Robust growth for online retail sales observed in June

Insight

Reaction to the Israel-Hamas conflict triggers a spike in energy prices while German Bunds lead a rally in European bonds with US Treasury futures also pointing to a decline in US Treasury yields. Not all the initial moves have been sustained. The USD is little changed, AUD is up, after being down with Fed speakers favouring holding rather than hiking rates, helping US equities rally while European shares fall.

Events Round-Up

GE: Industrial production (m/m%), Aug: -0.2 vs. -0.1 exp.

.. you’re sending me mixed signals – Robbie Williams

Reaction to the Israel-Hamas conflict triggers a spike in energy prices while German Bunds lead a rally in European bonds with US Treasury futures also pointing to a decline in US Treasury yields (the Treasury market is closed for Columbus Day). The USD is little changed with gains in JPY, CHF and commodity linked currencies offset by declines European pairs. Fed speakers favour holding rather than hiking rates, helping US equities rally while European shares fall.

The attack on Israel by Hamas has engulfed markets’ attention with Israel declaring war on Hamas, mobilising 300,000 reservists alongside a “complete siege” of the Gaza strip. PM Netanyahu said “we are just getting started…we are going to change the Middle East”. The market remains very concern over the potential for the war to escalate into other fronts and players . Israel has reportedly tackled threats on multiple fronts, particularly from Lebanon in the north while President Biden warned “against any other party hostile to Israel seeking advantage”

The initial reaction to this major geopolitical event triggered a bout of risk aversion at the Asian opened with risk assets in Europe also coming under pressure overnight while German bunds led a rally in European bonds (10y Bunds down 11bps to 2.772%). The US treasury market is closed for Columbus Day, but US Treasury futures have rallied implying a decline in 10y UST yields of around 12bps to 4.66%. Oil prices also spiked at the opened, gaining over 5% during our Asian trading session yesterday with LNG prices gaining even more overnight, up close to 15% in Europe.

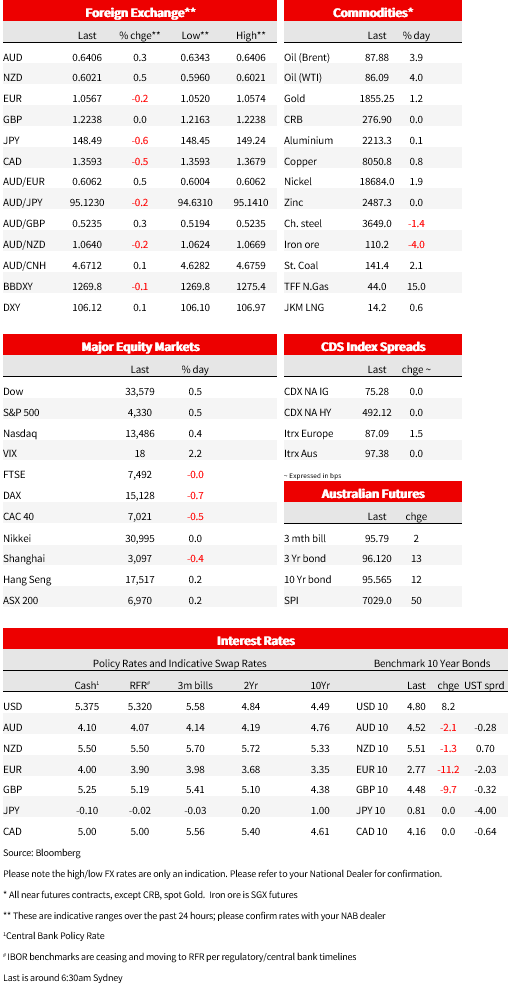

That said, it is interesting to note that the magnitude of the moves has been relatively contained and, in many instances, not all the moves have been sustained. For instance, the USD went bid during our APAC yesterday, but now is little changed with safe haven pairs retaining their initial gains (USD/JPY -0.5% to 148.44, CHF +0.3% to 0.9056) while initial declines recorded by risk sensitive pairs, such as the AUD and NZD have now been reversed with both antipodean pairs now up 0.3% and 0.5% respectively (Fed speaker a supporting factor, more below) to 0.6411 and 0.6024. Meanwhile GBP is unchanged at 1.2238 and the euro is down 0.2% to 1.0569, after trading to an overnight low of 1.0521.

US equities are the other notable risk asset recording a big u turn . For instance, the S&P500 opened down ½%, but then halfway through the overnight session it staged a recovery and later it moved back into positive territory. The S&P 500 has now ended the day with gains over 0.5% while the NASDAQ is +0.38%. Meanwhile, earlier in the session all regional European indices closed in negative territory with the Euro Stoxx 600 index ending the day 0.3% lower.

Oil prices have retained most of the initial gains with both Brent and WTI up close to 4%, after spiking above 5% at the Asian opened. Notably, however, gas prices have recorded the largest gains with TFF NAT Gas future up 15%. News from Israel may have played a part on the latter with Bloomberg reporting Chevron was instructed by Israel’s Ministry of Energy to shut production at the Tamar natural gas platform in the eastern Mediterranean. The market remains very sensitive to the risk of further ramifications from the Israel-Hamas conflict, suggesting volatility particularly in the energy sector is likely to remain elevated with Iran a major concern here. Intelligence reports suggesting Iran helped plan Hamas’s surprise attack on Israel but Iran’s representative to the UN denied that the country was involved in the attack.

Another factor playing into the u turn in US equities and the extension seen in the move up in US Treasury futures has messages coming from Fed speakers. Dallas Fed President Logan said that higher long-term rates mean less need for rate hikes viz “ …if term premiums rise, they could do some of the work of cooling the economy for us, leaving less need for additional monetary policy tightening”. My BNZ colleague, Jason Wong, rightly noted that Logan’s comment looked like a dovish shift from an FOMC member who is seen to be more on the hawkish side of the spectrum, although she added that “to the extent that strength in the economy is behind the increase in long-term interest rates”, the Fed may need to tighten more.

Later in the session and arguably having a bigger impact on the move up in US equities as well as gains in risk sensitive currencies such as the AUD and NZD, Fed vice-Chair Jefferson said that the Fed is “in a position to proceed carefully in assessing the extent of any additional policy firming that may be necessary …I will remain cognisant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy”.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.