NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

There was a mixed market reaction to the better than expected US Payrolls print on Friday with equities up, yields down and the USD lower.

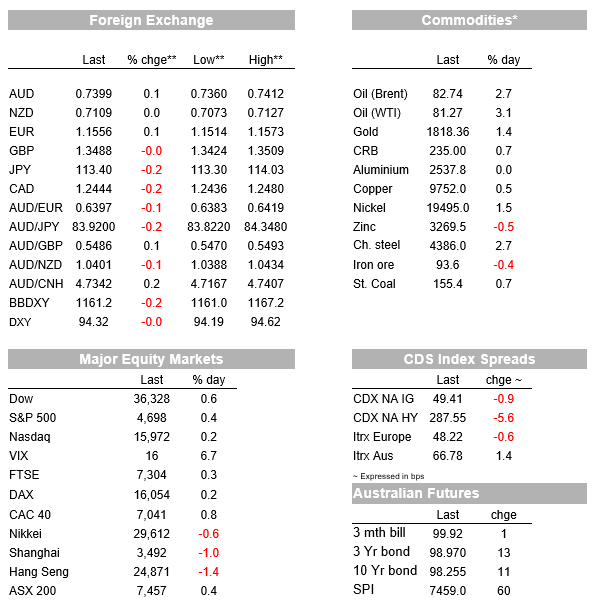

There was a mixed market reaction to the better than expected US Payrolls print on Friday (Payrolls +531k vs. 450k expected; and +235k in revisions) with equities up (S&P500 +0.4%), yields down (US 10yr -7.5bps to 1.45%) and the USD lower (BBDXY -0.2%). While yields did initially rise after the payrolls print and on hawkish commentary from the Fed’s George, another slide in UK Gilt yields on Friday more than outweighed with the BoE’s shock on hold decision Thursday still ricocheting through markets. Media reports suggest heavy losses in some bond funds which may be leading to exaggerated moves in markets. Meanwhile BoE officials aren’t helping with Governor Bailey saying the BoE MPC won’t “bottle it” in hiking if necessary in December, while Chief Economist Pill sounded more cautious fearing higher rates would damage the recovery from the pandemic “in a misguided attempt to clampdown on short term price pressures”, sentiments echoed by fellow MPC member Tenreyro.

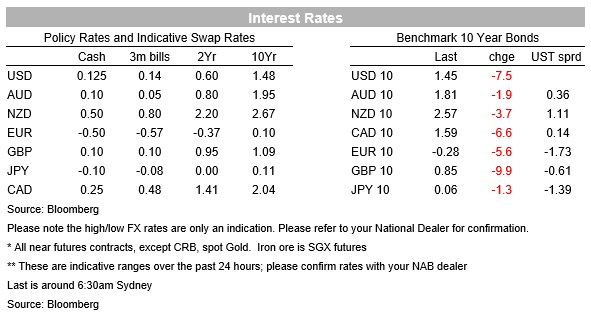

Looking closer at yields it was a messy Friday, and a very messy week. Overall US 10yr yields were down -7.5bps to 1.45%, after having moved up to 1.55% after the payroll number, with the slide in UK yields seeing the US 10yr hit a low of 1.4340%. While the move in US yields is broadly in line with the -9.9bps fall in UK 10yr Gilt yields to 0.85%, key moving averages have been broken with the 50day at 1.46 and 200day at 1.45. Real yields moved in sync with nominals with 10yr TIP yields -6.1bps to -1.10%, meaning the implied inflation breakeven was little moved at 2.55%. Curves flattened with the US 2s10s curve -9.8bps to 104.5bps. Fed Funds pricing has also moved out with a full rate hike now fully priced by September 2022 (previously July 2022) with a second not until February 2023 (previously December 2022). Aussie futures followed the move in global rates with the implied yield on the 3-year and 10-year futures closing down 9bps and 9.5bps respectively

As for the US jobs data it was undeniably strong, showing the US is moving past the delta outbreak with widespread jobs growth amongst industries. Headline payrolls were +531k against 450k expected, while importantly there were revisions of around 235k to the prior two months. The unemployment rate also fell by two tenths to 4.6% (consensus 4.7%) and is now around a percentage point away from its pre-pandemic level of 3.5%. Average Hourly Earnings growth also remained strong at 4.9% y/y – though some were fearing an upward surprise on this given the anecodtes. Relative to pre-pandemic levels payrolls are now 4.2m below February 2020 levels or 2.8% below, with around a third of those jobs that have yet to be recovered in the ‘leisure and hospitality’ sector. At the current trend payrolls pace of 450k, it would take around 9 months to recover to pre-pandemic levels which means the US could be at what some consider to be maximum employment by July 2022. That keeps alive the possibility of multiple hikes in H2 2022, while also not justifying an acceleration in the taper profile.

Equities lifted in the wake of the jobs numbers with the S&P500 +0.4% and is up 2% on the week with seven straight days of consecutive gains . The pivot towards re-opening gained further momentum after Pfizer said its latest COVID-19 drug used in combination with an HIV drug, cut the risk of hospitalisation by 89%. Bullish remarks by Pfizer Board Member and former-FDA commissioner Dr Gottlieb also added; he noted “By Jan. 4, this pandemic may well be over, at least as it relates to the United States,” at which point “we’ll be in more of an endemic phase of this virus,” also contributed (see CNBC: Pfizer board member Gottlieb says the Covid pandemic could be over in the U.S. by January ). No surprises then to see the broader Russell 2000 up 1.4% and over the week the Russell 2000 is up an incredible 6.1%. Travel/leisure stocks outperformed: United Airlines +7.3%; American Airlines +5.8%; Carnival +8.3%; Expedia +15.6%. Thematically the move lower in real yields seen over recent days is also supportive to equities.

Also in positive news, the first infrastructure package has been approved by Congress. Although the headline is $1.2 trillion, in reality new spending comprises only around $550bn over five years. The passage of the package has been fraught even though it was initially bi-partisan with the bill passing the House 228 v. 206, with the Democrats needing Republican votes given six Democrats voted against; only 13 Republicans obliged to help pass the bill. That is a bad omen looking to the mid-terms next year where President Biden is looking like he may become another lame duck if the Democrats cannot hold onto the House. As for the second infrastructure package worth $1.75tn, that still remains very uncertain with passage dependent on Democrats Manchin and Sinema via the budget reconciliation process in order to avoid an almost certain Republican filibuster.

FX market moves were modest on Friday, with the G10 currencies all contained to within +/-0.3% against the USD. The EUR hit a new year-to-date low immediately after payrolls, but recovered to finish 0.1% higher, at 1.1570. The policy divergence between Europe and the US is becoming clearer with ECB officials pushing back on notions of a 2022 hike, while Fed officials have previously opened the door to hikes in 2022. The Fed’s George on Friday (typically hawkish and 2022 voter) stuck to a mildly hawkish tone, noting that price increases were becoming broader (“while in the spring the increase in prices was being driven by select categories of goods and services, more recently the increase in prices has become generalized, and is apparent across a broad swath of the economy”) and that the labour market was tight with the Fed watching whether the participation rate lifts in response. The AUD and NZD followed a similar pattern, with the AUD ending up 0.1%, at around 0.7399. The AUD was the weakest of the majors last week, down 1.6%, after the RBA’s dovish messaging at its November board meeting. Followed then by GBP which has fallen 1.4% over the past week.

Central bank speak was mixed, emphasising the confusion that has beset rates markets over the past week. BoE officials tried to justify why they remain hawkish even though they wrongfooted the market. Chief Economist Pill said the decision was “a knife-edge decision” with still “some need ” for rate hikes, while also balancing those comments by noting that he feared that higher borrowing costs at the moment would damage the recovery from the pandemic “in a misguided attempt to clampdown on short term price pressures”. Those comments were echoed by known MPC dove Tenreyro who emphasised the risk of acting to early: “if you react immediately to inflation without waiting on what’s going on in the real economy, the risk is that you choke off the recovery and delay the renormalization of the economy”. Governor Bailey meanwhile kept the hawkish tone saying the BoE would not “ bottle it” and in response to a question: “interest rates need to rise … I’m not going to endorse 1%, but … it’s correct to think in those terms.” (see: Reuters: After market mayhem, BoE officials say rate hike still on table).

Closer to home, the RBA’s Statement of Monetary Policy on Friday didn’t provide any major surprises. The RBA’s central case, predicated on inflation increasing only very gradually, is still that the initial rate hike in the cycle will come in 2024 while its upside scenario implied lift-off in early 2023. While the RBA can clearly see the case of a 2023 hike, the SoMP again ruled out a 2022 hike (“in the Board’s view, the latest data and forecasts do not warrant an increase in the cash rate in 2022 ”). NAB’s view is that the RBA will raise rates from mid-2023 with a relatively aggressive series of hikes thereafter to bring the cash rate to 1.75-2.0% by the end of 2024. The aggressive series of rises reflects a view that by waiting for actual outcomes for wage and inflation to be consistent with target, the RBA will need to normalise rates quickly once sustainably higher inflation is achieved amid forecasts for a historically tight labour market.

In other news PM Morrison has indicated he will loosen the external boarder before Christmas to alleviate skills shortage. The AFR reports government sources as saying “ Resources, healthcare, agriculture, infrastructure and engineering will be among the industries prioritised to fill skill shortages as the Morrison government plots the return of foreign workers by Christmas. Hospitality businesses struggling to find staff to serve customers and man kitchens will also receive a fillip with working holidaymakers to be welcomed back as a matter of urgency) (see AFR: Miners, nurses and baristas first to be welcomed back). As for the next Federal Election, background briefing suggests the PM is going to wait until May 2022 to capitalise on an expected strong rebound in the economy (see AFR: Election in May on economic rebound looms).

A very quiet day with no data scheduled domestically. Offshore most focus will be on Fed speakers to gauge the implications of Friday’s stronger than expected payroll numbers on Friday. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

Confidence and Conditions Lift

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.