Robust growth for online retail sales observed in June

Insight

Japanese Yen slumps after only minor BoJ policy tweaks

In recent weeks it has become almost trite to talk about US exceptionalism, yet it has been on display once more in the last 24 hours, thanks more to weaker than expected data out of the Eurozone and China that another dose of significant upside US economic surprises. The USD is stronger across the board, led by sharp losses for the JPY – USD/JPY to a high of ¥151.71 – after the BoJ failed to back up an eye-popping upward revision to its FY2024 CPI forecasts with anything more than tinkering with its Yield Curve Control policy (albeit in line with pre policy meeting ‘leaks’). Risk sentiment has been a little better in the US and most of Europe, though front-end US rates were higher, pricing not helped by an upside surprise to the US Q3 Employment Cost Index. There is plenty of US data to look forward to tonight, ahead of the FOMC meeting outcome at 5:00AEDT tomorrow morning.

First to the Bank of Japan , where as expected, it left its policy rate unchanged (balance rate at -0.1%), but, as pre-empted by an earlier Nikkei report, introduced flexibility to its YCC program. The BoJ now sees the 1% cap on 10y JGBs as a reference rather an enforceable ceiling with the implication it is willing to allow 10y JGBs yields to trade above 1%. Importantly in this regard, the BoJ decided to relinquish its daily fixed-rate bond-buying operations; this has been its main tool for limiting a rise in JGB yields. In making the decision the Bank cited the “large side effects” it might entail.

Whether the Bank has abandoned YCC in practical terms it remains to be seen. A line in the Statement noted “It is appropriate for the Bank to increase the flexibility in the conduct of yield-curve control, so that long-term interest rates will be formed smoothly in financial markets in response to future developments.”. But at the press conference,Governor Ueda vowed to continue with large-scale bond buying as part of YCC adding that he didn’t see yields staying above 1% ‘f or a long time’.

Accompanying the decision, BoJ made substantial upward revisions to its inflation outlook with Core CPI now seen a 2.8%yoy in FY23, up 0.3% relative to its July forecasts. More dramatically, it upped its FY2024 core CPI forecast to 2.8%, compared to 1.9% previously, confirming the Bank now sees inflation above target for three successive years. Yet in limiting its revision to the FY25 forecast to 1.7% (up just 0.1%) it justifies the contention, made by Governor Ueda in his post meeting press conference that cost push inflation is behind the upward price revision and that he ‘cant’ see the inflation target in sight with certainly’. Ueda made clear BoJ still need so carefully monitor to see whether a wage-price cycle takes hold – from which we would infer it doesn’t now expect to form judgement on this before net Springs annual wage round.

USD/JPY didn’t really start moving until after Mr. Ueda spoke, when it moved clear above ¥150 and then ground steadily higher through the European and US sessions to a high of ¥150.71 (just shy of the ¥151.95 high on 21 October 2022 that preceded the BoJ’s FX intervention). On the latter, data released overnight indicated that the BoJ did not intervene in early October, contrary to our and many observers’ belief at the time.

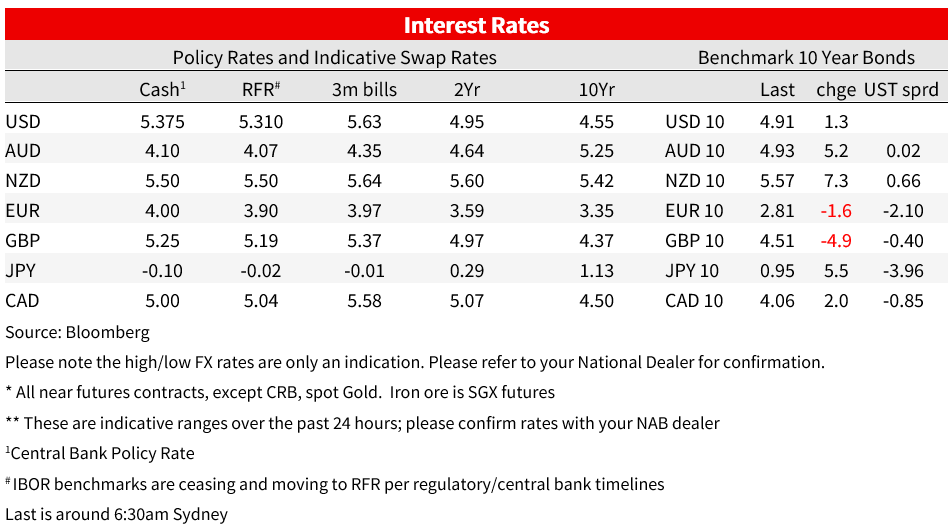

On the data front overnight, the most keenly anticipated release was the US Q3 Employment Cost Index (ECI). At 1.1% q/q , this was mildly disappointing after the 1.0% Q2 gain and the 1.0% expected for Q3. The detail showed a pick-up in wages and salaries to 1.2% from 1.0%, though annual ECI still dipped, to 4.3% from 4.5%. The message, that wages growth (or more accurately unit wage costs) aren’t yet fully consist with the Fed’s 2% inflation target was not lost on the front mnd of the US bond market, where 2-year Treasury yields jumped from 5.01% pre-release to as high as 5.08%.

Also out in the US, the Conference Board’s October consumer confidence reading came in above expectations at 102.6, down from an (upward revised) 104.3 but above the 100.6 consensus. And ahead of tonight’s US ISM Manufacturing index, the (Boeing-intensive) Chicago PMI slipped to 44.0 from 44.1, just below the 45.0 consensus. Canada printed August monthly GDP at 0.0%, versus 0.1% expected.

In Europe, more data disappointment came in the form of Q3 Eurozone GDP, printing -0.1% against a flat expected outcome (though hardly a surprise after the earlier reported German GDP). This nevertheless raises the spectre of a technical recession if Q4 is negative (and if Q3 is not subsequently revised higher). On the positive side, Eurozone October CPI was up just 0.1% against 0.3% expected (year-on-year down to a two-year low of 2.9%) with core CPI down to 4.3% from 4.5%. The data plays to the ECB being done at the current 4% Deposit R ate and 4.50% Refinancing Rate.

In FX , adding earlier weight to the AUD on top of broader USD-positive impact of the BoJ, yesterday’s China PMI data was a significant disappointment, coming as it did after the signs of growth acceleration evident in the mid-October GDP, Retail Sales and Industrial Production data. Manufacturing fell back to below 50 (49.5 from 50.2 and 50.2 expected) and non-manufacturing to 50.7 from 51.7 (532.0 expected). Let’s see if the Caixin version (manufacturing later this morning) says similar. AUD/USD slipped from above 0.6370 to around 0.63540 post the China data and has subsequently dropped to as low as 0.6315 in the context of post-US ECI USD gains. Note that USD/CNH has, in conjunction with the higher USD/JPY, risen from around 7.325 to 7.345 overnight. This has some (negative) implications for AUD/USD unless we see a strong protest from the PBoC this morning. The DXY USD index is up 0.5%, principally from the 0.3% contribution from EUR/USD, 1.6% from USD/JPY and 0.8% from USD/CHF.

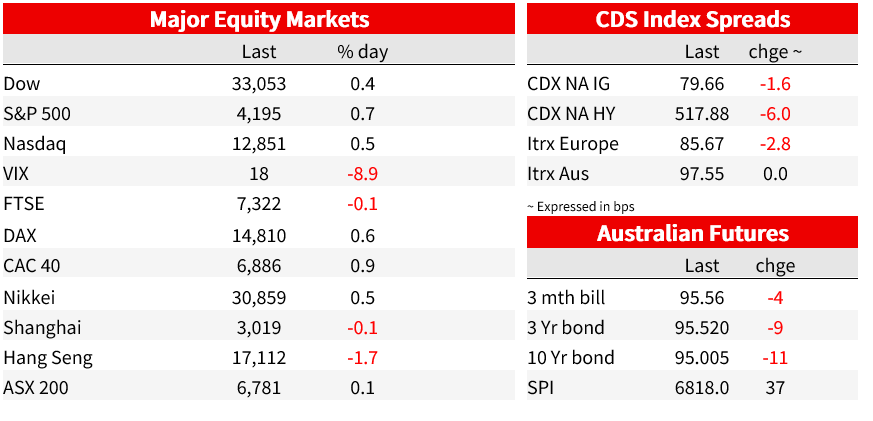

US bond yields were some 6bps higher at the front end post the US ECI report, but on net are little changed on the day, while an earlier 2bps decline in 10-year yields has turned into a rise of around 0.5bps. So overall a pretty flat night, after European bonds mostly finished lower in yield, albeit not by much. Australian bond futures show implied yields up about 3bps from Tuesday’s local close at both 3 and 10 years.

US equities are coming into the close showing gains of around 0.5% for both the S&P500 and NASDAQ. All S&P sub-sectors are in the green, gain led by Real Estate (2%) and Financials (1.1%). Oil is down just over $1 for both WTI and Bren blends, while gold is off $11 at $1,984.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.