Total spending grew 0.9% in June.

Subdued start to the week ahead of US CPI tonight

Overnight data:

A fairly subdued start ot the new trading owed something both to the absence of major market moving news Monday and the proximity to the week’s key global economic release – tonight’s US October CPI report. Locally we also have interest in the latest NAB Business Survey and Westpac’s Consumer Confidence reading, while NZ has its inaugural monthly CPI print.

The data calendar has been light but not without interest. China credit growth figures released last night were mixed relative to expectations (New Yuan Loans higher, Aggregate Financing lower) but showing relatively steady loan growth in both overall aggregate financing and the narrower Yuan Loans metric (ditto money supply growth) but with the mix showing strong growth in government debt and relatively weaker private sector loan growth. Almost 85% of net credit extended in October was from the sale of government bonds. The data don’t give us a whole lot of steer on whether this week’s slug of October activity readings (tomorrow) are apt to come in above or below expectations.

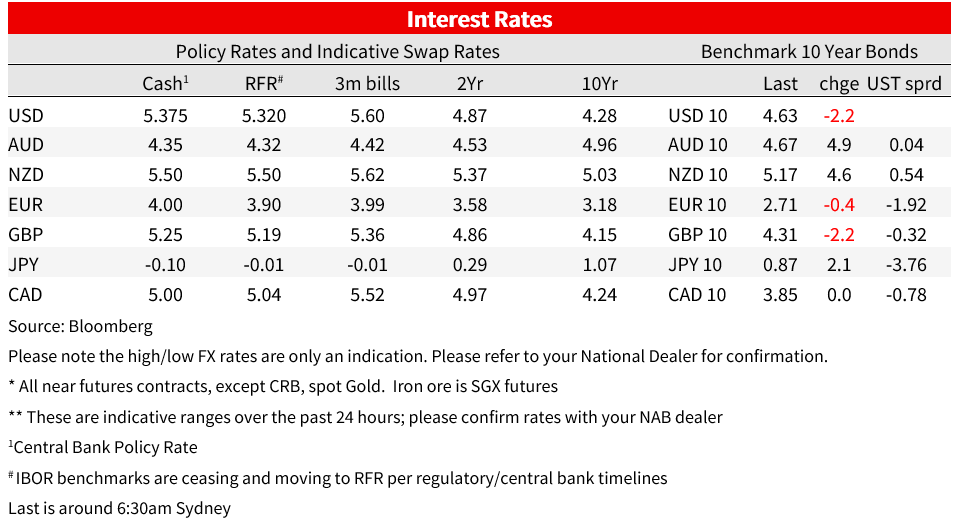

More market moving and ahead of US CPI tonight, The New York Fed’s survey of consumer expectations showed one year ahead inflation expectations reading slip from 3.67% to 3.57% (back close to its cycle low of 3.55% recorded in July). 2-year Treasury yields slipped from 5.06% to 5.04% post release. Treasury market volatility has been low overall, with 10s tracing out 4.63% to 4.695% range, currently on the day lows (-2.4bps versus last Friday’s NY close). 2s have held their post inflation expectations rally, currently -2.5bps down at 5.04%. Earlier in Europe, benchmark bonds were very narrowly mixed (10yr Bunds -0.4%, Gilts -2.1bps). 10-year Aussie futures are 2bps lower in yield terms from Monday’s local close.

On the US political front, markets are travelling on the presumption a US government shutdown from this Saturday, following the expiration of the current Continuing Resolution, will be avoided with incumbent House speaker Johnson’s proposals for a new (‘staggered’) stop-gap funding bill not similar to one his predecessor got through Congress in October (absent funding, at this stage, for the Ukraine and Israel war efforts). Tomorrow of course Presidents Biden and Xie meet, and quite how much bonhomie is seen to be exuding from the encounter will be of some importance.

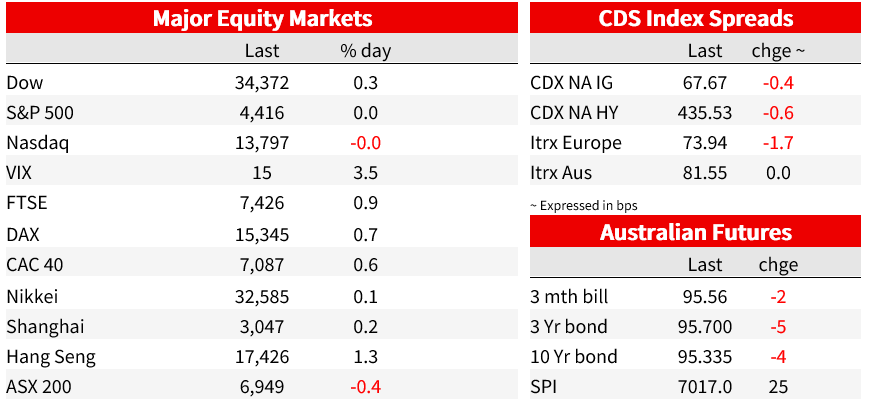

US Equities are having a quiet day, flitting in and out of the green/red during the last hour of trade, after what was a positive day for Europe but where gains of just under 1% for most indices was largely playing catch up to Friday’s New York afternoon rally.

In currencies, despite a slightly softer USD overall and the aforementioned minor slippage in Treasury yields, USD/JPY made a new cycle high of ¥151.91 overnight (4 pips shy of the 21 Sep 2022 high which preceded BoJ FX intervention). This despite the fact that Treasuries are well off their recent high north of 5.0%. Incidentally, MoF’s currency Czar Kenji Kanda was forced to resign yesterday for non-payment of taxes, so the person who would be phoning the BoJ to order intervention is currently not at his post, not that that should impact on any MoF decision to intervene.

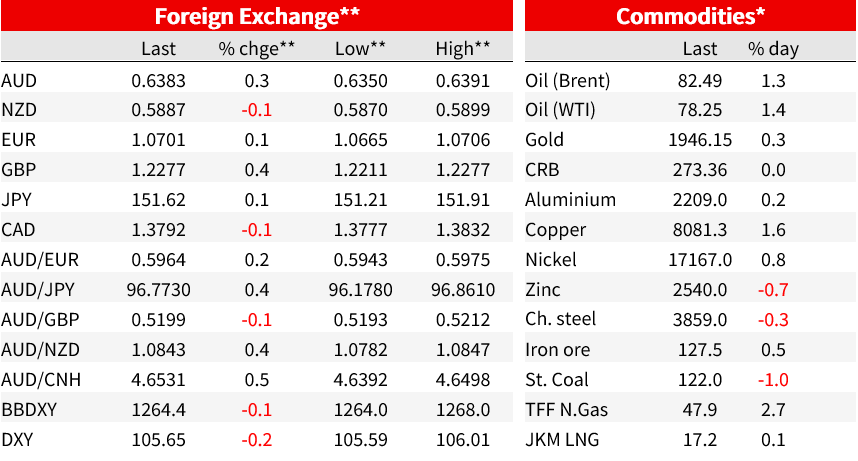

Mild USD slippage (DXY -0.2%, BBDXY -0.13%) goes hand in hand with the small, level shift down in US Treasury yields post the NY Fed inflation expectations data, the main beneficiaries of which have been the SEK, NOK, GBP and AUD, all up between 0.3% and 0.5% (AUD/USD to a high of 0.6391). Oil is up about $1 and gold $6 to $1,947.

Coming Up

Market Prices

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.