Robust growth for online retail sales observed in June

Insight

US CPI reverses much of the earlier week market moves

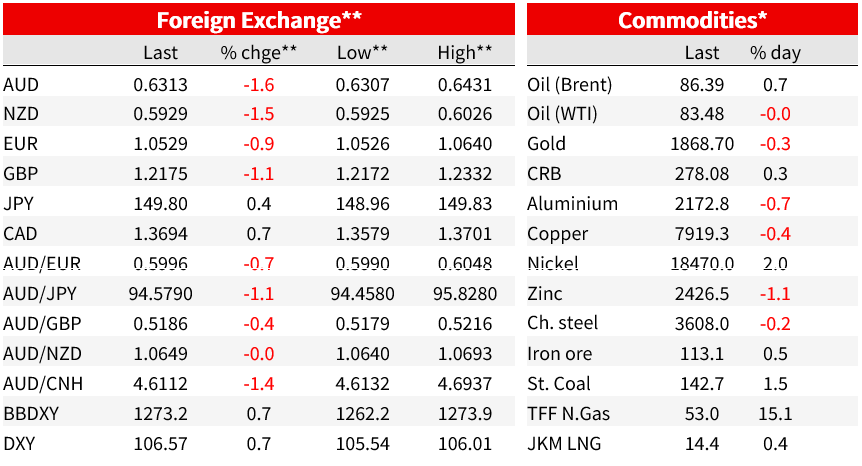

Much of the ‘good’ work done in the past week in the form of bull flattening of the US yield curve has been undone by the latest US CPI report, which shows in particular still uncomfortably high core service sector inflation. This has pulled odds of further Fed tightening back up to around 40% from below 30% earlier in the week. The USD has bounced back with AUD (-1.5%) followed by NZD (-1.4%) the primary victims. This is notwithstanding the fact European gas prices have shot up another 15% to now be 45% up since Hamas’ assault on Israel. This is now a significant negative terms of trade shock for Europe heading into the Northern Hemisphere winter and which in recent years past has been a significant negative currency force for gas-dependent European countries. Yet EUR/USD is off ‘only’ 0.8%.

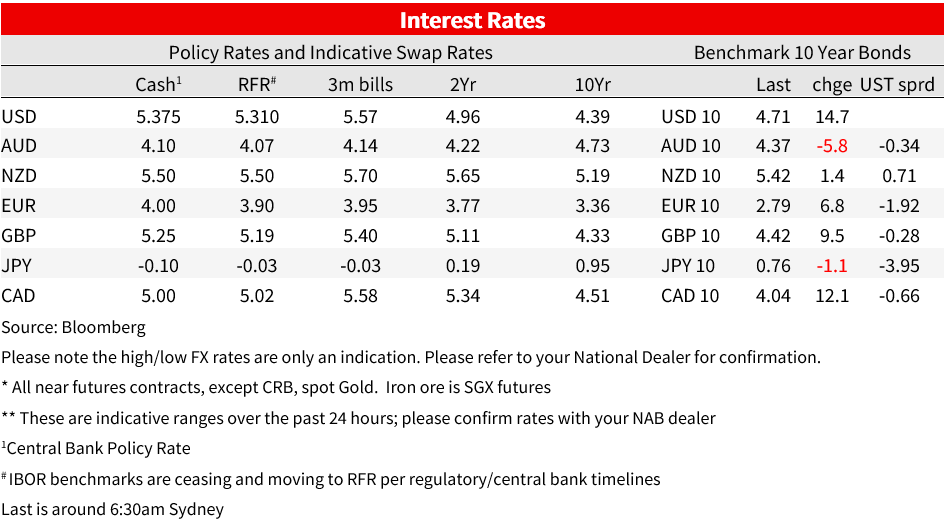

The main economic event of the week, US September CPI , saw the headline come in at 0.4%, above the 0.3% expected, for an unchanged 3.7% yr/yr rate. The core (ex food and energy) series rose by 0.3% as expected for a fall to 4.1% from 4.3%, in line with expectations,. But the devil was in the detail, in particular higher than hoped for core services inflation, contrasting with better-than-expected news on good inflation. Core good inflation fell by 0.4% on the month, to be down 3.2% year to date on an annualised basis, with an 18% fall in used car prices the biggest contributor. Core services prices (ex-energy) in contrast rose by 0.57% on the month and on a year-to-date annualized basis are running at 5.7%. Our friend Phil Suttle at Suttle Economics calculates the so-called supercore CPI measure (services ex-energy, rent and shelter) also at 0.57%, with gains averaging 0.44% per month though Q3 up from 0.34% in Q2.

The other piece of US economic news overnight was weekly initial jobless claims, matching the prior week’s low 209k, in line with expectations. Elsewhere, UK monthly GDP for August showed a 0.2% rise in line with expectations, for 0.3% on a 3M/3M basis, also as expected.

On the central bank front, nothing new from Fed officials overnight, while the ECB’s account of its September meeting were consistent with the claim made after the meeting that the ECB thinks it may have done enough to get inflation back to target. Noted ‘non-consensus’ ECB hawk Holzmann has been out again saying he doesn’t see inflation getting back to 2% without a recession in the Eurozone, while the Slovenian ECB GC member Vasle– also considered a hawk –said the ECB should be considering all options in regards to the next step for QT. The ECB’s Wunch, also deemed a hawk, sounded more conciliatory, saying ‘we don’t have to hike anymore’ if inflation numbers keep aligning with the ECB’s forecast.

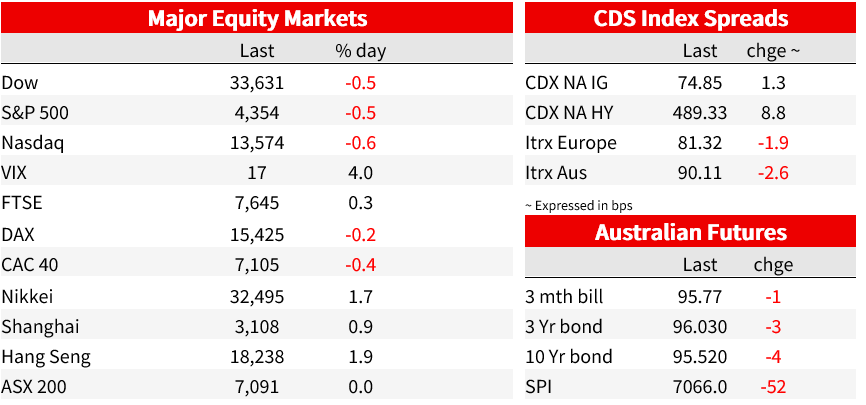

The renewed sell off in US bond market post-CPI, and which also showed up in rise of 7-10bps for European 10-year government bonds, has been exacerbated by a poorly received US 30-year auction, which tailed 4bps above the pre-action when-issued yield. The 30-year is currently up 16bps on the day to 4,86%, 10s up 14bos to 4.70% and the 2-yar +8bps at 5.07%. Australian 10-year futures show an implied yield of about 10bp up on Thursday’s local close.

In FX, USD weakness in the past week or so has been driven primarily by the bull flattening of the US yield curve, aided by various Fed officials pointing to the tightening of financial conditions implicit in the recent back up in longer dated bond yields as obviating the need to be lifting policy rates again, at least for now. No surprise therefore that the renewed bear steepening of the US curve post-CPI has seen a chunk of these losses reversed. The DXY index is currently 0.7% on the day to now be less than 0.5% below its (October 3) YTD high of 107.0.

By currency pair, it is AUD/USD (-1.4%), NZD/USD (-1.4%) followed by GBP/USD (-1.1%) showing the biggest losses. Were it not for the prevailing level near ¥150, USD/JPY would doubtless have been giving these currency pairs a run for their money, but JPY is off just 0.4% to be the ‘least weak’ G10 currency. At ¥149.80 or thereabouts as I type, FX markets will be on BoJ intervention watch this morning.

Coming into the close, the S&P500 and NASDAQ are each showing loss of just over 0.5%, after a European day which saw the FTSE up 0.3% but most Eurozone bourses down by a similar amount. Finally in commodities, oil prices remain little changed, having now given back all of the knee-jerk gains evident on Monday morning. But the TTF European benchmark gas price is up another 15% to now be 45% up on the week, on mounting concerns about supply shortages tunning into the winter after the earlier reported outages in both Israel and Finland.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.