Coming in for landing in a heavy cross wind

Insight

Risk assets had a solid end to the week with softer US economic data releases fuelling the notion that the Fed is done with the current tightening cycle. Front end yields led a rally in UST yields while the USD extended its decline to a third consecutive day.

Events Round-Up

AU: Retail Sales Ex Inflation (%), 3Q: 0.2 vs. -0.3 exp.

CH: Caixin China PMI Services, Oct: 50.4 vs 51 exp.

EC: Unemployment Rate (%), Sep: 6.5 vs. 6.4 exp.

CA: Unemployment Rate, (%) Oct: 5.7 vs. 5.6 exp.

US: Change in Nonfarm Payrolls (k), Oct: 150 vs. 180 exp.

US: Unemployment Rate (%), Oct: 3.9 vs 3.8 exp.

US: Average Hourly Earnings (m/m%), Oct: 0.2 vs. 0.3 exp.

US: Average Hourly Earnings (y/y%), Oct: 4.1 vs 4.0 exp.

US: ISM Services Index, Oct: 51.8 vs. 53.0 exp.

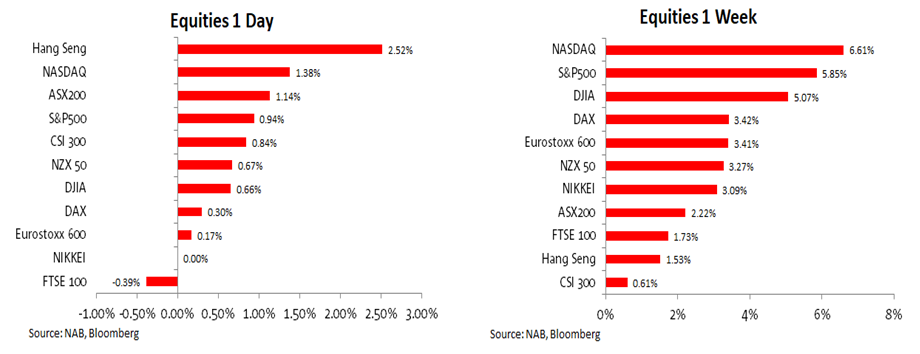

Risk assets had a solid end to the week with softer US economic data releases fuelling the notion that the Fed is done with current tightening cycle. The S&P 500 climbed close to 1% and the NASDAQ gained 1.38%, front end yields led a rally in UST yields while the USD extended its decline to a third consecutive day. US non-farm payrolls and US ISM printed softer than expected with the market trimming expectations for a January rate hike (25bps) to 10% while a full rate cut is now seen in Jun-24.

US non-farm payrolls increased by just 150k in October vs expectations for 180k print with downward revision to the prior two months (September down to 297k vs 336k originally). The 3-month moving average gain in overall payrolls slowed to 204k and private to 153k, so still a solid pace, but there are signs the labour market is cooling, amid improvement in labour supply (thanks to a rebound in immigration) and a tempering in the pace of hiring. The survey of households showed a more than 200,000 increase in those who lost their job or completed a temporary one. The unemployment rate increased to 3.9% in October from 3.8% in September, back in April it was 3.4% (history shows that if the unemployment rate rises half a percentage point, the economy tends to end up in a recession). Wages growth also eased during the month, average hourly earnings (AHE) rose 0.2%mom and 4.1%yoy, down from 4.3% in September. In the last three months, AHE rose just 3.2% annualized.

The October ISM services index fell to 51.8 from 53.6, below the consensus, 53.0. The biggest drop among the major subindexes was in business activity, down 4.7 points to 54.1, but this contrasts with the 3.7-point jump in new orders, partially reversing the September plunge. Adding to the notion of a cooling US labour market, the employment index fell 3.2 points to 50.2 while a decline in prices paid also favours a meaningful downshift in wage growth over the next few months.

Sticking with the data releases, Canada also had a labour market update on Friday with the data also revealing signs of a cooling market. Canada added 17.5k jobs in October, its weakest job gain in more than a year. Meanwhile the unemployment rose 0.2% points to 5.7%, the fourth monthly increase in the past six months. Wage growth for permanent employees slowed to 5%, missing expectations for a 5.2% gain, still this was the fourth straight month of pay raises of 5% or more. The data should keep the BoC on hold, but with wages growth still elevated, the Bank is likely to retain a tightening bias.

Finishing the trifactor of weaker than expected labour market data releases, the Euro area September labour report was also the weakest in a while . Unemployment rose 69k m/m, recording a second month of increase in 3, the unemployment rate rose one tenth to 6.5% vs expectations for an unchanged (6.45) outcome.

The softer than expected US data releases were the main driver for markets on Friday. A cooling labour market is encouraging the market to believe the Fed is done with its current tightening cycle. Near term Fed rate hike expectations have been trimmed (December now 4.8%, January 10%) while expectations for rate cuts next year have been brought forward, June 2024 now more than fully pricing a full 25bps rate cut (35bps compare to 21bps on Thursday).

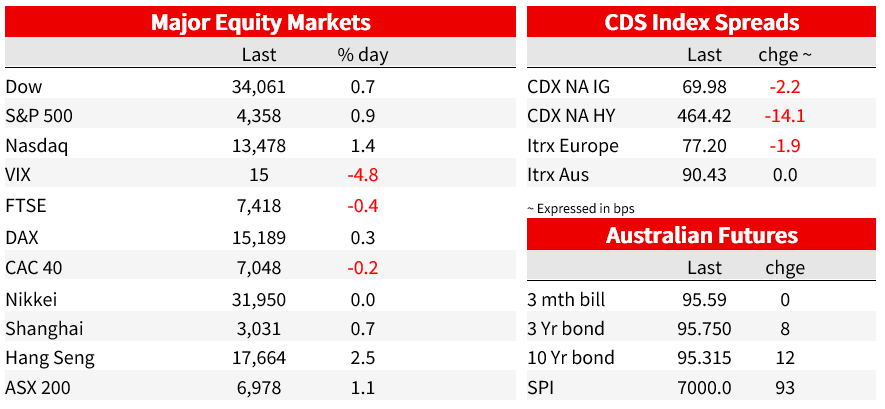

Risk assets had a positive Friday, thanks to the idea that bad economic news is good news(Fed done with its tightening cycle). The S&P 500 gained +0.94% and the NASDAQ was 1.38%. ON the week the S&P 500 climbed close to 6%, its best week year to date. The US reporting season is still underway and not all companies are reflecting the kind of optimism seen in the price action. Bloomberg notes that among companies that have issued guidance this earnings season for next quarter and beyond, more have been providing estimates that trail analysts’ expectations. A gauge of forward guidance that compares corporate forecasts with the Wall Street consensus has been lower only once since 2019.

The Eurostoxx 600 index managed a 0.17% gained on Friday, the Nikkei was flat and the UK FTS 100 was the underperformer, down -0.39%. All major indices managed to record gains for the week, although US gains were north of 5% while China’s CSI 300 printed a modest 0.61% gain for the past 5 trading days.

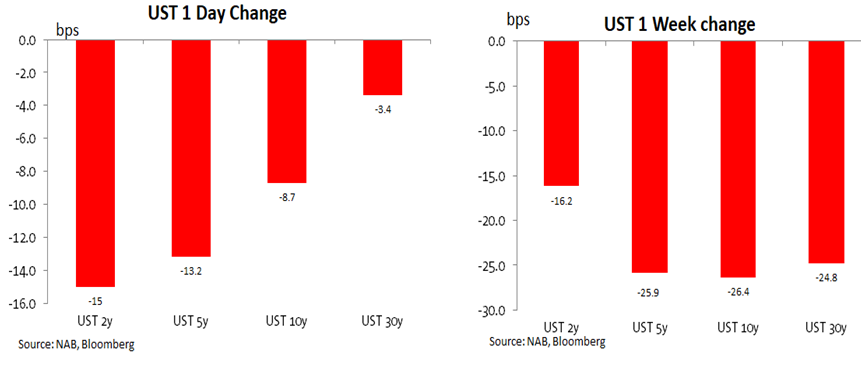

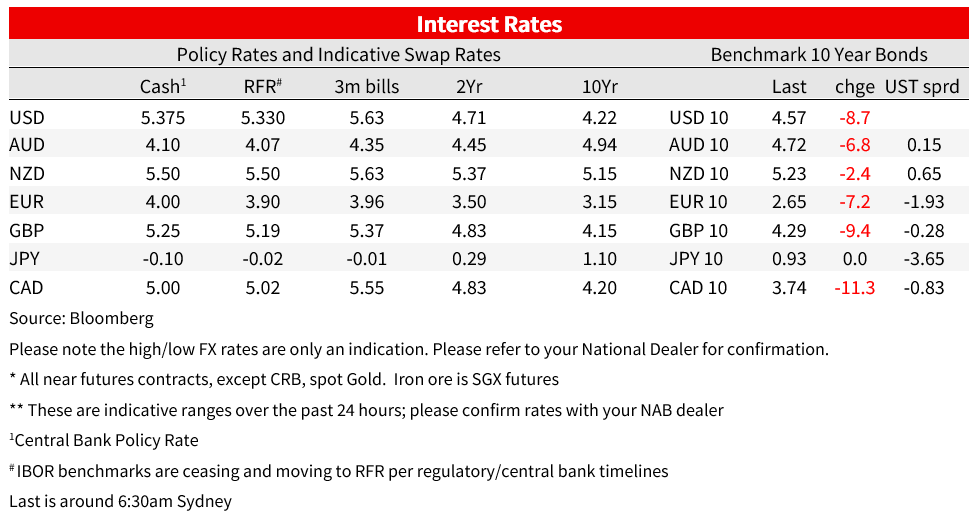

Front end bond yields led a bull steeping of the US Treasury curve with the two year tenor down 15bps to 4.841% while 10y UST fell 8bps to 4.57%, the benchmark yield traded down to an intraday low of 4.49% before recovering into the close.

Speaking after the US employment data, Richmond Fed President Barkin, an FOMC voter in 2024 noted that “What we saw today was data that showed a gradual lessening of the job market. I think that’s what those who would like to not see another rate hike would want to see. We’ll see what inflation comes in.”, but then reminded us that “We just got out of the last meeting! I don’t prejudge. What I would say is we want to be done with inflation.”. On the latter observation, is worth highlighting the Fed will get two more CPI reports before its next December 13 meeting.

European yields also traded lower on Friday, 10y Bunds fell 7bps to 2.645% while 10y UK Gilts eased 9.4bps to 4.288%. Australian bond futures closed the week at 95.315 (4.6850%), up 12 on the day.

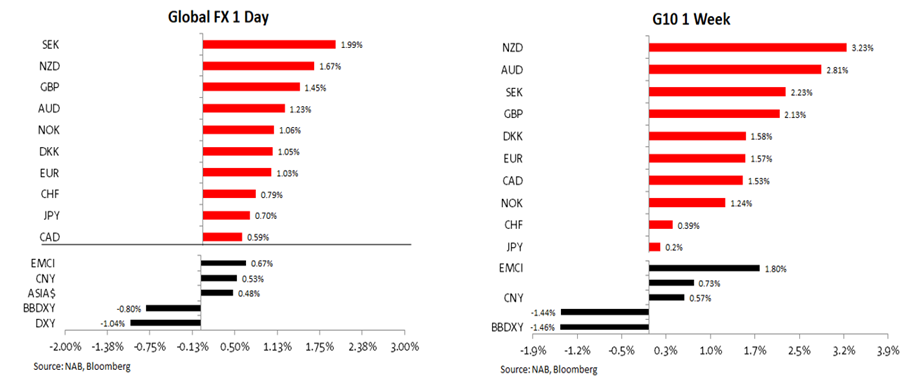

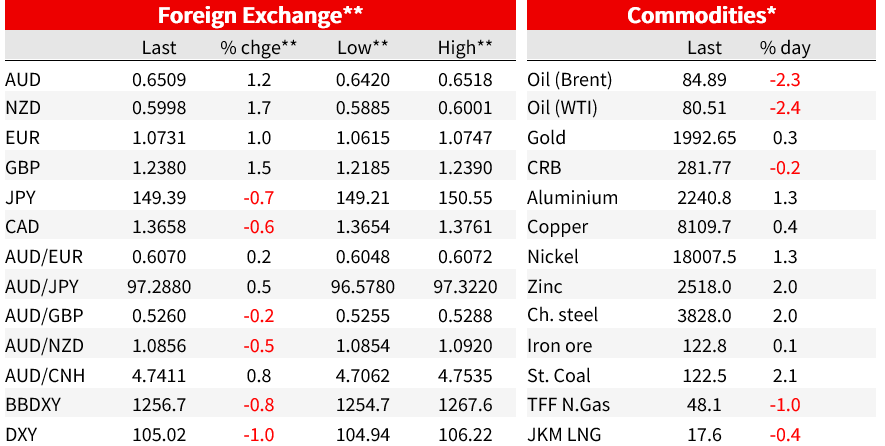

he USD was broadly weaker on Friday, extending its decline to a third consecutive day. The DXY and BBDXY indices fell 1.04% and 0.8% on Friday with both indices close to 1.5% lower on the week.

SEK led the gains on Friday, up 2% followed by GBP (1.45%), NZD (1.23%) and the AUD (1.06%). The AUD ended the week back above 0.65 and now start the new week at 0.6511. The NZD briefly traded above the 0.6 mark and now start the new week at 0.5994. The antipodean currencies were the notable performers on the week, NZD up 3.23% while the AUD was 2.81%.

The euro also performed against the USD, climbing to highs just below 1.0750, 2 big figures above the weekly lows. The union currency starts the new week at 1.0727, speaking to a Greek newspaper on Saturday, ECB president Lagarde said the ECB is determined to bring EU inflation down, adding that she was notr not worried about political backlash.

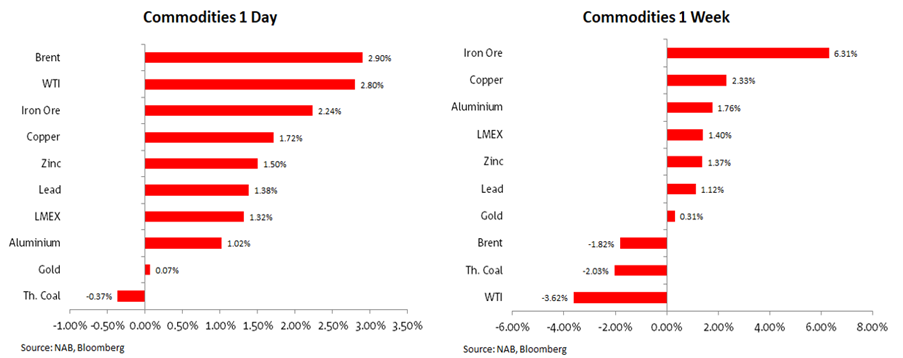

Oil prices fell over 2% on Friday with lead and Thermal coal up over 2%. Notably iron ore was again the outperformer on the week, up close to 5% over the past five trading days, showing little reaction to the softer China PMIs. Copper gained close to 1% last week while oil prices fell close to 6%.

In other news, China’s Premier Li Qiang pledge in a speech Sunday that China “We will continue to promote opening up, with greater inclusiveness and benefit sharing,” adding that China “will actively expand imports.”. China’s No. 2 official also vowed “to protect the rights and interests of foreign investors in accordance with the law,” comments that come after a measure of foreign investment into the world’s second-largest economy turned negative for the first time since records began in 1998.

Arab countries continue to call for an immediate ceasefire in Gaza, but the US warns this would allow Hamas to regroup. At the same time, however, the US continues to work for humanitarian pauses in the fighting, but Israel’s position remains one where there can be no temporary ceasefire with Hamas until all Israeli hostages are released. Indeed, this morning Bloomberg reports that Israel made a “significant, expanded” push in Hamas-ruled Gaza on Sunday, encircling Gaza City in its entirety and attacking targets above and below ground.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.