Robust growth for online retail sales observed in June

Insight

US equities are lower led by the tech heavy NASDAQ index and not helped by a new surge in UST yields. The USD extended yesterday’s gains with the AUD at the bottom of the G10 board, reversing its post CPI gains.

Events Round-Up

AU: CPI (y/y%), Q3: 5.4 vs. 5.3 exp.

AU: CPI trimmed mean (y/y%), Q3: 5.2 vs 5.0 exp.

AU: CPI trimmed mean (q/q%), Q3: 1.2 vs. 1.0 exp.

GE: IFO expectations, Oct: 84.7 vs. 83.5 exp.

CA: Bank of Canada policy rate (%), Oct: 5.0 vs. 5.0 exp.

US: New home sales (k), Sep: 759 vs. 680 exp.

Good Morning

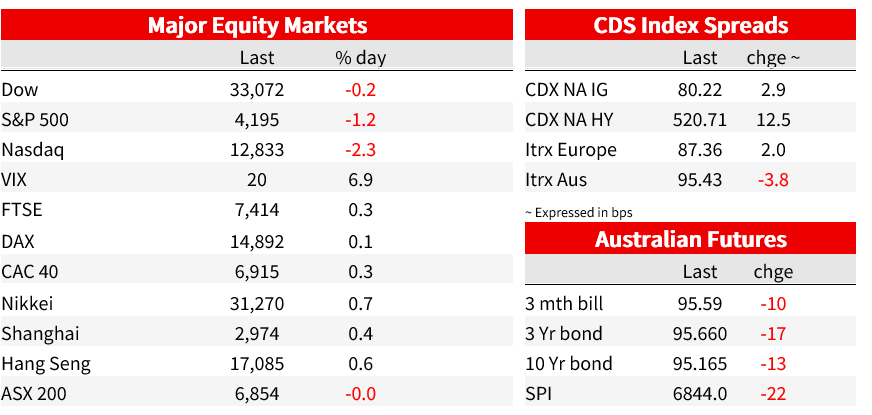

Markets are showing renewed signs of uneasiness with US corporate earnings results an additional source of volatility. US equities are lower led by the tech heavy NASDAQ index and not helped by a new surge in UST yields. The UST curve bear steepened with 10y UST up 13 bps over the past 24 hours. The USD extended yesterday’s gains with the AUD at the bottom of the G10 board, reversing its post CPI gains.

US equities are showing sharp losses on the day with big tech leading the decline . The NASDAQ is over 2% lower while the S&P 500 is down close 1.5%. Alphabet’s disappointing results have outweighed Microsoft better than expected numbers while underwhelming guidance from Texas instruments didn’t hep either, the Philadelphia Semiconductor Index is down over 4%. A decent move higher in UST yields (more below) was an additional headwind. Earlier in the session, ended little changed while initial gains by Asian equities, after China announced new debt issuance and a higher budget deficit, faded. The Hang Seng China Enterprises Index was up more than 3% intraday before closing 1% higher.

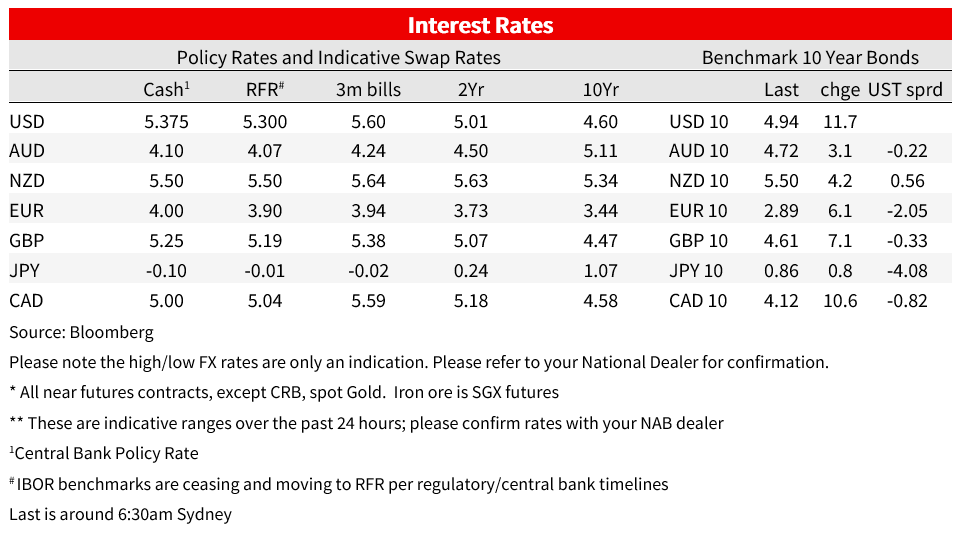

Core global yields are higher with US and German economic data releases supporting the move. US new home sales surprised with a 12.3% jump in September, the biggest monthly gain in over a year. Supply shortages alongside price discounts and mortgage rate buydowns by builders are supporting sales. Meanwhile in Germany, the IFO survey also delivered a positive surprise, the IFO expectations index climbed to 84.7 from 83.1 in September. This paints a slightly more optimistic picture than the advance PMIs, released earlier in the week, where the composite index fell further into contractionary territory.

The UST curve bear steepened with 10y UST yields up 13 bps over the past 24 hours to 4.95%. The move up in UST yields was also supported by supply concerns, amid expectations that increased auction sizes will be announced next week. Of note too, overnight the US$52bn 5-year note auction attracted weak demand with the bid/cover ratio the lowest since September last year. Earlier in the session core Sovereign European yields also ended the day higher. Ahead of the ECB meeting tonight (see more below), German real yields lead the underperformance with the money, paring 2024 ECB easing bets by 3bps to 71bps. The ECB is widely expected to hold tonight with the market leaning towards a higher for longer outlook. 10y Bunds closed +6bps to 2.88% while 10-year Gilts were +7bps to 4.605%.

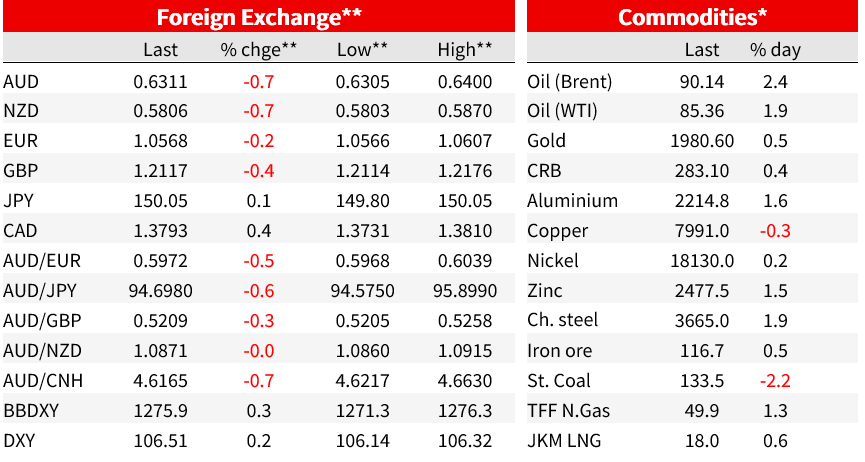

Risk aversion evident in equity markets plus a move up in core global yields, led by US Treasuries, have helped the USD extend its gains into a second consecutive day. The DXY and BBDXY indices are up 0.2% and 0.34% over the past 24 hours with the USD also up against all G10 pairs. Commodity linked currencies are the notable underperformers with the AUD at the bottom of the G10 board, down 0.77% to 0.6310, effectively reversing all of its post CPI gains seen during our day session yesterday. Yesterday, Australia’s Q3 trimmed mean CPI printed at 1.2% q/q, materially above the RBA’s August SoMP forecast. Notably too, details suggest domestically sensitive components are the main driver of inflationary pressure. NAB continues to expect a hike in November, and for the tightening bias to remain.

The NZD could not escape the USD surge, the pair is down 0.7% to 0.5804 while the CAD is -0.48% lower. Overnight the BoC lefts its policy rate unchanged, as expected, at 5%. The Bank retained its tightening bias with Governor Macklem noting in a statement that “Council is concerned that progress towards price stability is slow and inflationary risks have increased, and is prepared to raise the policy rate further if needed.”.

In other news, Israel has agreed to delay its ground attack in Gaza in order for the US to assemble air defenses to protect its troops in the Middle East (thereby suggesting both possible time for more aid to get in and presumably more negotiations, but also a sense of an invasion is coming). Netanyahu says, “we are preparing for a ground operation,” the timing of which will be reached by consensus. Adds, “we are in a battle for our existence”

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.