Robust growth for online retail sales observed in June

Insight

Fed Chair Powell’s remarks have seen a choppy market response and a steeper curve, but against a backdrop of weak risk sentiment

AU: Employment change (k), Sep: 7 vs. 20 exp.

AU: Unemployment rate (%), Sep: 3.6 vs. 3.7 exp.

US: Initial jobless claims (k), wk to 14 Oct: 198 vs. 210 exp.

US: Philly Fed business outlook, Oct: -9.0 vs. -7.0 exp.

US: Existing home sales (m/m%), Sep: -2.0 vs.-3.7 exp.

“If you think you can handle me, please handle me carefully” – Demi Lovato

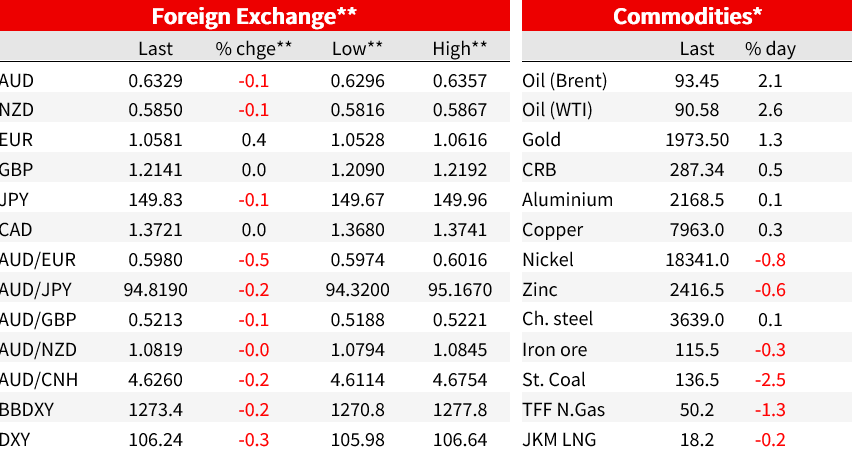

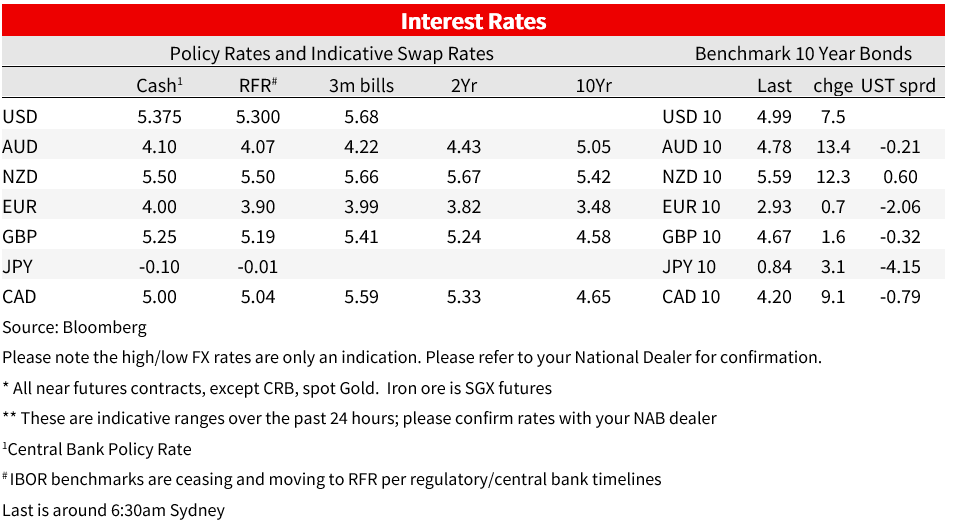

Fed Chair Powell’s remarks have seen a choppy market response, but against a backdrop of weak risk sentiment. The US 10-year rate traded at a fresh 16-year high of 4.99% and the curve is steeper, but the USD has been broadly weaker overnight, down 0.3% on the DXY. The euro is stronger, while commodity currencies have underperformed.

Fed Chair Powell spoke at the Economic Club of New York 3am our time. The key message was the FOMC is ‘proceeding carefully.’ His comments were supportive recent sentiments from his colleagues that the FOMC is likely to be on hold in November. Powell said policy was restrictive and there may still be tightening in the pipeline. Despite being ‘attentive’ to strong growth and labour market data, “Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy” (our emphasis). The WSJ’s Timiraos notes that, like in August, that’s a downgrade form the more muscular ‘would’ earlier in the year. Markets were already discounting slim prospect of a November hike though trimmed that even further, now pricing less than 1bp, while December pricing was trimmed from 34% to 25%.

In the Q&A, Powell said that the recent long-term bond sell off could lessen the need for further hikes at the margin if they persist. He also gave some succour to the higher for longer framing, saying the evidence is that policy is not too tight right now…either the neutral rate has risen, or rates have not been high enough for long enough. Powell noted the run-up in bond yields was mostly due to higher term premia.

The combination of near-term patience but, but attentiveness to data for how long rates will remain restrictive, has seen the yield curve twist steepen. Yields were little changed ahead of Powell’s remarks and were choppy during his speech and the Q&A with markets reacting to both dovish and hawkish soundbites. However, in the Q&A, Powell gave. This saw rates and the USD climb back higher. The 2yr yield fell about 6bp to 5.16%, briefly paring some of that move before settling back at 5.16%. The 10yr yield had touched new cycle high of 4.98% prior to Powell’s speech, and did the opposite of 2yrs as he spoke, initially up 9bp to 4.99%, nearing 5% for the first time since 2007, and after a brief pullback to 4.94% is back around 4.97%. The consequence is further de-inversion of the 2s10s curve, now at -19bp, compared to -111bp in early July, and the least inverted that measure has been in over a year.

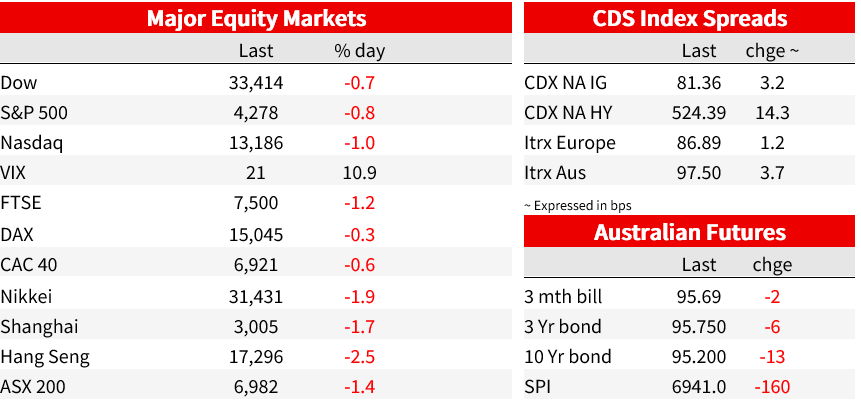

Equity markets also had a choppy session. The S&P500 ranged from down 0.6% to up 0.6% around Powell’s remarks, but slid after that to be down 0.85% on the day. Tesla sank over 9% on disappointing results, its worst day since July. In contrast, Netflix was 16% higher.

Ahead of Powell speaking, US economic data were mixed, but not particularly market moving, and geopolitical backdrop was weighing on risk sentiment. Initial jobless claims to fell to 198k, their lowest level since January, and stubbornly resisting the broader signs of some easing in US labour market tightness. Continuing claims rose to 1.73m, the highest level since July. That pattern is consistent with more difficulty finding employment and so longer spells out of work, but still low layoffs. Existing home sales fell 2% in September to a 13-year low.

Weaker risk sentiment yesterday initially drove a stronger USD, with the DXY spending time above 106.6, though that reversed with the DXY 0.3% lower over the day at 106.22. The AUD saw an intraday low of 0.6296 in our afternoon yesterday, but found support just below 0.63 and recovered alongside the broadly weaker USD to be little changed over the day at 0.6329.

Softer than expected employment data yesterday initially weighed on the AUD, but over the past 24 hours the move in the aussie has been in line with the NZD and the CAD, all about flat to the USD. European currencies have outperformed, with EUR recovering to 1.06 and AUD/EUR down to 0.5982.

As for the local employment data yesterday , while headline employment growth disappointed at +7k vs +20k expected and +35k needed to keep pace with population growth and leave the unemployment rate and participation rates stable, the unemployment rate fell 1 tenth to 3.6%. Employment growth month to month has been very volatile recently and the monthly number shouldn’t be taken too literally. In trend terms, employment growth is +23k, consistent with a slower pace of gains than earlier in the year. Despite the slower jobs growth in the month, the decline in the part rate means the unemployment rate fell, and at 3.6% is within the 3.4-3.7% range that had persisted for over a year. RBA governor Bullock this week said “ there are signs that that the labour market is turning, but the labour market is still very tight.” Nothing to change that assessment in yesterday’s data. The RBA forecast the unemployment rate averaging 3.9% in Q4.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.