Robust growth for online retail sales observed in June

Insight

Higher US yields and 'risk-off' tone see AUD's hard-fought gains undone

Good morning

Middle East developments, that include US President Biden visiting Israel and publicly backing its claim Hamas was responsible for the Gaza hospital atrocity, and Iran calling for a ‘full and immediate boycott’ of Israel by Muslim countries, have contributed to higher oil prices overnight and, at least partly because of that, higher US bonds yields (and a steeper curve). This in turn sees risk markets under fresh pressure, the USD higher and the AUD give back most of this week’s hard-fought gains. A better than feared 20-year US bond auction has seen some of the earlier market moves retraced, but only very partially so. Its Australian labour market day, and tonight (early tomorrow morning our time) Fed chair Powell address the Economics Club in New York.

Overnight news beyond the Middle-East – and ahead of Powell tonight – includes three Fed speakers. NY Fed President John Williams sad, “We’re going to stick at it to make sure that we really achieve that goal of 2% on a sustained basis…We need to keep this restrictive stance of policy in place for some time.” Also of note, Williams said he is “not yet convinced” the neutral rate is higher. Fed Governor Waller (erstwhile hawk) said “I believe we can wait, watch and see how the economy evolves before making definitive moves on the path of the policy rate….I will be looking carefully at the data to see whether the real side of the economy begins to cool off or whether prices, the nominal side of the economy, heat up….As of today, it is too soon to tell.” And Fed Governor Bowman (also hawkish of late talking of the need for more than one further Fed hike) said that inflation has come down but is still too high, that strength in goods spending has been surprising and that the Fed is highly focused on returning inflation to 2%. No specific comments on the Fed’s next steps though.

We also heard from ECB Council member Robert Holzmann (considered one of the most hawkish GC members) who said in an interview the Israel-Hamas war risks stoking oil prices and in turn driving inflation and weighing on growth. “What has changed since our last board is the perception of risk: following the latest developments in the Middle East, the risk of higher oil prices and consequently higher inflation and lower growth has clearly increased,” Holzmann was cited as saying. He didn’t use it, but the ‘stagflation’ word appears to be coming back on to the lips of monetary policy makers, at least in Europe.

On the data front, the just released Fed’s Beige Book , published ahead of the end-month FOMC meeting, reported most districts indicated little to no change in economic activity since the September report. Consumer spending was mixed, especially among general retailers and auto dealers, due to differences in prices and product offerings. The near-term outlook for the economy was generally described as stable or having slightly weaker growth, while labor market tightness continued to ease across the nation. All up a bit, well, beige really. US September Housing Starts rose by 7%, close to the 7.8% expected but only partially reversing August’s 12.5% drop. Building permits fell by 5.7%, after rising 6.8% in August. UK inflation data came in a tenth above expectations on both headline and core CPI, at 6.7% and 6.1% expected, but were below the Bank of England’s August MPR forecasts (0.2% and 0.1% lower respectively).

China Q3 and September activity data mostly exceeded expectations, albeit there was a fair amount of scepticism that the data was quite as good as the headlines would have you believe (in particular that sequential quarterly real GDP growth had jumped from a (downward revised) 0.5% in Q2 to 1.3% in Q3 (i.e. 5.3% annualised). What is clear is that what improvements there was last quarter, and in September along, was consumption-led (annual Retail Sales growth jumped to 5.5% from 4.6%, above the 4.9% Bloomberg consensus, and was concentrated in goods more so than services. Fixed Asset Investment looks to have remained subdued (3.1% YTD in September down from 3.2% in August) while growth in industrial production looks to be holding up, unchanged at 4.5% y/y, a little above the 4.4% consensus and aided by some pick up in export demand).

Yesterday’s ‘fireside chat’ with RBA Governor Michele Bullock was illuminating, in particular her remarks that, “There’s a few things that are suggestive that it’s going to be difficult to get inflation down” and “services inflation – inflation in things like takeaways, hairdressers, restaurants, those sorts of things – that inflation is running at a bit over 4 per cent… So it’s above our target and it’s pretty sticky. And that’s what we’re observing overseas as well”.

And later on, there was some discussion of inflation expectations in the context of supply shocks (in response to a question on Israel/Gaza) in which Bullock highlighted that “the longer inflation stays above target and the more people observe it happening in their day-to-day lives, the harder it will be” ( to keep longer term expectations anchored near 2.5%, where she says they are now). The Governor’s comments add to the recent body of evidence that the RBA has turned somewhat more hawkish this month (pace Assistant Governor Kent’s remarks last week, and this week’s RBA Minutes). The signalling has not been lost on markets, which now assign a roughly 25% chance to a quarter point rate hike on 7 November and close to 50% by 2 December – still too low in NAB’s view – but where the next flash point for a further shift in expectations is next Wednesday’s Q3 CPI report.

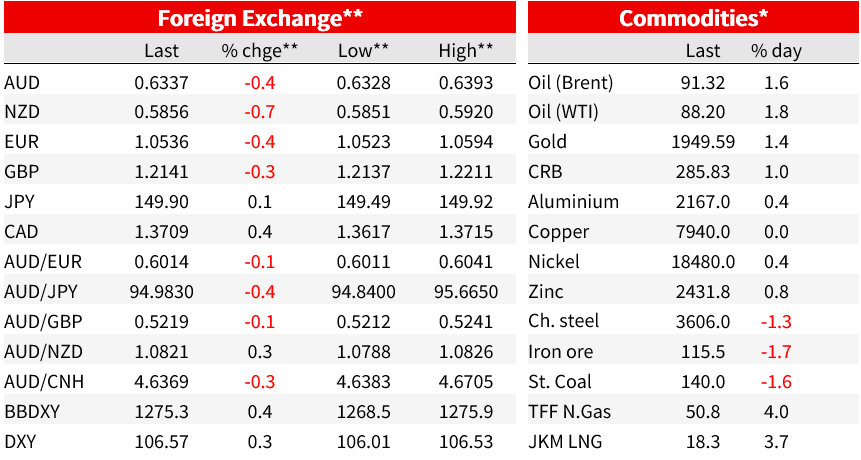

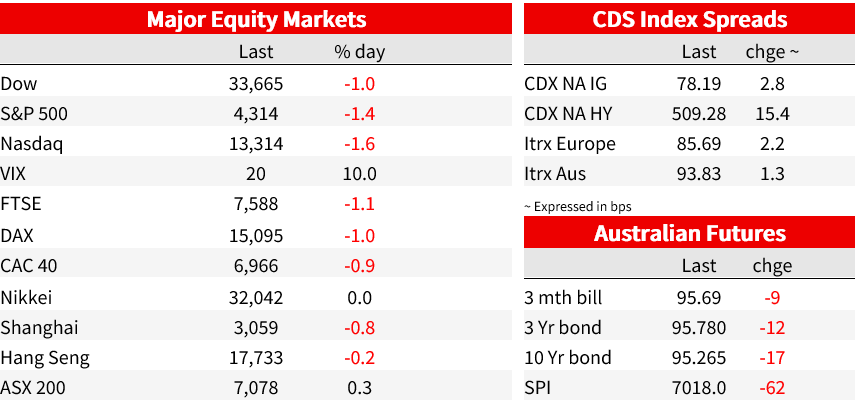

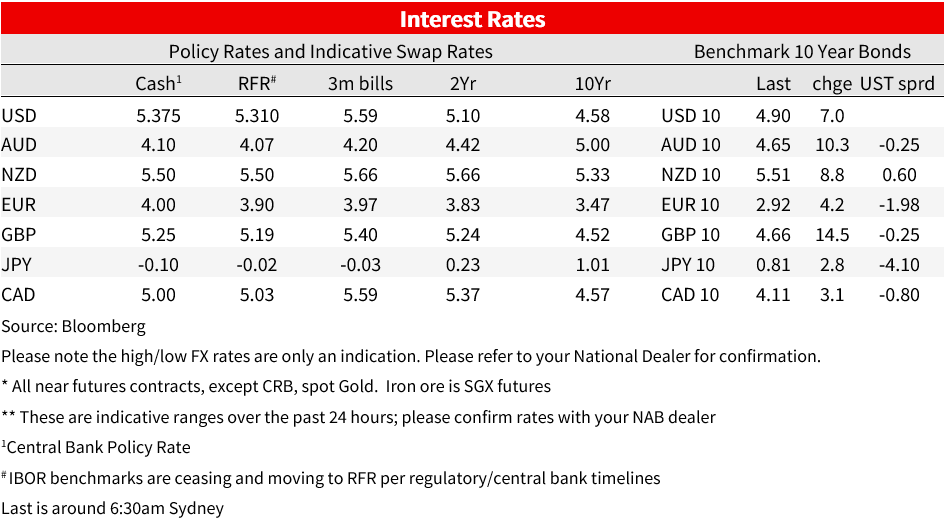

Market wise, the higher US yields/risk market sell off has been grist to the (stronger) USD mill, though notable in our view that latest gains have been very modest – certainly in relation to US 10-year yields exceeding their 6 October) highs (to 4.925%) and the VIX up 2 points to almost 20 in the last 24 hours. It does make us question just how much USD-positive news is now already in the price?

The $13bn 20-year Treasury bond auction went better than expected, clearing over 1bps below its when-issued (pre-auction) yield of 5.257%, at 5.245%. The 20-year yield subsequently fell back to around 5.20%, the catalysts for a small pull back in the USD (DXY -0.2% since the auction) and seeing US stock markets lift off their lows – but moves which have now largely been retraced with the DXY back sitting close to its intra-day highs and stocks making new lows.

AUD/USD has inevitable been a victim of the risk-off tone, giving back more than half of this week’s hard fought – RBA and China data related – gains from around 0.63 to almost 0.64 (0.6336 as I type). CHF and JPY are the best performing G0 currencies (both little changed in the last 24-hours) while AUD losses have been exceeded by CAD (despite higher oil prices) NZD, NOK an SEK.

Coming into the NYSE close and ahead of Netflix and Tesla’s results, the S&P was showing a loss of 1.5% (NASDAQ -1.6%) led by falls of more than 2% for Consumer Discretionaries, Industrials, Materials and Real Estate. Oil prices are currently up just shy of 2% (WTI +$1.66, Brent crude +$1.53).

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.