Online retail sales growth slowed in May following a fairly strong April

Insight

US PPI beat expectations fuelling hawkish FOMC expectations

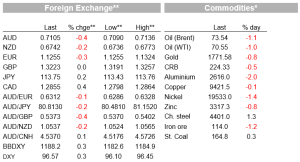

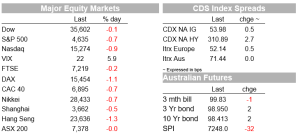

Ahead of the FOMC announcement early tomorrow morning, equities have remained nervous extending their losses for the week. A much bigger than expected jump in US PPI figures has added an extra layer of tension, fuelling hawkish FOMC expectations. Tech shares have led a decline in US equities while EU shares retreated for a fifth day in a row. Heightened Omicron concerns and spike in Gas prices are additional concerns in the old continent. UST yields have edged a little bit higher while the USD is a tad stronger. AUD has remained above 71c while NZD is languishing below 0.6750.

As the FOMC concludes its first of two-day meeting the US data flow has delivered yet another piece of evidence pointing to severe price pressures and an urgent need for policy measures to cool the economy. US PPI posted a record annual increase of almost 10% in November , the PPI for final demand increased 9.6% from a year earlier and 0.8% from the prior month (7.7% for the ex food and energy series). This was the biggest annual gain since the series began in 2010, but the finished goods PPI, which has a longer history, rose by 13.3% y/y, the strongest since 1980. Worryingly too, the PPI for processed goods for intermediate demand was up 26.5% y/y (not a typo), a surge that will sustain a pipeline of inflationary pressures well into 2022.

The PPI data add to the inflation angst by the market and likely cements in the more hawkish pivot widely expected by the Fed. The market is already expecting a faster QE tapering to be announced and currently prices around 3 Fed hikes in 2022 (OIS end 2022 Fed Funds rate priced at 0.88%). The FOMC will also deliver a new set of forecasts with the last two iterations in June and September resulting in economic upgrades with projected rate hikes brought forward. The data flow since June has essentially provided more evidence of inflationary pressures, thus the question is how much more hawkish is the Fed pivot going to be.

My BNZ colleague, Jason Wong has noted that in June and September, projected rate hikes were brought forward and the USD exhibited upward momentum since, while the more hawkish pivot didn’t prevent US equities from trending higher, or the US 10-year rate from tracking around the historically low 1½% mark.

Ahead of the FOMC announcement tomorrow morning, the surge in US PPI has added another layer of edginess to the equity investors. Big US Tech companies are leading the decline with the NASDAQ index down 1.5% as I type, the S&P 500 is -0.88% with Financials (+).71%) the only sector in the green while the Dow is down 0.33%. Meanwhile vibes in Europe are not that great either, European shares are down for a fifth day in a row, the STX Europe 600 index closed the day down 0.84%, the longest streak of losses since mid-March 2020.

In addition to Fed hawkish concerns, Europe’s energy crisis remains in a limbo with no clear imminent resolution. UK and European gas prices rose another 10%, adding to the 10% gains the previous day, with low inventories, geopolitical risk at the Russia-Ukraine border, cold temperatures and a lack of wind power all adding to the fear of power shortages. Oil prices are down 2%, with the IEA saying that the global oil market has returned to surplus, while traders see weaker demand from Omicron as some countries impose restrictions to stop its spread.

Omicron news continue to hit the screen with a positive and negative headlines leaving us none the wiser. Yesterday we learned the Omicron coronavirus variant has appeared for the first time in China, according to health authorities, piling pressure on officials already contending with an outbreak in one of the country’s most important manufacturing hubs. Meanwhile new Omicron infections in the UK are running at 200,000 a day, dwarfing the number of officially confirmed cases, according to an estimate from the UK Health Security Agency.

Overnight New York Governor Kathy Hochul said that Covid-19 hospitalizations across the state has surged by 70% since Thanksgiving, prompting her to institute a statewide indoor mask mandate for businesses without vaccine requirements.

On a more positive note, more analysis of Omicron from a South African study of over 200,000 COVID19 cases showed reduced vaccine effectiveness of a two-dose Pfizer regimen from 80% for Delta to 33% for Omicron, but its effect on hospitalisation was less marked, from 93% to 70%. In contrast to adults, children under the age of 18 are 20% were more likely to end up in hospital. But, then UK infectious diseases academic Robert Read from Southampton said on BBG TV that the South African study was somewhat superficial, limited, a non-robust study, so care was needed when interpreting the result.

Pfizer reported that its anti-viral pill Paxloid cut the risk of hospitalisation or death by up to 89% in high-risk patients and 70% in standard risk patients, according to the final trial results that confirm earlier data. While the trial was conducted when Delta was the prominent variant, early lab studies showed it continued to work against Omicron.

The UK House of Commons approved new Covid measures, but only thanks to support from the main opposition Labour Party, almost 100 Conservatives oppose use of compulsory Covid passes . My colleague Gavin Friend notes all the focus is on the size of the Tory Party rebellion as a measure of dissatisfaction with Johnson on this issue (which many of his own MPs see as too draconian and damaging to the economy) as well as unease with what has been happening on a range of other things like sleaze and parties last yr against govt guidance – an issue that has undermined public confidence in the govt. The polls have swung from around an 11% Tory lead to around a 9pt lead for Labour – the most since 2014.

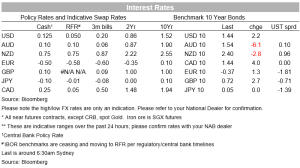

Other data released overnight were in line with expectations. Of interest, UK labour market data showed further strength, reinforcing the noting that the UK labour market remains tight after the end of furlough in September , the demand for labour still outstripping supply as the already known backdrop to Thursday’s BoE meeting. If not for the surge in Omicron case numbers, a BoE rate hike would be taken as given at the end of the week, but the Bank is widely expected to keep rates steady. GBP now trades at 1.3225, unchanged on the day.

UST rates have edged a little bit higher, up around 2bps across the curve with the 10y Note now trading at 1.4377%, broadly similar to changes in yield on most of the European bonds.

In currencies, the USD is a tad stronger recording gains across the board. Commodity linked risk sensitive pairs are the big underperformers with NOK down 0.68% retaining an elevated level of volatility, amid swing in oil prices. Ahead of Thursday’s Norges Bank meeting, a 25bps rate hike is no longer a given, following new covid restrictions by Norway’s government late on Monday.

The NZD has tracked sideways around the 0.6750 mark, after posting a fresh year-to-date low of 0.6736 yesterday afternoon, 1pip below last week’s low. After dipping below 0.71 yesterday, the AUD is trying to stay just above that mark.

Yesterday the NAB Business survey revelead Conditions rose to 12 from 10 pts while Confidence fell to 12 from 20 pts. Importantly capacity utilisation continued to rise to 83.2% and is the highest since June 2021 and is suggestive of a strong rebound in activity and a strong recovery in the labour market from lock downs. Price pressures out of the survey remain elevated, particularly for purchase costs and final product prices, which suggests price pressures showing through in the CPI in Q4 2021.

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.