Online retail sales growth slowed in May following a fairly strong April

Insight

Bostic retracts his 50bps comment, states “is not my preferred policy action” for March

https://soundcloud.com/user-291029717/rba-to-join-the-rate-rise-race?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

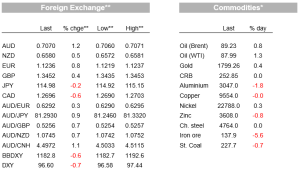

A positive day for risk assets with some seeing value emerge after the sharp sell-off in equities (S&P500 so far +1.5% and NASDAQ +2.7%). A late day retraction by the Fed’s Bostic in which he played down the prospects of a 50bps hike in March also added (50bps “is not my preferred policy action ” for March). Shorter end US yields likewise retraced their earlier 5.2bps increase in Asia – that move having been driven by Bostic’s initial comments in a w/e FT interview in which he seemingly supported the possibility of a 50bp move if needed. US 2 year yields are now broadly unchanged on a 24 hour basis at 1.17%. 10yr yields were also little moved, up just 0.5bps to 1.77%. The improvement in risk sentiment is clearly seen in G10 FX where the AUD leapt 1.2% to 70.67, reversing earlier declines and outperforming the fall in the USD with the DXY -0.7%. There were also comments by a several other Fed speakers, though these were not market moving.

First to Fed speak. The most notable in terms of market moves was the Fed’s Bostic retreat from his earlier words of a 50bp hike being a possibility. Bostic said in a yahoo finance interview that a 50 basis point hike in March “is not my preferred policy action,” and that he still has “…three rate increases in mind. March is looking like the right time”. From there, however, “we are not on any set progression. ”. The Fed’s Daly also refused to play the hawkish line, noting that market pricing for 5 rate hikes in 2022 is “…quite a bit of tightening, but it’s also quite a bit of accommodation left in the system because the terminal rate of interest is 2.5%…”.

Daly also believed that the Fed was “not behind the curve, we are not behind the curve at all.”. Receiving little attention, but perhaps significant given the unknown impacts of quantitative tightening, the Fed’s George noted “More aggressive action on the balance sheet could allow for a shallower path for the policy rate,” and that “ by holding long duration assets, the Fed’s balance sheet is depressing the price of duration, by lowering longer-term yields by as much as 1.5 percentage points according to some rules-of-thumb, incentivizing reach-for-yield behavior and increasing fragility within the financial system …”. The rule of thumb is interesting and suggests the Fed is prepared for higher yields and for what may follow – i.e. the Fed put is lower .

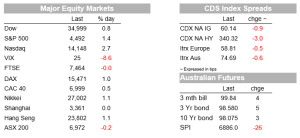

The back to back consecutive rise in US stocks has got some thinking whether the trough has passed. Despite the talk of higher rates, earnings so far have been much better than expected. About one-third of S&P 500 companies have reported fourth-quarter earnings and 77% have beaten Wall Street’s earnings expectations, according to FactSet. Whether we have passed the trough is uncertain, but certainly for some value is re-emerging. The S&P500 is up 1.5% so far today, meaning for January it has fallen just shy of 6% for the month. Tech stocks are leading the charge, with the Nasdaq index up 2½% and if this is sustained into the close, then the index would also avoid recording a double-digit percentage drop for January. This week is a big week for equities with earnings from key names including Alphabet and Amazon.

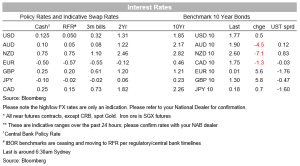

As for rates there has been little in the way of developments overnight. The US 10 year yield is broadly steady at 1.77% and 4.9 rate hikes are priced for 2022. Across the pond European 10-year rates are up in the order of 5-6bps, not helped by higher inflation data. CPI inflation data in January for Germany was much stronger than expected, with the EU harmonised measure at 0.9% m/m against 0.0% expected! The annual rate of inflation is running at up 0.9% m/m and 5.1% y/y. While the figures were driven by higher energy costs, core inflationary pressure remained strong. CPI inflation for Spain was also much higher than expected, at 6.1% y/y. Euro area data will be released on Wednesday. Meanwhile GDP data for region was slightly softer than expected at 0.3% q/q for Q4 against 0.4% expected. Also in terms of data was the US Chicago PMI which surprisingly lifted to 65.2 (61.5 expected) and points to upside risk to the ISM Manufacturing tonight.

In FX the USD has pulled back from its cyclical high recorded at the end of last week, with the DXY index down 0.7%. The euro was supported after the strong Germany inflation data and the positive Italian election result will be helping as well for the 0.8% gain in EUR to 1.1244. The AUD is showing its exposure to the positive risk sentiment, up some 1.2% to 0.7070.

Finally in European news, the Italy-Germany 10-year spread narrowed after the Italian Presidential election result, which removes some political risk overhanging the country. Meanwhile in the UK PM Johnson grip on power looks tenuous after the publishing of the Partygate investigation. In a series of damning conclusions, senior civil servant Sue Gray’s partial findings said there were “failures of leadership and judgment by different parts of No 10 and the Cabinet Office at different times” and some of the behavior was “difficult to justify.”

Domestically all focus on the RBA. There is also plenty of second-tier data out with the most important being Retail Sales for December. Offshore the only real top-tier data release is the US ISM Manufacturing where focus will be on the prices paid series after the unexpectedly sharp fall in the prices index in December. Details below:

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Online retail sales growth slowed in May following a fairly strong April

Insight

Long-term signal vs. Short-term noise

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.