Long-term signal vs. Short-term noise

Insight

Positive Omicron reports coming from South Africa alongside an encouraging preliminary assessment from Dr Fauci over the weekend boosted sentiment with overnight news of policy easing in China, an additional bonus.

https://soundcloud.com/user-291029717/china-and-omicron-hopes-drive-a-bounce-back?in=user-291029717/sets/the-morning-call

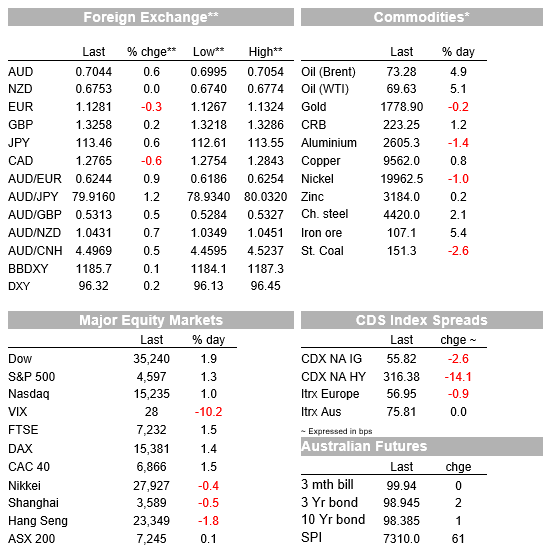

After a volatile week, European and US equities have started the new week with a positive tone, recovering some of last week’s losses. Positive Omicron reports coming from South Africa alongside an encouraging preliminary assessment from Dr Fauci over the weekend boosted sentiment with overnight news of policy easing in China, an additional bonus. The UST curve has bear steepened with the USD little changed, its underperformance against commodity linked currencies (ex NZD), offset by gains against safe haven pairs.

In a sign of reopening optimism, the Dow index is leading the rebound in US equities, up just under 2% in the last hour of trading. The S&P 500 is up over 1.2% with Energy, Industrials and Material stocks leading the charge. The NASDAQ is not too far behind, up 1.05% as I type. Looking at the intraday charts it has been a steady rise for equities over the course of the overnight session, but markets remain volatile, the VIX index has come down from its Friday high of 35.32, but at 27 it is still reflecting an environment of choppy conditions. The Euro Stoxx 600 index closed up 1.3%, recovering much of the loss seen over the prior two sessions.

Although there is still a lot of uncertainty over Omicron‘s health and economic impact, investors have embraced news from South Africa suggesting the exponential rise in Omicron infections has not been followed by a big wave in hospitalisations . Comments on Sunday from Dr Fauci, US President Joe Biden’s chief medical adviser, noting initial data from South Africa are “a bit encouraging regarding the severity,” certainly helped the mood at the start of the new week.

On this score, immunologist reports coming from South Africa suggest there are early indications that the new Omicron variant is likely to evade the protections of current vaccines to at least some extent, but it is unlikely to cause more severe illness than previous variants. This is because the T-cell response is still active against Omicron, even if the mutations on the spike protein reduce the chance of antibodies to bind. Adding a more cautious take there have also been reports noting high levels of reinfection with some of these new infections leading to serious illness. Importantly too, data coming from the Tshwane metro area, one of the largest hospital systems in Gauteng is showing a material increase in hospitalisations under the age of 20 and 5 years. So, there is a lot we don’t know yet and while sentiment has improved, the still elevated VIX level is a reminder that price action is likely to remain choppy until we know more.

Another bonus to the improvement in risk sentiment overnight was news of policy easing coming from China. After the signals provided by Premier Li Keqiang last week, the PBoC People’s Bank of China will reduce the reserve requirement ratio (RRR) by 0.5 percentage point for most banks on Dec. 15, releasing 1.2 trillion yuan ($188 billion) of liquidity. The RRR cut will be applied to all banks except those that are already on the lowest level of 5%, which are mostly small rural banks. The move eases concerns over the close to ¥1 trn worth of the one-year loans maturing on the same day of the cut takes effect. The RRR cut will help banks repay the loans and help replenish institutions’ long-term capital.

However, perhaps more important than the RRR announcement, the PBOC decision was closely followed by a statement from the communist party central committee vowing to stabilize the economy in 2022, signalling an easing of some property curbs. A Central Economic Work Conference has been announced for some time this month with the objective of determining an economic policy plans for the next year.

Meanwhile, more detail has been leaked on Evergrande’s imminent debt restructuring, which would be the largest on record, expected to include all public bonds (including offshore) and its private debt obligations. According to Bloomberg, Evergrande has some $19.2 billion in outstanding offshore public bonds and $8.4 billion in local notes.

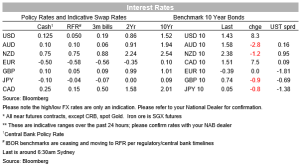

Looking at the rates markets, the improvement in risk sentiment has resulted in a bear steepening of the UST curve with the 10y Note, up around 8.5bps to 1.43% while the 2y rate is up 4.4 to 0.634%. Moves in core European yields were more subdued with 10y Bunds little changed at -0.388% while 10y Gilts closed 1bps lower at 0.738%.

Softer than expected German factory orders probably played a part in the inability for Bund yields to rise with orders slumping by 6.9% m/m in October, driven by an almost 11% fall in investment goods from outside the euro area, while domestic orders rose 3.4%. Meanwhile comments from BoE Broadbent played a hand in the move lower in Gilts ( 2 y down 1.5bps to 0.44%). Speaking in Leeds, BoE Broadbent said that “I go into these meetings not knowing very often what I’m going to vote myself”. The Deputy Governor still believes that interest rates will rise, highlighting Nov forecasts of above target inflation in 2-3 years without higher rates, but is not sure sure how Omicron will impact his decision on interest rates. After being more than fully price mid October, the market has continued to reduce the chance of a BoE rate hike in December, now around 0.25% priced.

The USD is little changed in index terms with the DXY index now trading at 96.32. Safe Haven pairs, JPY and CHF, have lost ground reflecting the improvement in risk sentiment in equity markets. USD/JPY now trades at ¥113.47 while CHF is the big underperformer, down 0.94% to 0.9259.

On the other hand, commodity linked currencies have had a positive start to the week . China policy easing news have helped copper (+1.94%) and iron ore (2.5%) perform while after last week’ s tumble (in fact six weekly consecutive falls), oil prices have opened the new week higher, currently up over 3%, with Brent crude now trading at USD73.30. Oil prices rose after Saudi Arabia boosted crude prices, signalling confidence in the demand outlook. This has been a nice backdrop for the AUD to perform, up 0.57% to 0.7041 with NOK (0.83%) and CAD (0.55%) also joining the party.

NZD was the notable laggard, unchanged at 0.6745. RBNZ Deputy Governor Bascand gave an interview to the FT where he said that if house prices cooled down faster than expected it could affect the RBNZ’s forecast for rapid interest rate rises next year. In last month’s MPS, the Bank projected 5.6% house price inflation next year but a number of anecdotes already suggest that the housing market has hit the wall, following the 180bps lift in key mortgage rates, the tighter macro prudential setting, tighter bank lending conditions and the government’s investor tax changes.

In the last hour US government officials have announced a diplomatic boycott the Beijing Winter Olympics in February due to concerns about “crimes against humanity” and other human rights abuses. Bloomberg notes the boycott means that athletes are free to compete even as administration officials stay home. The US decision stops short of the full-scale measures seen during the Cold War and at other points in Olympic history.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Long-term signal vs. Short-term noise

Insight

Join us as we discuss interest rates, general economic conditions, and the NAB AUD/USD forecast

Webinar

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.