Coming in for landing in a heavy cross wind

Insight

Risk sentiment started the week on firmer footing. Equities are higher, the US dollar is lower, and US yields were higher. Brent oil lost 3%, back below $88 a barrel.

Events round-up AU: Retail sales (m/m%), Sep: 0.9 vs 0.3 exp. GE: GDP (q/q%), Q3: -0.1 vs. -0.2 exp. EA: Economic confidence, Oct: 93.3 vs.93.0 exp. GE: CPI EU harmonised (m/m%), Oct: -0.2 vs. 0.1 exp. GE: CPI EU harmonised (y/y%), Oct: 3.0 vs. 3.3 exp.

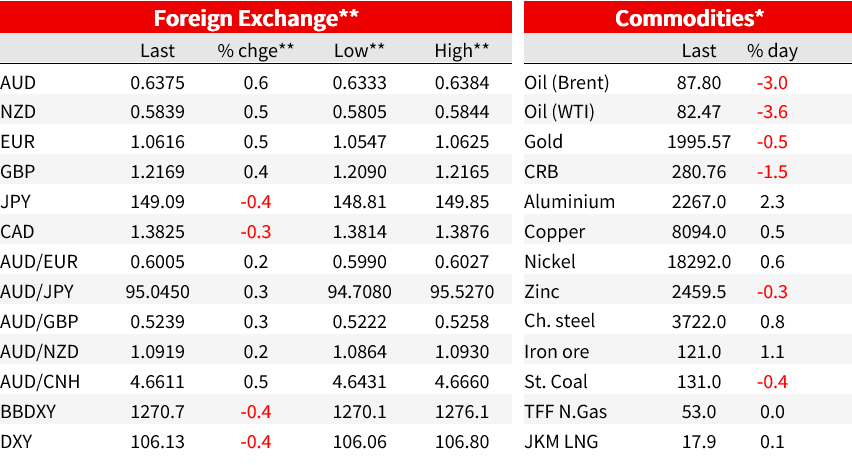

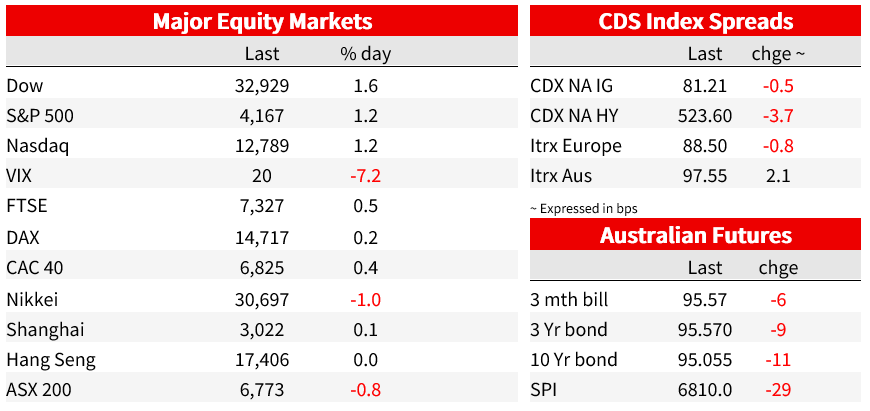

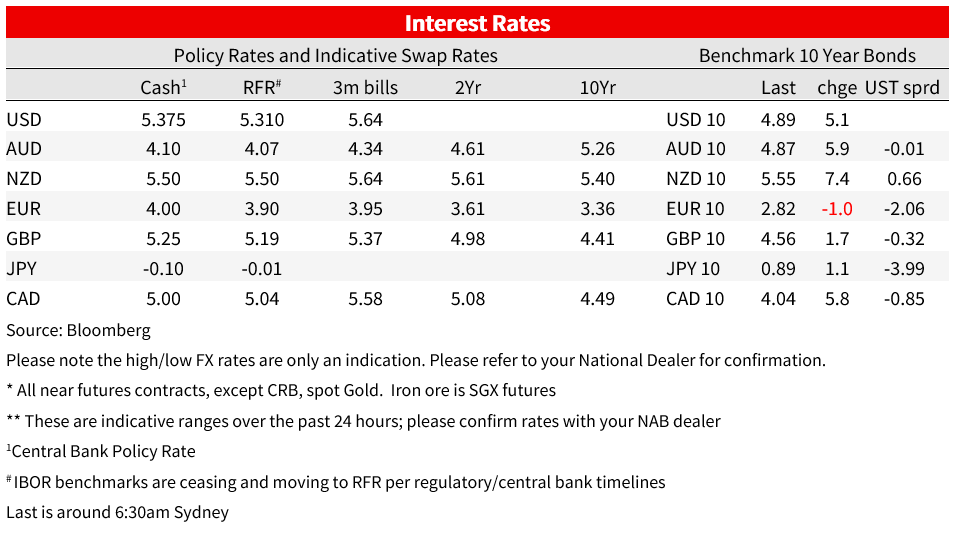

Risk sentiment started the week on firmer footing. Equities are higher, the US dollar is lower, and US yields were higher. Brent oil lost 3%, back below $88 a barrel. The price action is consistent with a more sanguine view of the prospects for greater broadening of the Israel-Gaza conflict. The S&P500 gained 1.2%. that was a broad-based gain, with all sectors higher on the day, led by Communication Services and Financials., but A Nikkei report that the BoJ would consider letting the 10yr yields rise above 1% helped the yen. The WSJ reports that Israeli tanks and infantry have pushed into the outskirts of Gaza city in a major advance aimed at encircling the enclave’s biggest population centre. But the market response suggests developments over the past couple of days may have been more gradualist than feared. Brent oil was down 3% to below $88, 3.8% above its 6 October level and 9% below its late September peak. WTI slipped below $83. The World Bank in its quarterly Commodity Market Outlook concluded that the effects of the conflict “should be limited should be limited if the conflict doesn’t widen” and “the global economy is in a much better position than it was in the 1970s to cope with a major oil-price shock.” The World Bank’s baseline is for a decline in oil prices to average $81 next year. A ‘small disruption’ loosely equivalent to Libya in 2011 would see supply down 0.5-2mn bpd and prices 3-13% higher, ranging to a ‘large disruption’ comparable to the Arab oil embargo, that would see supply 6-8m bpd lower and prices around $150. A Nikkei report that BoJ officials would discuss a further tweak of its yield curve control policy saw a jump higher in the yen. The yen had been trading lower ahead of the report, but jumped around 0.5%, taking the USDJPY to 148.81, its lowest intraday level since October 11. The JPY has largely held on to those gains, up 0.4% against the broadly weaker dollar on the day. The USD was 0.4% lower on the DXY, while the euro gained 0.5% to 1.0615 . The AUD was again the outperformer, gaining 0.6% against the dollar, helped by the positive risk tone. Stronger retail sales data (see below) reinforcing expectations the RBA is unlikely to be done helped the cause. The AUD reached an intraday high of 0.6384, currently not far off that at 0.6376. It was also a full day for European country-level data, ahead of euro area GDP and preliminary CPI prints today. German GDP fell 0.1% in Q3, slightly better than consensus for -0.2% q/q, and there were upward revisions to prior data. The prevailing view that the economy is struggling to perform remains intact, but a contraction of 0.3% y/y on a workday adjusted basis, compared to expectations for -0.7%, was enough to see some support for the euro. Country level data so far doesn’t obviously skew the risks to the 0.0% q/q consensus for euro area GDP tonight. The flip side of sluggish European activity is moderating inflation, and German and Spanish preliminary October CPIs overnight came in below expectations. German harmonised inflation slowed to 3.0% from 4.3% and 3.3% expected, while Spanish rose to 3.5% from 3.3%, but undershot expectations for 3.8%. Core inflation (on a non-harmonised basis) also slowed in both countries, but remained above headline measures, with base effects from moderating energy prices a key source of downward pressure on headline inflation in much of Europe. The data suggest downside risk on Euro area CPI figures due tonight. Softer inflation fed expectations of an ECB at the end of its tightening cycle, and European bonds outperformed. German 10yr yields were 1bp lower at 2.82%. US yields, in contrast, were higher. 10yr yields were up 5bp to 4.88%, while the 2yr gained 3bp to 5.04%. There were some jitters, with an initial small rally in bonds around the release of the Treasury’s estimates for quarterly borrowing at 6am our time, but little lasting reaction. The US Treasury reduced its estimate for federal borrowing for the current quarter to $776bn from $852bn after upgrading its projection for revenues , a contrast to recent widening in the fiscal deficit. The Treasury’s updated issuance plans are set for release Wednesday. Locally yesterday, September retail sales rose 0.9% m/m, well above consensus for 0.3%. There were also small upward revisions to prior months. The ABS cited a range of factors as supporting the outcome, and while we don’t expect retail growth of 0.9% m/m to persist, on a trend basis retail sales is suggestive of resilience in the Australian consumer even as very elevated population growth is a key tailwind to aggregate consumer spending growth. Volumes estimates are published Friday, and we expect to see a small positive for quarterly retail volumes growth after three consecutive quarters of declines in this good-heavy consumption indicator. The RBA said in October that activity was “more resilient than expected ” in the first half of 2023, and yesterday’s data suggests greater resilience than the RBA’s August framing has continued in the second half. Market pricing sits at 63% for November, with 43bp priced by mid next year. Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.