Coming in for landing in a heavy cross wind

Insight

It was a quiet start to the week for news flow, which was mostly reflected in market movements, though yields are generally higher.

GE: Factory orders (m/m%), Sep: 0.2 vs. -1.5 exp.

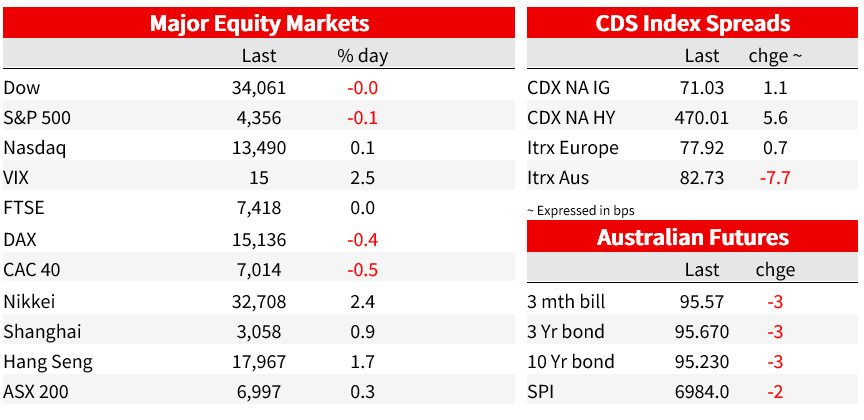

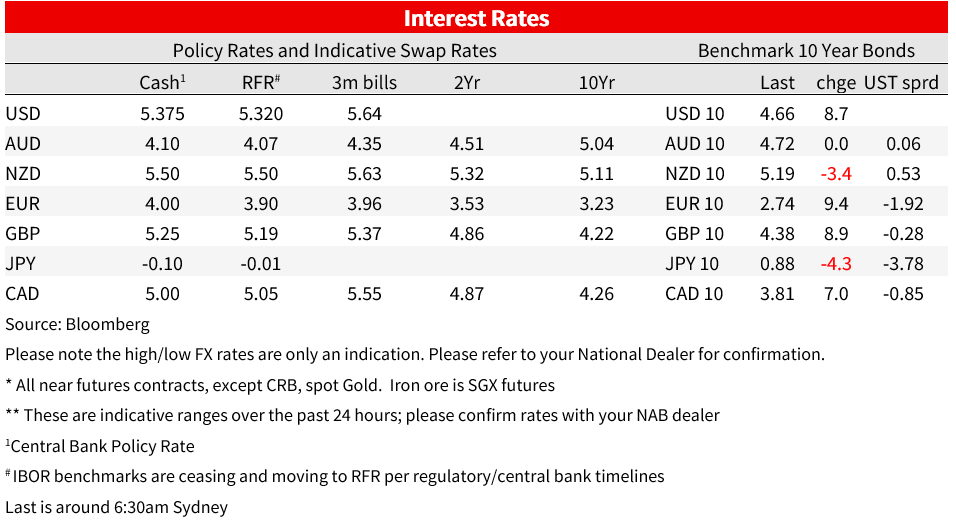

It was a quiet start to the week for news flow, which was reflected in market movements. After the big rally in bonds and equities last week, yields are mostly higher globally to start the new week. the US 10yr yield is up 9bp to 4.66%, back to its level immediately ahead of payrolls data on Friday. The US dollar is a little stronger, up 0.1% on the DXY and equity markets struggled for direction. The S&P500 was little changed heading in to the close, following a 5-day streak of gains. Late in the US session, the Senior Loan Officers Survey was released and showed tighter standards and weaker demand, though the proportion of US banks tightening standards on commercial and industrial loans for medium and large businesses fell to 33.9%, from 50.8%.

BoJ Governor Ueda spoke yesterday and signalled low chance of ending negative rates this year . With only two months to go there was no surprises there. Potentially more important for the timeline towards policy normalisation was a comment that they are watching Spring wage negotiations for next year, which could suggest a more material change to policy settings is unlikely until those outcomes are known. In the context of sharp upward revisions to near-term inflation forecasts, he said that “the likelihood of realizing the outlook for achieving the price stability target of 2 percent seems to be gradually rising,” but that “sustainable and stable achievement of the price stability target is not yet envisaged with sufficient certainty .” Labour cash earnings data due today are expected to rise 1.2% y/y after 1.1%, demonstrating why the BoJ remains uncertain even with elevated near-term inflation. There was little market reaction to Ueda’s comments. 10yr JGB yields were lower at 0.88%, but largely reflecting catch up as Japan returned from a long weekend.

From central bankers, ECB’s Holzmann told Reuters “don’t expect any reduction of the rates soon. Eventually it will happen but for the time being I don’t see it.” Holzmann is on the hawkish end of ECB spectrum, so the comments weren’t taken as an emphatic pushback on pricing for cuts, where 35bp of cuts are priced by June. Holzmann said that “we should stand ready again to hike if needed, and certainly don’t declare victory too early on.”

BoE chief economist Huw Pill spoke and made the point that UK inflation on a year-ended basis will ‘see a sharp fall further’ to levels more in line with other countries, which Pill said would make the UK look less like an outlier to other countries. The BOE’s new forecasts released last week see inflation at 4.8% in October from 6.7% as household energy bills move down another step. Huw said that he did not think those forces that pushed inflation to levels ‘in some cases quite a lot higher’ than the US were very persistent. Looking further forward, Pill saw rates settling somewhere between current ‘restrictive’ levels and pre-pandemic ‘too-low’ levels, but said it was premature to think about cuts at this stage.

In economic news overnight, German factory orders rose 0.2% m/m in September against consensus estimates for a 1.5% drop, but prior data were revised down. A 4.2% jump in foreign orders offset a 5.9% slump in domestic orders and that won’t change the narrative of a very sluggish German economy. Industrial production numbers are due today.

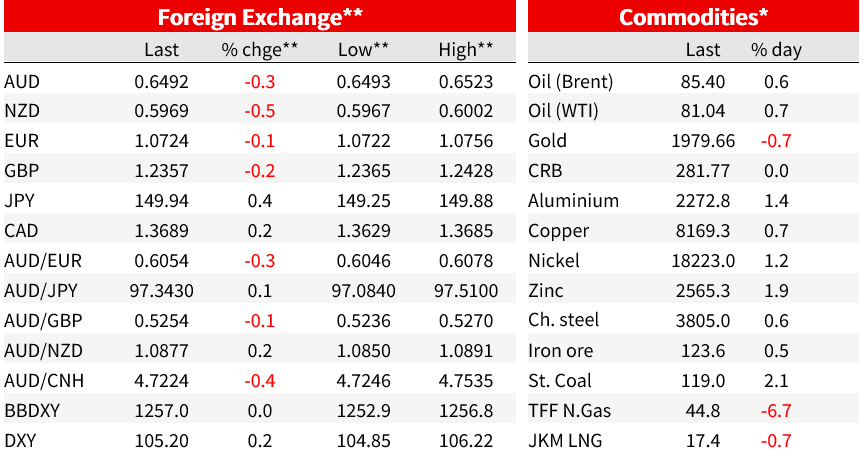

In currency moves the US dollar is 0.1% higher on the DXY. The EUR and GBP show little change from last week’s close, currently 1.0722 and 1.2365 respectively. The USD gained 0.3% against the yen, currently just below 150 at 149.91, helped by higher yields. The AUD lost 0.3% to be back a little below 65c at 0.6492, after touching an intraday high of 0.6523. The NZD was 0.5% lower.

Oil prices were a little higher to start the week, though gains have been pared over the past couple of hours. Brent oil is 0.6% higher to $85.4. Over the weekend, Saudi Arabia and Russia reaffirmed they will stick with oil supply curbs of more than 1 million barrels a day through the end of the year.

Coming Up

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.