise likely given re-opening in VIC. Earnings season also continues with Twitter and Alphabet reporting. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.