Total spending grew 0.9% in June.

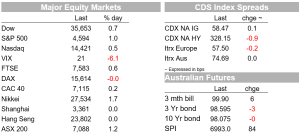

Equities recovery continued overnight with both European and US markets extending recent gains.

Equities recovery continued overnight with both European and US markets extending recent gains. EU inflation beats expectations and prints a new record high, piling on the pressure for the ECB to change its tune. EU rates tick higher while the UST curve bull flattens, ADP is a big miss, printing a 301K drop in private payrolls. EU currencies lead gains against the greenback while AUD and NZD are little changed.

As I type, the S&P 500 is 0.93% higher on the day and the NASDAQ is +0.50%, the former looks set close with gains for a fourth consecutive day while the latter is aiming for a fifth day. Strong earnings results and guidance continue to support the equity market, helping easing concerns over companies’ ability to perform in a rising cash environment, so far roughly 80% of S&P 500 companies have met or beat estimates. Notable US performers over the past 24 hours include Alphabet and Advanced Micro Devices following solid earnings reports. In Europe, the Stoxx Europe 600 gained 0.45% with Novo Nordisk and Vodafone both gaining after reporting on Wednesday.

EU inflation surpassed expectations and printed a new record high (post-2000). CPI for January climbed one tenth to 5.1% yoy, punching through the 4.4% median estimate reported by Bloomberg . While slowing in Germany and France, the euro zone’s two biggest economies, the spike in energy saw headline inflation rising across the remaining members of the currency bloc. Excluding energy and other volatile components like food, core inflation was 2.3%, down from last month’s 2.6%.The decline was largely attributed to base effects related to Germany’s VAT cut in the second half of 2020, that said EU core CPI remains above the ECB’s 2% target.

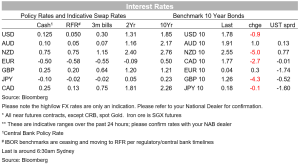

Money markets briefly priced a 10bps ECB rate hike as early as July, German 2-year yields climb for a seventh day to -0.477%, its longest rising streak since September 2017 . Core EU 10y yields edged up around 1bps on average with 10y Bunds ending the day at 0.036%. The ECB meets tonight (more below) and while expectations are for the Bank to stick to its inflation narrative that price pressures will abate, ECB President Lagarde will face tough question at the press conference. The pandemic bond buying programme will end in March and the ECB still plans to buy bonds (under its separate Asset Purchase Programme) until at least October, which would seem to rule out rate increases before then.

Moving onto the US, the ADP private payrolls report was a big miss, printing -301k of job losses against expectations for a rise of 180k. The US Omicron wave was largely to blame with more than 5m people – officially – reportedly infected in the week of the payroll survey. This suggest the drop in jobs should have been bigger, but workers only fall off payrolls if they did zero paid work during the pay period covered by the survey week and received zero paid sickness leave. Overall, there is a general sense that this is a temporary setback which arguably could extend into February, making interpretation of the state of the US labour market a difficult task over the near term and it is worth stressing here that history also suggests the recovery of covid job losses do not reverse immediately. Forecasts for Friday’s payrolls are now all over the place with many calling for a negative print in January (median estimate is officially still at +150k). Depending on the magnitude of the disruption, this can potentially become a solid excuse for the Fed the wait on the side lines after a first-rate hike in March. A theme to watch, but for now this yet another reason to push back on the notion of more than 4 rate hikes this year.

The UST has traded with a bull flattening bias over the past 24 hours with a 4.2bps decline in the 30y Bond to 2.069% leading the way. The 10y Note is 3.8bps lower and now trades at 1.76% while 2y rate is 1.5bps lower at 1.155%.

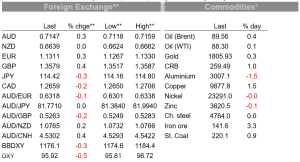

The USD has continued its recent broad decline with the DXY index now trading below the 96 handle ( 95.94, and down 0.45% over the past 24 hours) , European currencies have lead the charge as the market ponders the potential for the ECB to join other central banks in begin a new rate hike cycle. The EUR has appreciated 0.36% to 1.1314, now almost 2 cents above the lows reached last week with higher beta EU pairs such as NOK and SEK up 0.61% and 0.85% respectively. Meanwhile NZD and AUD have consolidated after their strong gains over the past few days. The AUD now trades at 0.7148 and like yesterday small blip post the RBA statement, Governor Lowe speech yesterday only elicited a small pull back, with the pair essentially unchanged over the past 24 hours.

While the Governor’s speech largely reiterated yesterday’s post-Board Statement, the Q&A to the speech was more insightful. The key takeaways were that: (1) The RBA is still “prepared to be patient ” as they await more information on wages growth and the outlook and trajectory for inflation until they can conclude inflation is sustainably at target. Interest rate rises starting later in 2022 were deemed “a plausible scenario”, but “it’s still quite plausible that the first increase…is a year or longer away ”. (2) There is no strict definition of what inflation sustainably at target means with relevant factors being the actual rate of inflation, the trajectory and the breadth of price increases, as well as aggregate wages growth; (3) Governor Lowe expects supply chain disruptions to be resolved over the months ahead and the RBA does not see a large risk of the economy overheating from keeping rates at 0.1%.

OPEC and friends agreed to a nominal increase of a 400k b/d from March, but in practice the market remains sceptical on the ability of the group to deliver on its supply promises . Bloomberg notes that while Saudi Arabia, the UAE, Iraq and Kuwait have spare capacity, the remaining 23 members are struggling with lack of investment and unrest. Lybia and Nigeria are top of the list amongst strugglers, but last month’s drone strike in Abu Dhabi are a new increasing concern while the Ukraine tensions now also means Russia is one to watch. OPEC supply constraints have been supportive for oil prices, these concerns have not yet gone away. WTI and Brent ended the day little changed at $88.07 and $89.27 respectively.

On Ukraine tensions news, while diplomatic dialogue continues, the US has moved more troops into Europe and ordered soldiers already stationed on the continent to move further east. Russia called the move ‘destructive’ . Meanwhile Russia’s foreign policy aide Yuri Ushakov told reporters in Moscow Beijing supports Moscow’s demand for security guarantees from the US and NATO.

(I: FRX, FXMARKET, AUD, 30025, 30036, 30022, JFRX, ?15308575, ?3377279)

Read our NAB Markets Research disclaimer

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.