Firmer consumer and steady outlook

Insight

Quiet data wise, but some notable moves in markets.

Events/Key Headlines

GE: Industrial production (m/m%), Sep: -1.4 vs. -0.2 exp.

BN: Treasuries Extend Rally After 3-Year Auction Sells Without Hitch

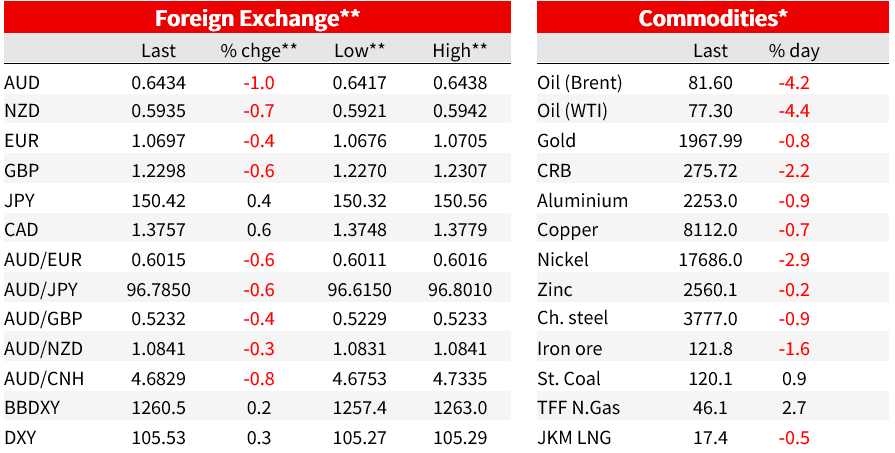

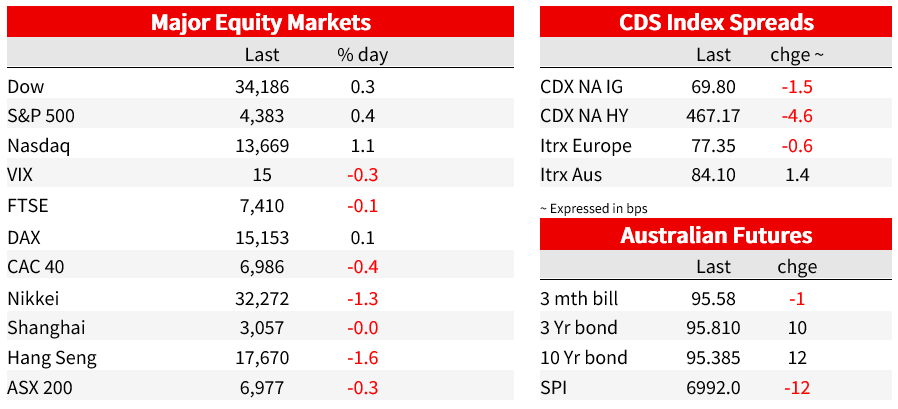

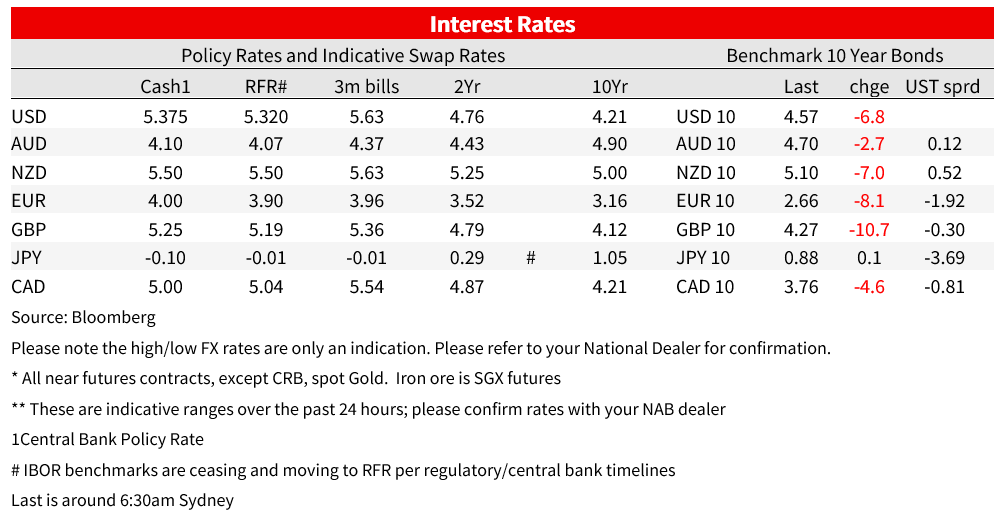

Quiet data wise, but some notable moves in markets. US Treasuries bear flattened with the 10yr yield -8.5bps to 4.56% (low 4.54%; high 4.66%). In contrast 2yr yields were -2.0bps to 4.92%. No rhyme or reason but some of the move came in the wake of a reasonable 3yr auction (clearing very near the when-issued yield and indirect bidders up 8ppt), ahead of tonight’s 10yr and Thursday’s 30yr. Also in the background was some mixed Fed speak, which seemed balanced on net to your scribe (details below). Fed funds pricing dipped further to 93bps worth of cuts priced for 2024 (from 89.9bps of cuts on Monday). The other potential weight was the oil price with Brent -4.1% to $81.68. The 10yr implied breakeven was -2.9bps to 2.39%, while the 10yr TIP was -6.2bps to 2.19%.

Half-way through the last hour of power, US equities are green with the S&P500 up 0.4%. In FX the US dollar has made broad based gains and partially unwinding the weakness from last week following the FOMC and softer than expected US labour market report. The DXY is up 0.2%. Underperforming is the AUD (-1.0% to 0.6434) which is also weaker on the crosses (AUD/NZD -0.3% to 1.0836). Key to that weakness was while the RBA hiked, there was a much less-hawkish tightening bias. Disappointment was also seen in rates with 3yr bond future implying a -10bp yield move over the past 24 hours. The weakest in the G10 basket though has been NOK (USD/NOK +1.2% to 11.1925) with the slide in oil prices a factor. Other majors broadly reflected USD strength: EUR -0.3%; GBP -0.6%; USD/JPY +0.4% to 150.40.

The sharp fall in oil prices certainly got your scribe’s attention. The most plausible explanation appears to be better supply for now in the physical market with several articles noting that Russia’s crude shipments are running at a four month high, China’s trade data yesterday highlighting uncertain demand prospects, and OPEC+ countries exporting in excess of recent production cuts.

As for the RBA, as expected they hiked by 25bps to 4.35%, but what caught the markets’ attention was a much less-hawkish tightening bias. Key to that was the insertion of the qualifier “whether” when discussing the probability of further rate hikes (“Whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and the evolving assessment of risks ”). That qualifier came despite upward revisions to the RBA’s inflation track – now 3½% by end 2024 (up from 3¼%), and “top of the target range of 2 to 3 per cent by the end of 2025” (up from “back within the 2–3 per cent target range in late 2025”). The market reaction saw terminal rate pricing for the RBA move slightly lower (it’s still about 4.45% in May), but there was a much more material rally further along the curve.

NAB revised its RBA call following the RBA meeting. We now expect another 25bp hike most likely in February after the Q4 CPI, and we also think rates cuts are unlikely to begin until November 2024 (previously August 2024) with gradual cuts through 2025 and 2026 to 3.1%. Key for us was the revisions to the outlook which mean a single 25bp adjustment is unlikely to be seen as enough to offset the upside risks. As such, we penciled in a further hike to a 4.6% peak – most likely in February, when the Board will have the benefit of the full Q4 CPI to assess the evolution of inflation pressures (though December is a live possibility) (see NAB note: NAB expects follow up hike in February). Markets currently only priced 2bps of hikes for December and a cumulative 7bps for February.

US Fed speak was not that market moving and seemed balanced. On the hawkish side the Fed’s Bowman said “I continue to expect that we will need to increase the federal funds rate further to bring inflation down to our 2% target in a timely way”. Ditto the Fed’s Kashkari who said “I am not ready to say we are in a good place” and the “Fed would do more on rates if needed”. However Goolsbee sounded more cautious, saying he didn’t want to pre-commit to whether further rate hikes would be required and that the fabled “golden path” was still achievable. Waller who was not speaking on policy suggested he at least was concerned about the recent rise in yields, noting: “ Since the end of July, this thing has gone way up, almost a full percentage point. In central bank terms, in financial markets, that’s an earthquake”.

Data was sparse. German industrial production fell for the fourth consecutive month at -1.4% m/m vs. -0.1% expected. The German manufacturing sector is under pressure from high energy prices, the rise in interest rates and the slowdown in China. Data out of China yesterday was mixed with imports beating with its first increase since February (+3.0% y/y vs. -5.0% expected), but exports faltering (-6.4% y/y vs. ‑3.5% expected). The recovery in China remains fragile, the data coming after last week’s disappointing Official PMIs.

Coming up:

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.