Robust growth for online retail sales observed in June

Insight

Oil prices down again as demand pessimism deepens

Across the financial asset and commodity price complex, oil continues to show the most volatility, crude oil benchmarks adding 2.5% or so to Tuesday’s 4% fall, reportedly on deepening pessimism about the demand and hence global growth outlook. In which respect former ECB chief Mario Draghi says the Eurozone will be in recession by year end, though he is pinning the blame for that partly on high energy prices. US equities are though having a good last couple of hours of NYSE trading, recouping most of their morning fall to be little changed on the day. The big USD is also fairly flat but where commodity linked currencies (AUD, NZD, CAD) are faring worse alongside a weaker JPY. The US 10-year note auction received a mixed recession, ‘tailing’ by 1bps but with a stronger indirect bid than last time, seen as symptomatic of strong foreign demand. Yields fell a couple basis points post auction to be back knocking on the door of 4.50% but have pulled back up in late day NY trade. .

Economic news flow has been light overnight, of note just Eurozone October Retail sales -0.3% m/m vs -0.2% expected, though yr/yr it’s -2.9% vs. -3.1% expected thanks to upward revisions, but this is down from -1.8% in August. Final German October CPI at 3.8% headline and 3.0% HICP were both unchanged on the preliminary release.

We’ve had some contrasting inflation expectations news. The ECB 1-year ahead CPI inflation expectation series rose to 4.0% from 3.5% (3-year expectations unchanged at 2.5%) which is in contrast to yesterday’s NZ ones, where the 1-year ahead eased to 3.60% from 4.17% a quarter ago (so heading in the right direction). But a push higher in the 5-year and 10-year ahead series, to 2.43% (from 2.25%) and 2.28% (from 2.22%) respectively, will raise an eyebrow at the RBNZ and something to keep an eye on (albeit this is a survey with a mere 39 respondents).

One central bank still exhibiting a clear tightening bias is the Bank of Canada summary of its 25 October meeting noting that. “Some members felt that it was more likely than not that the policy rate would need to increase further to return inflation to target,” the minutes said, adding that the lack of downward momentum in underlying, or core, inflation was a source of concern. “Others viewed the most likely scenario as one where a 5% policy rate would be sufficient to get inflation back to the 2% target, provided it was maintained at that level for long enough.”

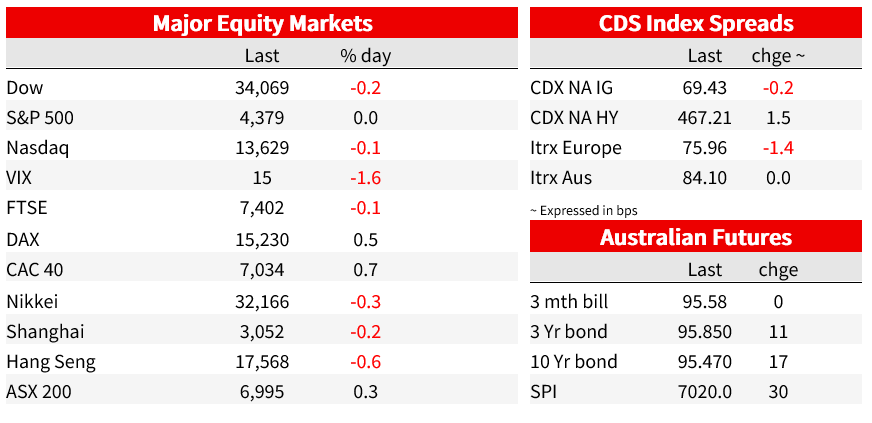

In Bond land, the keenly anticipated 10-year Note auction cleared at 4.52%, bps above its when-issued or pre-action level of 5.51%, while the bid-cover ratio of 2.45 was down on 2.50 last time. Nevertheless, the indirect bidder interest – often seen as reflective of the strength or otherwise of foreign demand – was up on last time at 69.7% (60.3%) such that we saw a small rally post auction with 10s back knocking on the door of 4.50%. Since when, they have pulled back up to be 4.525% (-4bps -4.1% on Tuesday’s NY close) arguably in conjunction with the recovery in US stock market where the S&P500 and NASDAQ are now back to flat for the day 30 minutes prior to the close. Aussie 10-year futures have an implied yield 8bps down on Wednesday’s local close, at 4.52% (so the ACGB-UST 10-year yield gap now effectively zero). Earlier, 10-year Bunds finished 4.3bps lower and gilts -3.5bps.

In FX, the USD is overall little changed (DXY flat, thanks largely to a flat EUR/USD hovering around 1.07, held up by a stronger USD/JPY (+0.4%) but down by weaker commodity linked currencies (CAD -0.2%, which figures in the DXY, plus we have AUD/USD – not part of DXY -0.5% in the last 24 hours ago to a low of 0.6404. It was trading above 0.6480 in front of Tuesday’s RBA rate hike.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.