Robust growth for online retail sales observed in June

Insight

Close but no cigar – US 10 year bonds traded to as high as 4.99% on Friday

Friday data and events Highlights:

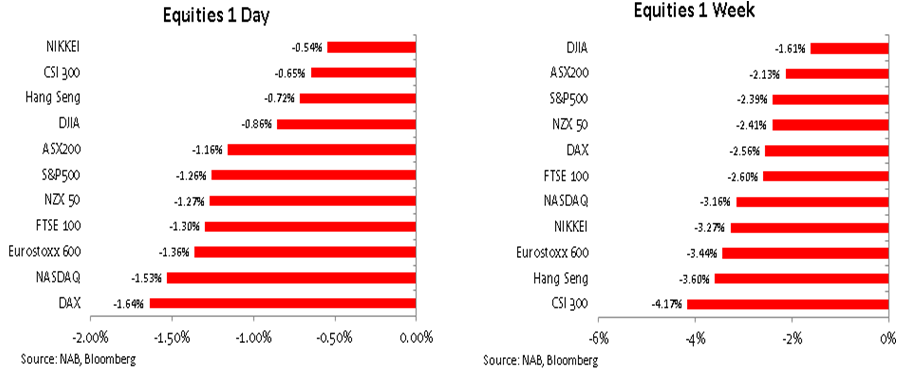

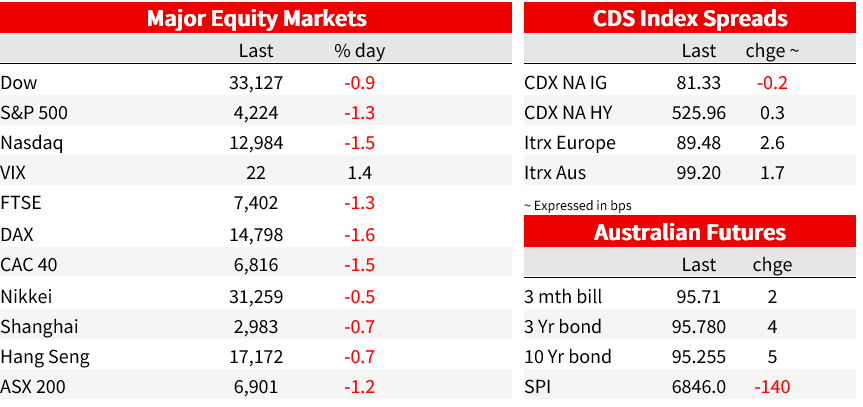

Asset market volatility continues through Friday, incorporating a fifth successive down-day for both the S&P500 and NASDAQ (taking losses for the week to 2.4% and 3.2% respectively) and the 10-year US Treasury yield posting a new cycle high of 4.99% early on in the New York day before peeling back to 4.91% by the close, finding some haven support amid the ongoing stock market weakness and perhaps too ahead of the weekend given still sky-high Middle East tensions. The VIX lifted by just a third of a point but at 21.71, closed at its highest since April 24.

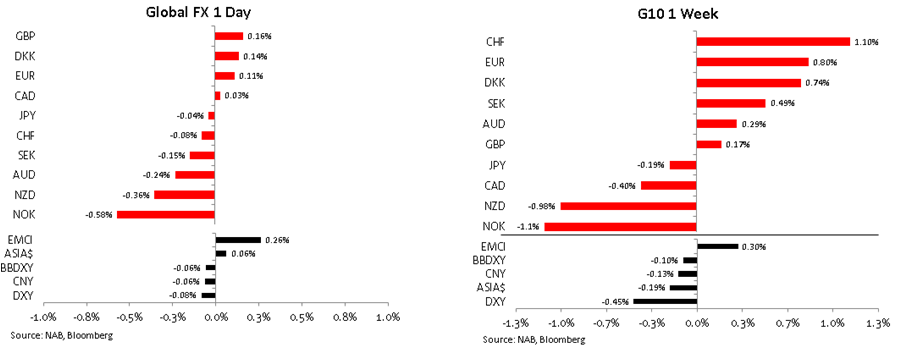

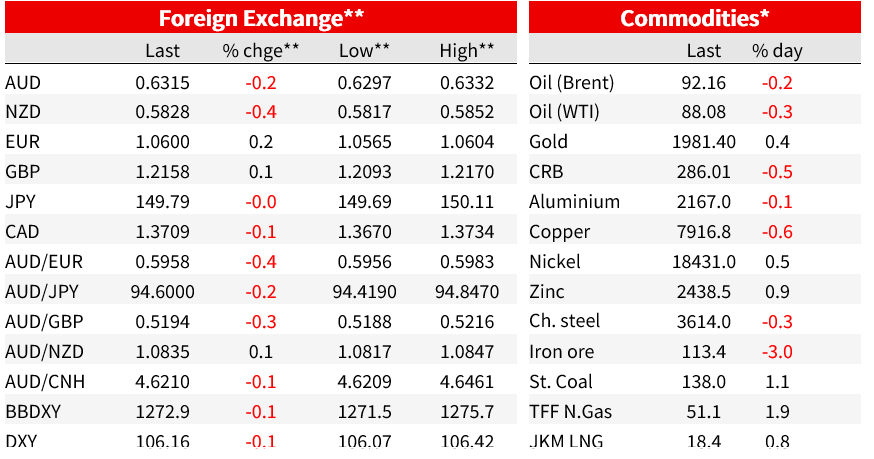

Currency volatility was much more subdued , the DXY tracing out only a 0.3% range to close less than 0.1% lower. AUD languished in the low 0.63s Friday to be little changed on the week. USD/JPY spent most Friday above ¥149.80 but fell one pip short of printing ¥150 for the first time since 3 October (when the BoJ is suspected of intervening) and before that exactly one year ago (21 October 2022). A weekend Nikkei report saying that the BoJ is raising the possibility of a tweak to its Yield Curve Control policy out of the October 31 BoJ meeting would, if it transpires, be a JPY positive development, yet in the meantime the early APAC market has seen fit to push USD/JPY above ¥150 (high of Y150.11 showing on Bloomberg) but we are just back below ¥150 as I type. .

Economic data was mostly second tier Friday (see above) one exception being UK Retail Sales, which fell a much larger than expected 1% (ex-auto fuel) for which the stats. office pinned the blame in part on unseasonally warm weather which delayed the onset of winter clothes purchases (-1.6%), though the likes of household goods purchases were also very weak (-2.6%) which was harder to pin on the weather.

Central bank speakers were thin on the ground Friday. Cleveland Fed president Loretta Mester (a 2023 non-voter) said that “From my forecast I would say we’re within one of the peak, then we can hold it there for a while,” she said in Q&A following a speech. “Regardless of the decision made at our next meeting, if the economy evolves as anticipated, in my view, we are likely near or at a holding point on the funds rate,” Mester said (remarks that were seen to be a little less unequivocal than of late regarding the need for at least one more hike). Earlier Friday, BoE Governor Andrew Bailey told the Belfast Telegraph that UK wages are growing too quickly to be compatible with the 2% inflation target.

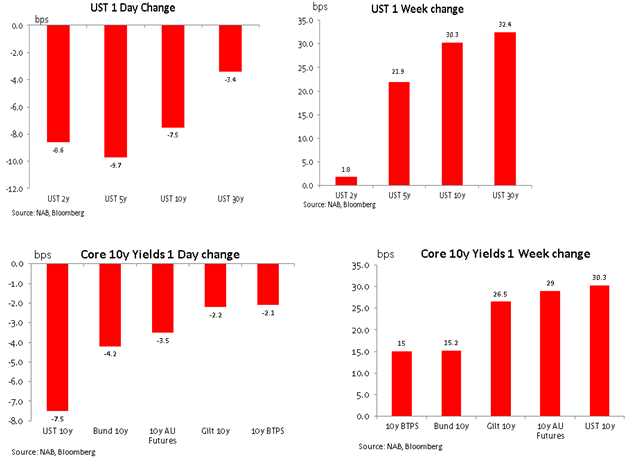

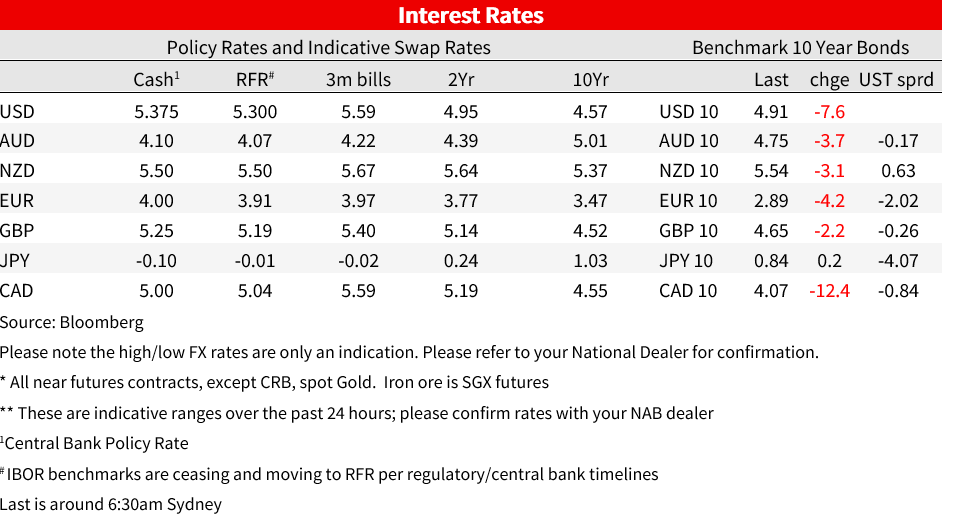

In bond land, a bit of a pull-back in Treasury yields on Friday (10s -3.5bps but which still left them up 30bps on the week and to the aforementioned high of 4.99%). 2s were up a mere 2bps – that’s some bear steepener. Bunds significantly lagged the rise in Treasuries, 10s up just 15bps, though UK Gilts and ACGBs pretty matched the US longer end moves. In Europe, S&P returned Greece to an investment grade (BBB-) rating Friday for the first time in over a decade (i.e. since the 2011 Greek Euro crisis) and reaffirmed Italy’s BBB investment grade status with a stable outlook, Yet with 10-year Greek debt already trading some 55-60bps though Italy at 10 years (4.35% vs 4.92%) the ratings news looks as though it was very much ‘in the price’ (plus Greece’s fiscal metrics have been moving in the right direction- hence the upgrade – unlike Italy’s).

apan’s 10 yr JGB yield traded as high as 0.845% on Friday, and early week price action will need to consider Sunday’s Nikkei report that the Bank of Japan has begun to discuss the possibility of another tweak to its Yield Curve Control settings, noting that long-term rates are rising in tandem with those in the US. Such a move (in what form the report doesn’t say) is seen being discussed at the next policy meeting (Oct 31) though the Nikkei notes some officials remain cautious, seeing a need to continue to monitor wage increases

The Nikkei report hasn’t stopped traders bidding USD/JPY through ¥150 at the start of the APAC trading day (high of¥150.11 showing on Bloomberg) though it has quickly recoiled, to now be just below. A rock steady USD/JPY exchange rate on Friday just below ¥150 contributed to a fairly low-volatility FX Friday more generally – certainly relative to other asset classes, with the DXY index tracing out a mere 0.3% range and finishing -0.1% down on Thursday’s close – and down 0.5% on the week. This is somewhat surprising in the context of risk-off sentiment where equities suffered a fifth consecutive down day (S&P500 -1.3% Friday and -2.4% on the week, NASDAQ -1.5% taking the weekly loss to 3.2%). The Swiss Franc looks to be the safe-haven currency of choice at present.

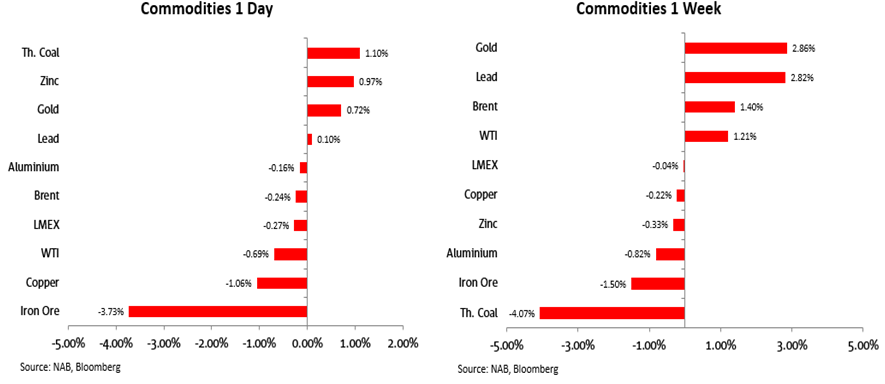

And while AUD continues to be seen as the preferred G10 FX whipping boy whenever risk is ‘off’, AUD/USD managed a small ‘up’ week (+0.3%) albeit it was off 0.25% on Friday alone. The weekly performance wa also creditable in the context of iron ore having a very bad day Friday (-3.7%, to be -1.5% on the week) and thermal coal losing 4% in the week.

Elsewhere in commodities , gold continues to find safe haven support outweighing the impact of rising real yields, up 0.7% Friday and 2.9% on the wek. Oil was a touch softer Friday (Brent -0.24%, WTI -0.7%) but on the week both are higher (1.4% and 1.2% respectively).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.