Online retail sales growth slowed in May following a fairly strong April

Insight

US equities close slightly higher while Europe starts the new week on the back foot.

US equities close slightly higher while Europe starts the new week on the back foot. Core yields reverse some of Friday’s decline with breakevens driving the move up while real yields are pushed lower- 10y UK real yields and 30y US real yields make new record lows. Good night for commodities and pro-growth FX, NZD leads gains in G10.

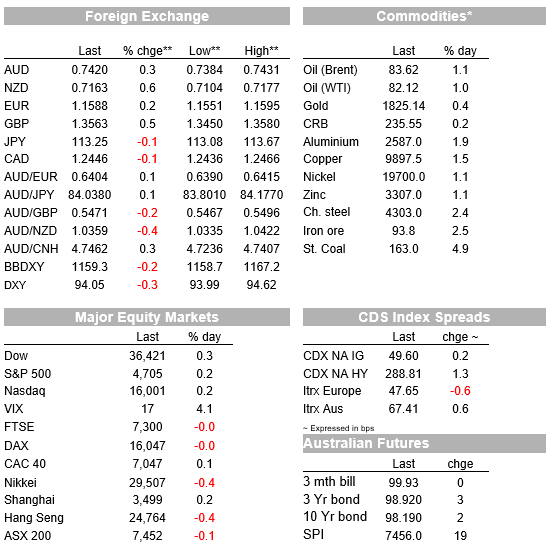

After opening higher and then trading lower, US equities have managed to eke out small gains at the start of the new week. In the process the S&P 500 extends its winning streak to an impressive eight consecutive day, closing Monday’s session up 0.16%. Materials and Energy led the overnight gains (1.20% and 0.85% respectively) with defensive sectors underperforming, Utilities down 1.55%. The NASDAQ closed 0.21% higher, despite a 2.8% decline in Tesla shares (initially almost 10%) after Elon Musk asked his Twitter friends if he should sell 10% of his $210bn stake on the company.

In contrast European investor have started the new week on a more cautious mood with most major regional indices closing Monday’s session with small losses . That said the Stoxx 600 index managed to stay in the green up 0.04% and similar to the US, energy and mining shares outperformed as base metals and oil prices rose. Worth noting that, just like the US, European equites are enjoying a nice purple patch, up for five weeks in a row amid optimism companies can weather the challenges from rising input cost and supply chain disruptions.

To some extent the lacklustre equity start to the new week is somewhat disappointing, particularly when we look at the US. Positive news have come and gone without much fanfare, over the weekend, Congress passed the $550b infrastructure bill, which would have done no harm to market sentiment, the weekend Pfizer Covid pill news is great news for the fight against the virus and overnight the US reopened its borders to citizens of 33 countries who had been barred by Covid-19 restrictions for more than 18 months.

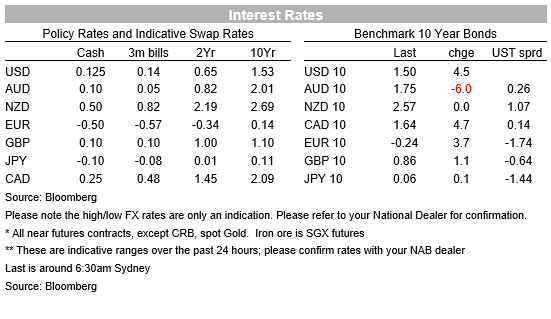

Inflation concerns may have something to do with the sedated sentiment in markets. After the big moves last week, core nominal yields have risen overnight with the 5 year part the curve leading the move up in the US, up 6bps to 1.114% while the 10y Note gained 4.4 bps to 1.498%. Core yields in Europe also traded higher with 10y Bunds up 3.7bps to -0.24% while 10y UK Gilts gained 1.8bps to 0.856%. Digging deeper into the moves, gains in nominal yields has been driven by a lift in the breakeven component while real yields have been pushed lower. The yield on UK 10-year inflation-linked bonds fell as much as 3 bps to minus 3.19%, surpassing a previous low hit in December 2020. It comes after the equivalent rate on 30-year linkers hit an all-time low on Friday. In the US, the 30-year TIPS yield fell as much as 6.3 bps to minus 0.508%, also a new record low. 10y US break evens rose 6bps to 2.61% overnight with 10y TIPS down almost 2bps to -1.11%.

On this score and against a light flow of data releases, the NY Fed’s monthly survey of household inflation expectations showed the year-ahead rate lift from 5.3% to 5.7% while the 3-year ahead rate was steady at 4.2%, both at their highest level since the survey began in 2013. CPI inflation data later this week is expected to record a lift to 5.9% y/y in October, so the near-term expectations data are not out of whack.

After last week’s Fed policy update, the speaking circuit has begun, for which we’ll hear a lot of divergent views from FOMC members. Fed Vice Chair Clarida stuck to the script, saying he expected this year’s surge in inflation to ease as supply and demand imbalances fade over time. He expected the Fed to meet its goals for raising rates by the end of 2022 and that median Fed projections for rate rises in 2023-24 seemed appropriate. That said, he added most Fed officials see risks of higher than anticipated inflation.

St Louis Fed Bullard reiterated his hawkish credentials, arguing that “this is one of hottest labour markets we’ve seen” and that he had two rate hikes for next year pencilled in. As expected, Governor Quarles will be leaving the Fed and this will happen in the last week of December, giving President Biden another slot to fill. And early this morning Fed Evans said “I expect that the currently elevated inflation readings from supply side pressures will eventually fade,”, but he then added that “Rents and homeownership costs have accelerated in recent months…These developments deserve careful monitoring and present a greater upside risk to my inflation outlook than I had thought last summer”.

So, the conclusion is that just like the market, Fed officials are not a hundred percent sure how inflation dynamics will play out. If price pressure remain elevated, then next year the Fed will be force to lean against them even if the maximum employment has not yet been reached.

European gas prices rose 5-10% as it became clearer that Gazprom won’t be helping out to add supply, saying that it won’t sell any spot fuel via its sales platform this week and it didn’t book any extra supply capacity for Europe at the weekend auction. The Kremlin said that Nordstream 2 approval would help, making it obvious that politics was playing a role, with Russia likely only helping if it served its long-term interests. Oil prices have begun the week on a positive note, up about 1%.

FX markets have also started the new week in a subdued manner, still the buoyancy in equities and uptick in metal prices (aluminium +1.98% copper +1.25%) benefited pro-growth currencies with USD indices down between 0.15% and 0.3% . NZD has led the gains in G10, +0.66% to 0.7162%, news of an ease in covid restrictions in Auckland boosted the kiwi, although my colleague Jason Wong notes that he doesn’t see that as much of a positive driver. While in Auckland some retail shops will be allowed to open from Wednesday, hairdressers, nail salons, and most hospitality venues will still likely be unable to trade for another few weeks until the new traffic light system takes effect. These restrictions remain some of the harshest in the world, with China a notable exception, and NZ is about six months behind the world in terms of dealing with learning to live with COVID19. How business and consumer sentiment respond to endemic COVID remains a big cloud of uncertainty overhanging the local economy.

The AUD is up 0.3% to 0.7420 with a 5% gain in steam coal and uptick in oil prices ( 0.75%/0.90%) additional supporting factors. After the post RBA decline, the AUD appears to be finding a base above 74c. Risk sentiment and commodities remain the biggest driver for the pair at the moment with rates markets dynamics mostly a source for volatility.

GBP also had a good night, up 0.41% to 1.3560%, notwithstanding a backdrop of record low real yields (see above), and media reports of the EU-UK Brexit deal potentially blowing up in the face of the UK if it activates article 16 of the Northern Ireland protocol to suspend parts of post-Brexit arrangements for the Irish border.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Read our NAB Markets Research disclaimer

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.